On November 12, 2019, the DoubleLine Emerging Markets team held a webcast discussing the Emerging Markets Fixed Income Fund (DBLEX/DLENX), the Low Duration Emerging Markets Fixed Income Fund (DBLLX/DELNX) and the Global Bond Fund (DBLGX/DLGBX) titled “Navigating Deglobalization.”

Q3 2019 hedge fund letters, conferences and more

This recap is not intended to represent a complete transcript of the webcast It is not intended as solicitation to buy or sell securities If you are interested in hearing more of the Emerging Markets team’s views please listen to the full version of this webcast on www doublelinefunds com under “Latest Webcasts” under the “tab You can use the “Jump To” feature to navigate to each slide You can also learn more about future webcasts by viewing the 2019 webcast schedule at www doublelinefunds com under Webcasts”.

DBLGX Duration (As of 11/30/2019) 5.38; FTSE WGBI Duration (As of 11/30/2019) 8.48

Gross Expense Ratio I share 0 55 N share 0 80

Performance data quoted represents past performance past performance does not guarantee future results The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost Current performance of the fund may be lower or higher than the performance quoted Performance data current to the most recent month end may be obtained by calling 213 633 8200 or by visiting www doublelinefunds com.

Recap

Macro Outlook Deglobalization

Trade War

- The trade war has accelerated deglobalization tendencies across the globe.

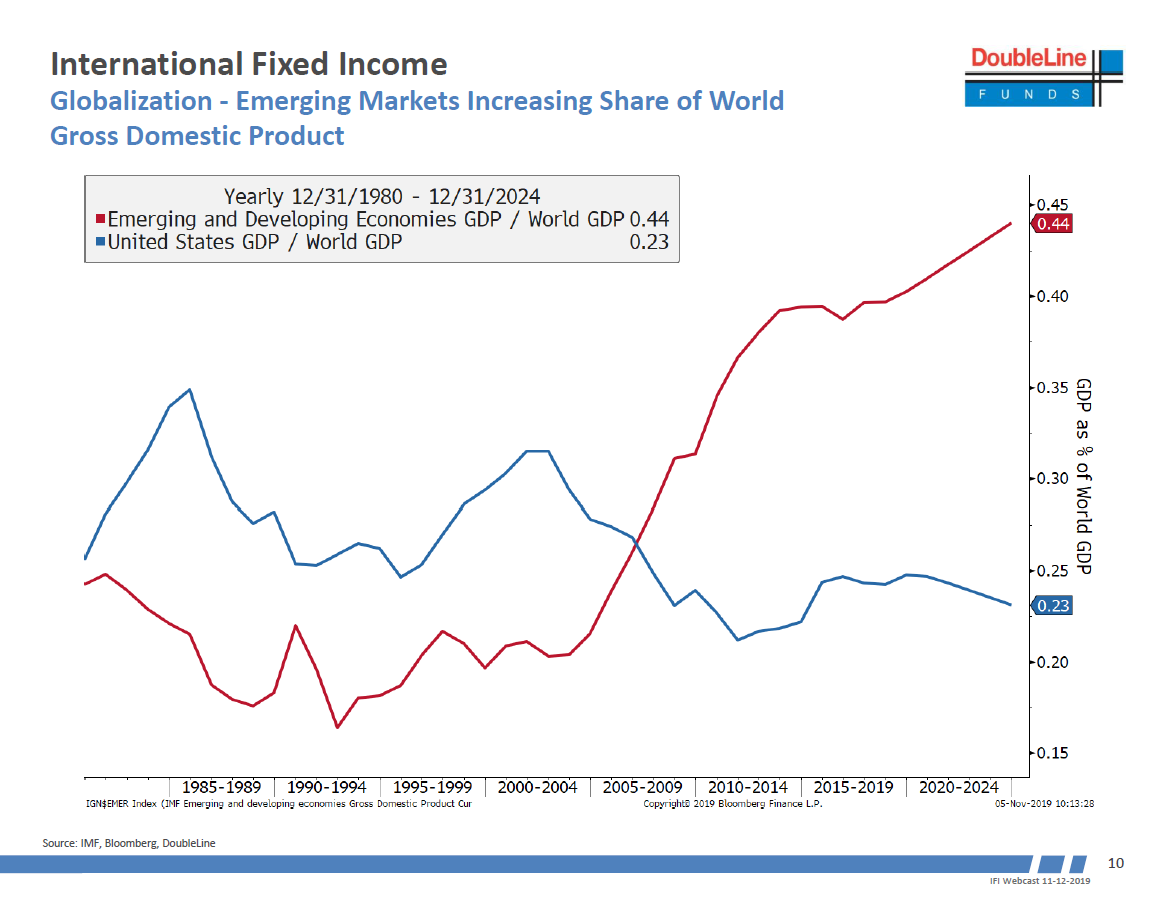

- This comes after a period of globalization, led by emerging markets In the early 2000s, emerging market economies accounted for roughly 20 of global growth Today, emerging markets make up roughly 44 of global Gross Domestic Product (growth, as measured by the International Monetary Fund (IMF).

- Emerging markets experienced most of their growth through the export channel.

- Developed markets’ demand for goods has driven emerging market growth the past two decades.

- The United States (U S has seen its share of global GDP growth reduced from 33 in the early 2000 s to roughly 23 today.

- In the 2000 s, the U S ramped up its imports of energy products, largely oil Today that energy gap has narrowed despite the fact the trade deficit has been widening.

- America went from one of the largest global importers of energy to a net exporter of energy.

- China has accounted for the lion’s share of exported goods to the United States since 2009 hence the current focus of trying to rebalance trade relations with China due to the goods deficit.

- The trade war escalation has led to a drop in total global exports Global imports, as a contributor to global GDP, has fallen to roughly zero on a net basis.

- Global trade volumes on a year over year ( basis have fallen into negative territory The only other time we saw negative readings to this magnitude was during the previous two recessions in 2001 and 2008.

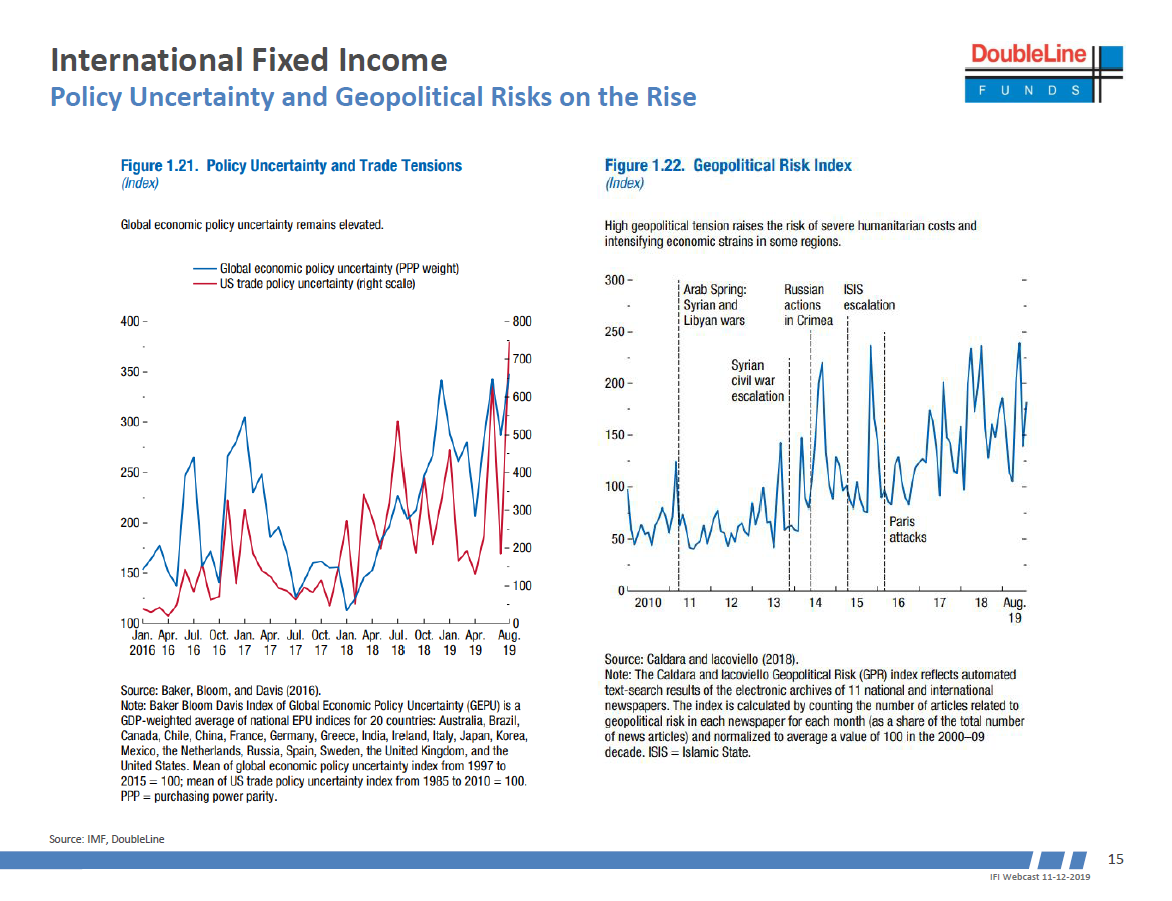

Policy Uncertainty Geopolitical Risk

- There may be some correlation to trade wars, but nonetheless, global policy uncertainty has risen substantially, per the IMF.

The net impact of policy uncertainty has been that foreign direct investments have fallen, or companies that are investing outside of their borders Firms have decided that with uncertainty on trade, policy, and geopolitical risks they will hold back on investments Foreign direct investments has fallen to essentially zero as a percentage of GDP.- Reinvestment of earnings has driven the U S net foreign direct investment flows into negative territory for the first time in over two decades.

- U S imports from China have unsurprisingly fallen, with other Asian economies being the beneficiaries, as exports to the U S have increased from Vietnam, Taiwan, Thailand, and Singapore.

Financial Linkages

The United States Dollar (USD)

- The USD dominates foreign exchange reserves, international debt, international loans, and foreign exchange turnover.

- The USD also leads invoicing for most exports and imports, especially in emerging market countries, followed by the Euro.

- USD offshore credit for non U S entities has increased steadily since 2002.

Societal Tensions

Rising Inequality, Automation Risk, Underwhelming Labor Market Reforms

- Rising inequality is not just a U S phenomenon Workers globally have seen their incomes grow at a slower pace than GDP growth and inflation.

- In the U S the top 0 1 owns as many assets as the bottom 90 combined.

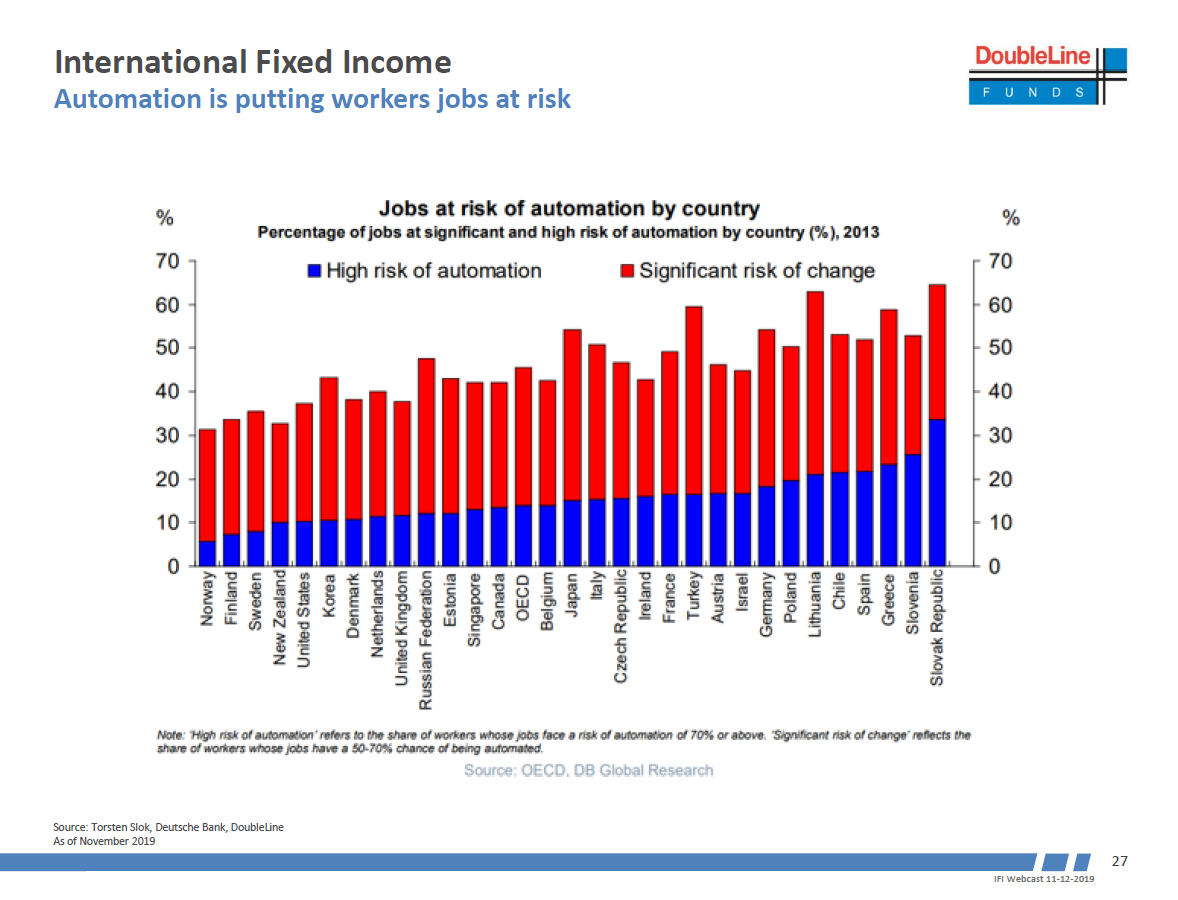

- Many jobs globally, especially on the manufacturing side, are at risk of being replaced or eliminated by automation.

- Output gains globally from major reforms in labor markets, domestic finance, and product markets have all underwhelmed versus the IMF and economists’ estimates, further frustrating workers.

- As a result, we have seen a rise in populism and social tensions in many countries, globally.

Global Markets

Global Growth Uncertainty

- Global growth slowed fairly sharply in 2015 and 2016 on the back of a commodity price orrection, concern about China’s reserves, and the weakness of the Chinese currency

- Strong stimulus in 2017 and 2018 from China and Europe as well as fiscal stimulus from the U S brought global growth back.

- Trade wars started in 2018 and we saw global growth slow once again Global central banks and governments have responded with more accommodative monetary policies, respectively.

- The big question now is whether this is going to be an experience similar to 2013 and 2015-2016 where we had a slowdown and then a cyclical bounce or this is something potentially worse, as we saw in 2000-2001 and 2007-2008.

- Germany, an export driven economy has been very weak with the combination of the slowdown in global trade volume and auto industry issues, more specifically around emissions and slowing global auto demand

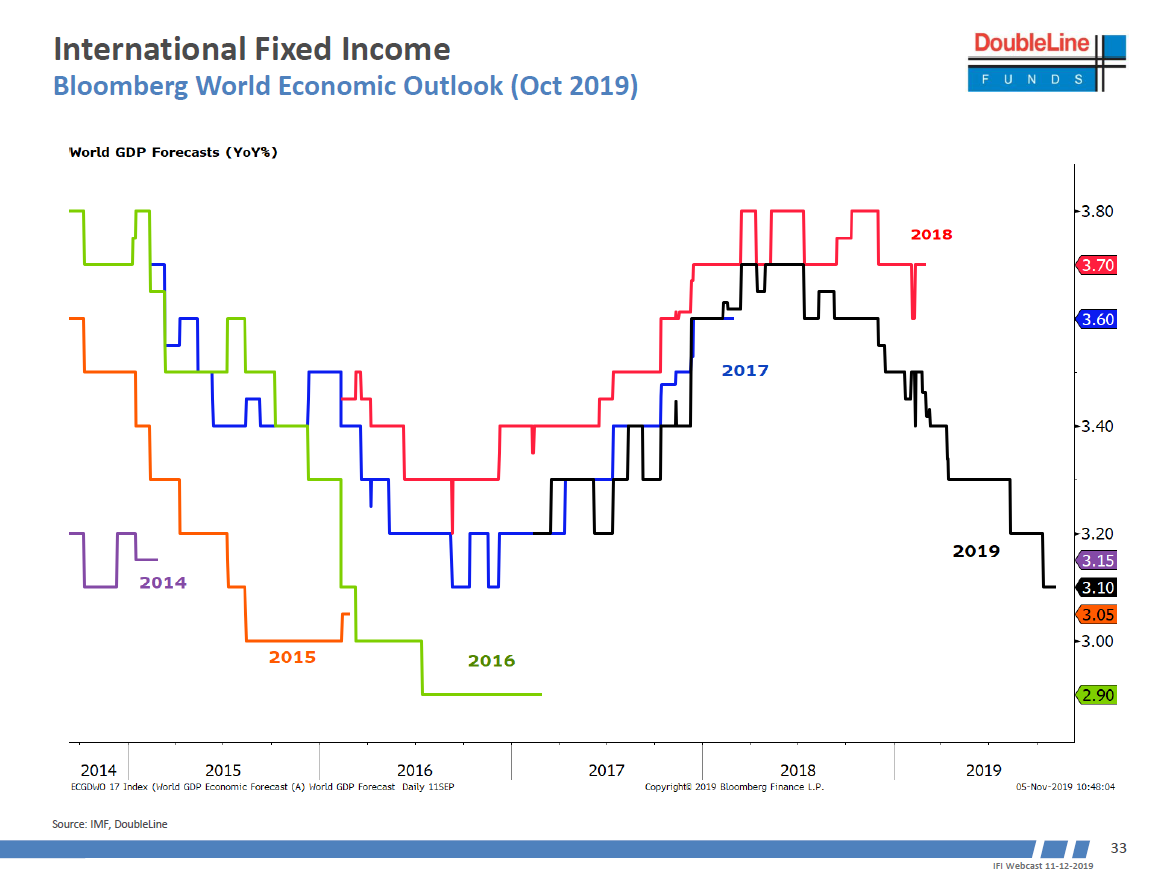

- The IMF projects global GDP growth to slow to 3% in 2019 from 3.6% in 2018 but then pick up to 3.4% in 2020 The expected pickup in growth next year is projected to be driven by emerging market economies, not by developed countries.

- The IMF expects emerging market growth to pick up from 3.9% in 2019 to 4.6% in 2020.

China Growth Deceleration

- While the official GDP growth figure in China has been slowing, the slowdown in real activity and industrial activity, as measured by the Li Keqiang Index, has been much more gradual.

- Fiscal spending in China remains robust and continues to pick up.

Europe & US

-

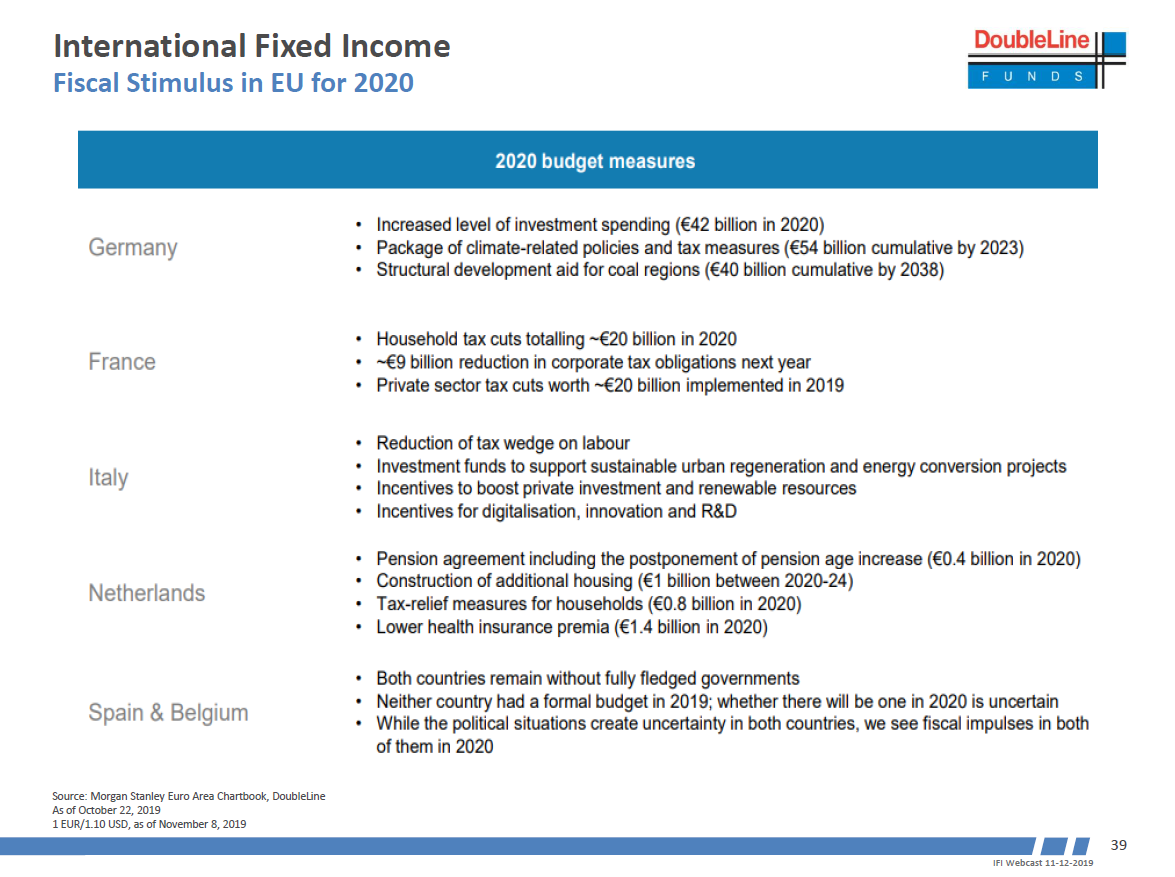

- The market is expecting a lot of fiscal stimulus out of Europe in 2020 done so in small packages across the European Union (EU).

- In the U S fiscal expansion is expected to continue no matter which political party wins the 2020 Presidential election.

- On the monetary policy front, we have seen interest rate cuts by both developed and emerging market central banks this year Beyond interest rate policy, central banks have also been expanding their balance sheets

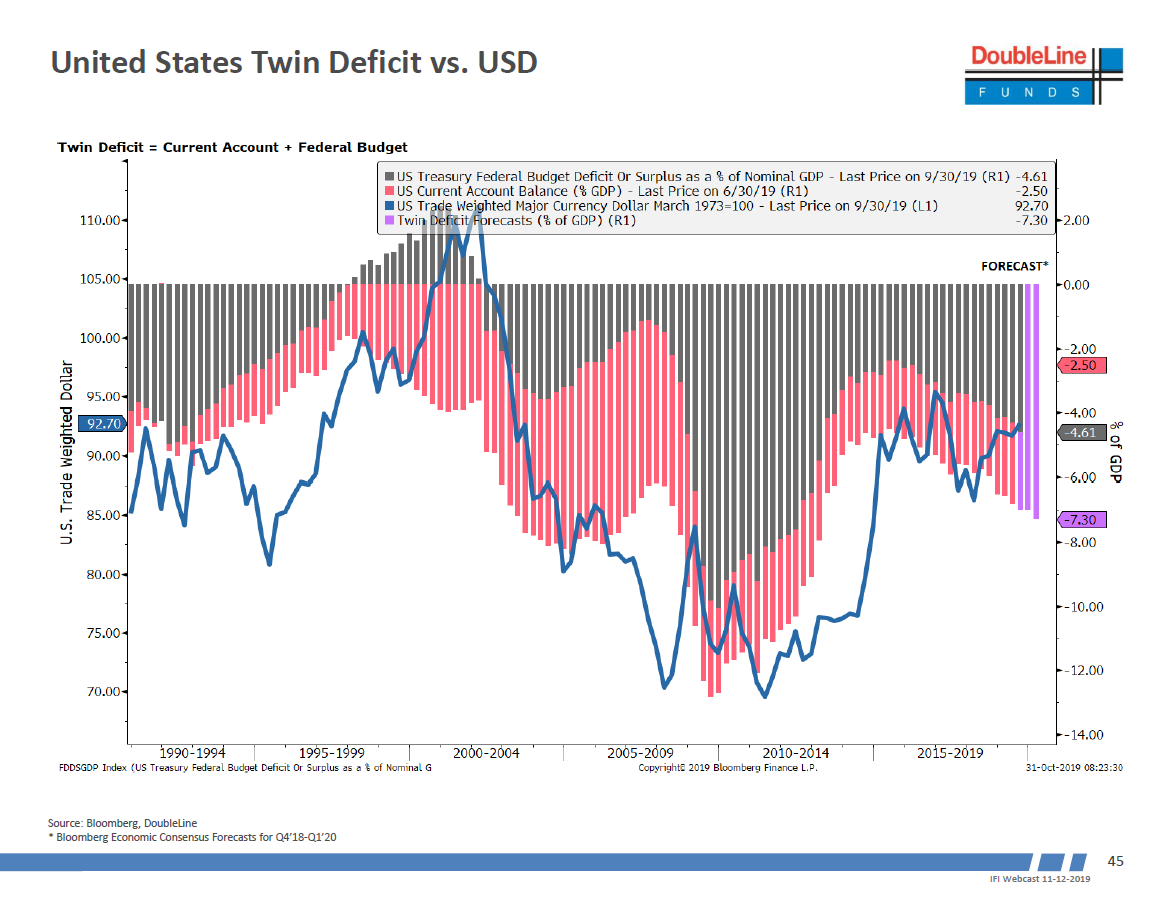

- The U S budget deficit should continue to widen, which should stimulate the global economy.

- The combination of continued fiscal expansion and monetary policy easing underlies DoubleLine’s view that the USD will be pressured to depreciate.

- Historically, as trade deficits and fiscal deficits widen, it puts devaluation pressures on the currency.

- Slowing global growth and escalation of trade tensions were both tailwinds for the USD in the second half of 2018 The fact that the USD has not risen more aggressively in 2019 as both of these tailwinds have persisted implies to DoubleLine that speculative net short positioning on the USD has kept the USD from appreciating further Furthermore, any reduction in the trade tensions could potentially be net USD negative, net positive for non dollar currencies, and net positive for global growth

Interest Rates

- The amount of debt of companies in developed countries with an interest coverage ratio of less than one has been rising meaning companies that are laden with a lot of debt could have trouble servicing their debt should growth slow or earnings and revenues decline.

- This is especially concerning when taking into account this number has risen despite interest rates falling rather aggressively.

- U.S . total debt outstanding is now over 100% of GDP.

- Despite the U.S. Federal Reserve (Fed) viewing inflation as muted, many measures of inflation are printing above the Fed’s 2% target.

- Wage growth robustness, especially in developed markets, has likely contributed to higher core inflation measures.

- Despite concerns around trade & slowing manufacturing data, consumer confidence remains robust in both developed and emerging market economies.

- The bulk of the U.S. Treasury (UST) rate rally transpired during trade war escalations, so the question is: What would rates do if a de escalation of the trade war occurs or a ‘mini deal’ is reached?

- At DoubleLine, we believe the 10 year UST yield hit a potential low earlier this year. We are watching the 2% level on the 10 year UST very closely as there is congestion at that level.

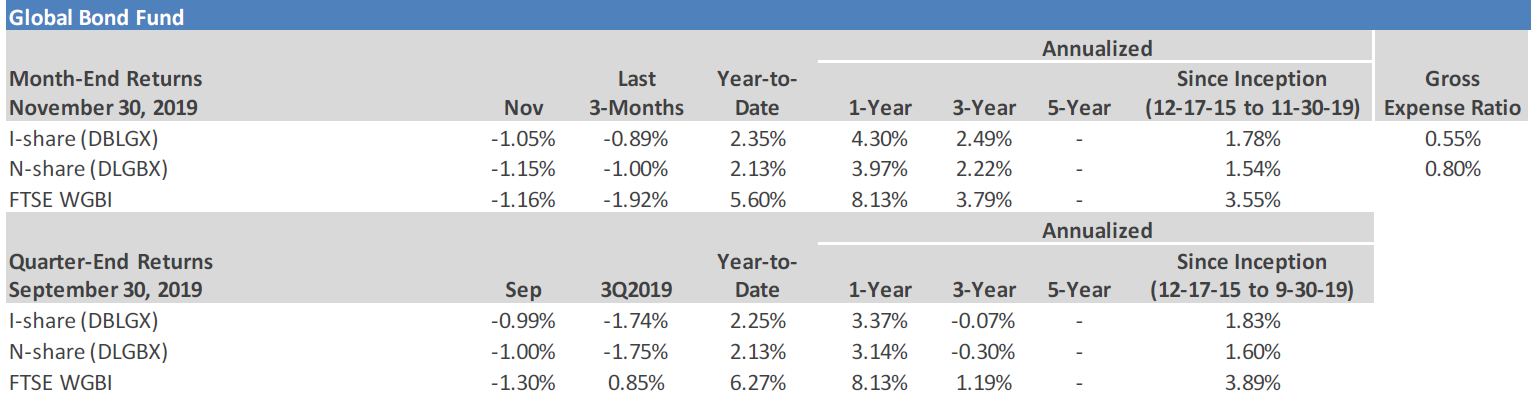

DoubleLine Global Bond Fund (DBLGX) Review

- 1 year performance as of 11/30/2019

- DBLGX: 4.30%

- FTSE WGBI Index: 8.13%

- 12 month underperformance was driven by the Funds shorter duration relative to the benchmark as global interest rates rallied, and an underweight to the United States relative to the benchmark.

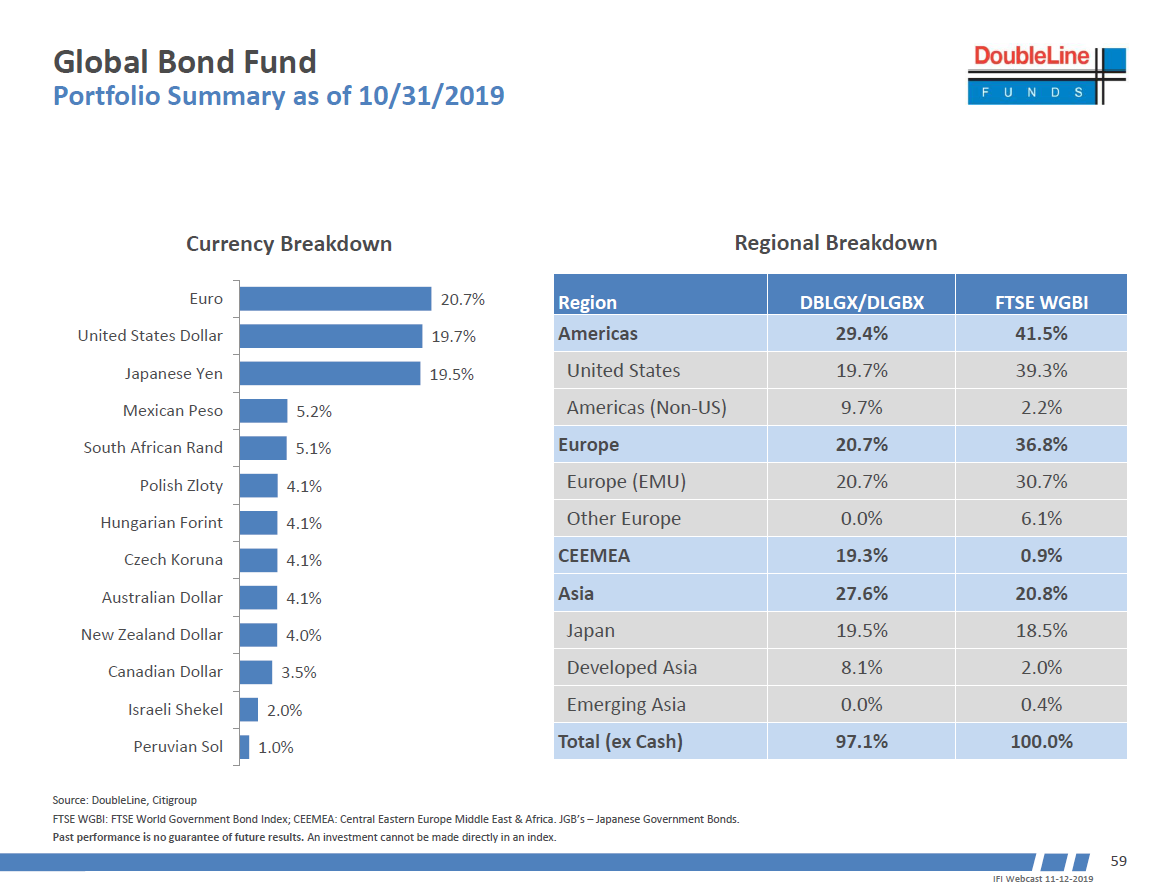

- Regionally, as of 10/31/2019, the Fund is underweight United States and Europe and overweight Central & Eastern Europe, Middle East and Africa (CEEMEA), Latin America, and Asia exposure relative to the benchmark.

Emerging Markets

- Positive returns for emerging market fixed income in 2019 have been driven by rallying global interest rates and emerging market credit spread tightening.

- Risks facing the emerging market asset class going forward.

- Global Growth Uncertainty

- Global Trade Negotiations

- China Growth Deceleration

- European Political Risks/ Brexit

- The case for emerging markets

- Secular Improving Credit Story

- Emerging markets real GDP growth continues to be double the pace of developed markets

- In 1999 26 of the JPM EMBI GD Index was investment grade, as of 10 31 2019 54 of that Index was investment grade.

- While we have seen slight weakening of fiscal balances as a percentage of GDP for both emerging markets and developed markets, the pace of theweakness has been more muted in Emerging Markets.

- Strong Credit Fundamentals

- Despite slowing growth, emerging market investment grade and high yield issuers have been able to keep corporate leverage ratios relatively stable and interest coverage ratios at relatively solid levels.

- Emerging market corporate leverage is at its lowest level since 2013.

- Net leverage of emerging market investment grade and high yield corporations remain lower than that of developed market corporations.

- Attractive Valuations

- As of 10 31 2019

- Emerging market investment grade corporates have a 38 basis points spread pickup versus U S investment grade corporates

- Emerging market high yield corporates have a 175 basis points spread pickup versus U S high yield corporates

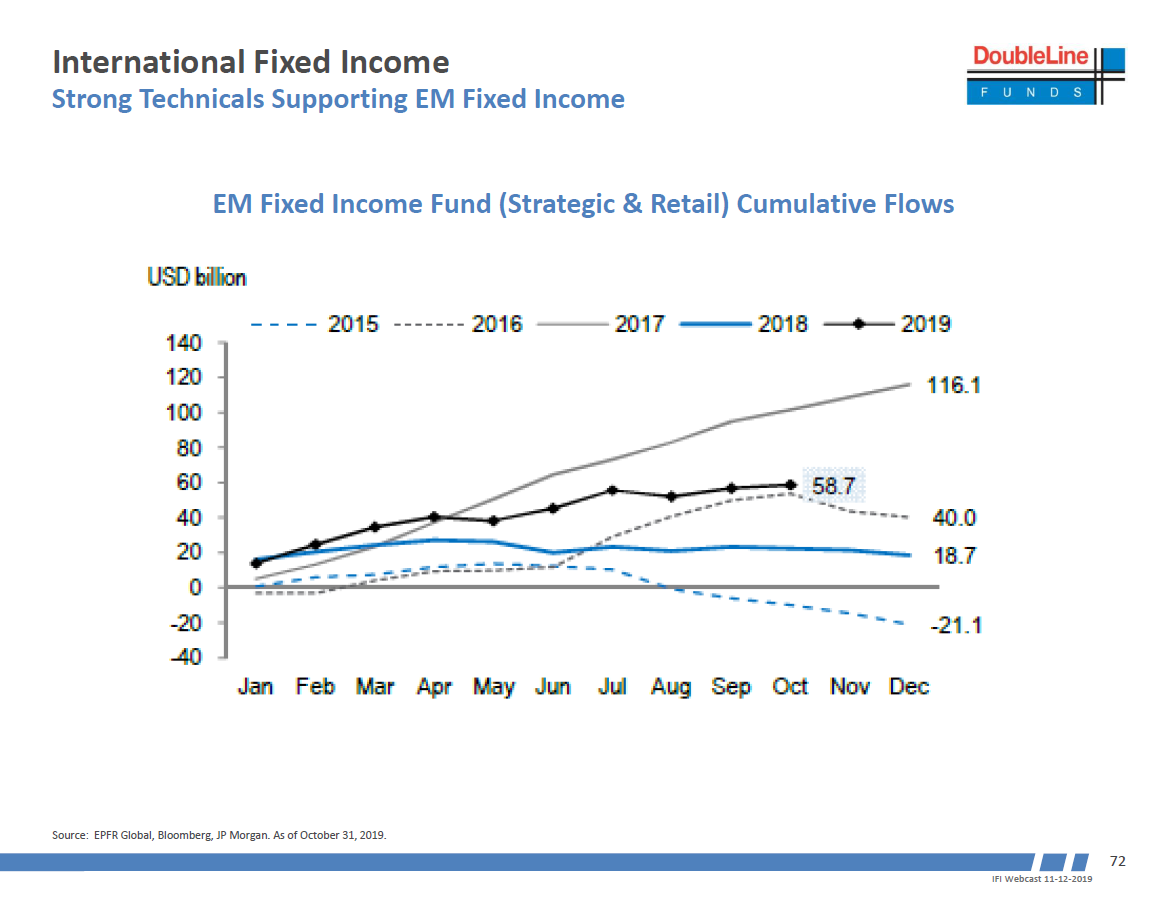

- Strong Technicals

- Year to date ( emerging market fixed income cumulative flows have rebounded strongly from a weak 2018 As of the end of October, cumulative flows were 58 7 billion for 2019 driven by investors searching for yield and wide credit spreads to begin the year, providing an attractive entry point.

- YTD gross issuance and net financing in emerging markets fixed income have both exceeded most expectations so far this year.

- Secular Improving Credit Story

Idiosyncratic Emerging Market Country Risks

All of these idiosyncratic risks lead the DoubleLine Emerging Market Fixed Income team to avoid some countries all together, such as South Africa and Turkey, while also looking for opportunities if some of these situations start to stabilize, such as in Chile, Ecuador and Peru.

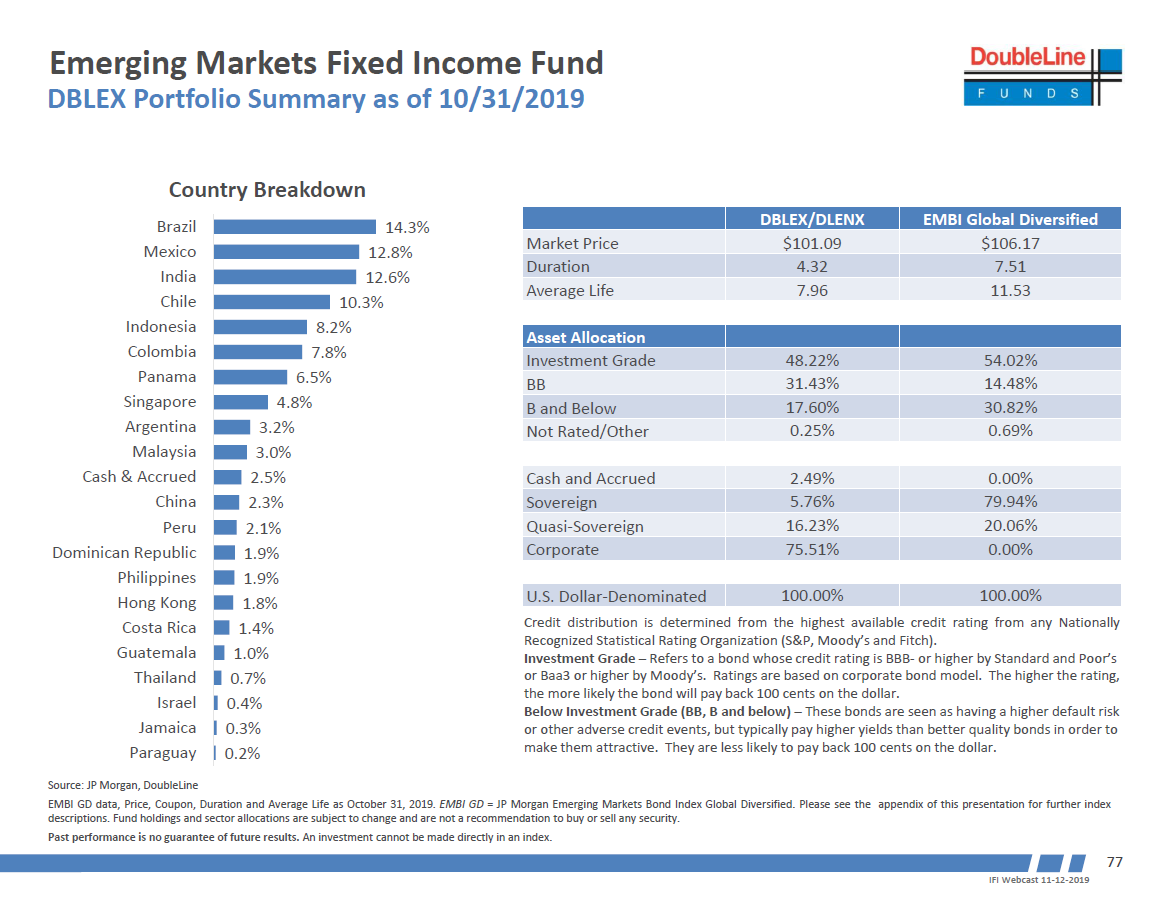

DoubleLine Emerging Markets Fixed Income Fund (DBLEX) Review (As of 10/31/2019)

- The Fund invests in 21 countries, with Brazil, Mexico, India, Chile and Indonesia being the top 5 holdings.

- Duration of 4.32 years

- 48.3% Investment Grade

- 49.1% High Yield

- Top 5 sectors: Banking, Oil & Gas, Utilities, Telecommunications & Transportation

DoubleLine Low Duration Emerging Market Fixed Income Fund (DBLLX) Review, (As of 10/31/2019)

- The Fund invests in 20 countries, with Brazil, Mexico, Colombia, China and India being the top 5 holdings.

- Duration of 1.65 years

- 72.4% Investment Grade

- 26.4% High Yield

- Top 5 sectors: Banking, Oil & Gas, Sovereign, Telecommunications &Transportation