We recently presented our investment thesis on KAR Auction Services (KAR) at ValueX Vail. Aside from a “leisurely hike” up the mountain at 10K feet after starving myself for three weeks, and a torturous spin class with our new Chief of Staff, this is always my favorite trip of the year. Click on the image below to learn more about Frankenstein, review statistics on horse manure and the transition from junk to gold.

Q1 hedge fund letters, conference, scoops etc

Peak Car

Nothing is as painful to the human mind as great and sudden change. – Mary Shelley, Frankenstein

A little bit more about auto auctions

KAR Auction Services is a holding company for two high quality auction businesses that operate in attractive duopolies. In 2018, KAR facilitated the sale of ~ 6 million used and salvage vehicles.

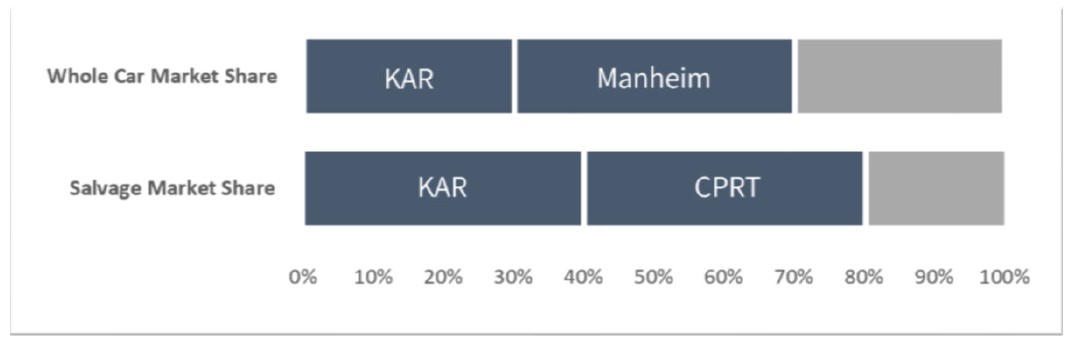

- The first segment we’ll discuss today is Insurance Auto Auctions or IAA. IAA is the second largest provider of salvage auctions services. These vehicles are typically older, damaged vehicles that are largely sold by insurance companies. IAA and Copart represent ~ 80% of the market.

- The second segment we’ll discuss today is ADESA. ADESA is the second largest provider of used vehicle auction services. Vehicles at these auctions are typically purchased by dealerships. The industry is highly consolidated with ADESA and Manheim (a subsidiary of Cox) representing ~ 70% of the North American market.

- KAR also provides floorplan financing to dealerships through a wholly-owned subsidiary called AFC. AFC earns a majority of its revenue from fees on short-term loans. Since this is a relatively small piece of the business – less than 10% of sales – in the interest of time, we are going to focus on the economics of both auction businesses today.

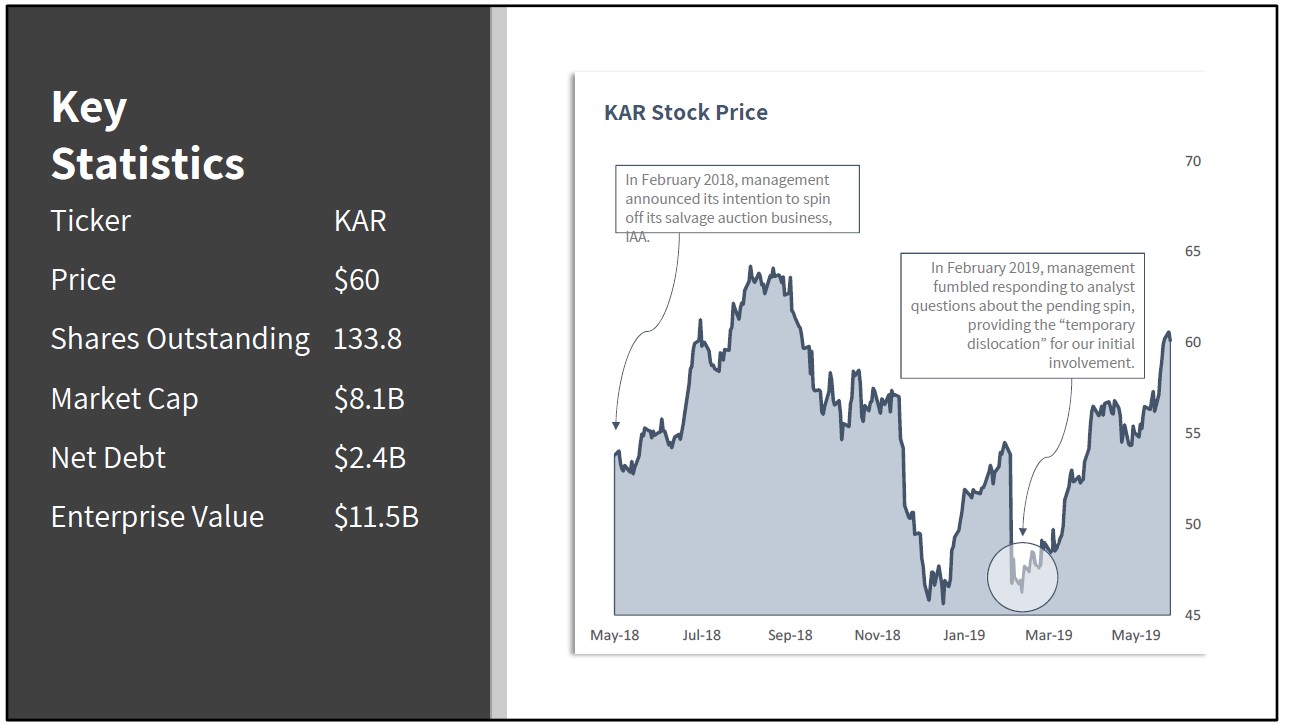

In February 2018, management announced its intention to spin off its salvage auction business, IAA. We think this is the catalyst to unlock significant near-term upside.

In February 2019, management fumbled responding to analyst questions about the pending spin, providing the “temporary dislocation” for our initial involvement.

Investment Thesis

- This is a good business with attractive industry dynamics – high margins and low capital intensity generate strong, recurring free cash flow and high returns on capital.

- Pending spin-off of IAA should unlock significant market value in the salvage auction business which trades at a ridiculously large discount to Copart.

- While the undervaluation of IAA is largely appreciated by the street, we think the real story here is uncovered by following management incentives.

Our investment thesis can be boiled down to three simple points:

1) This is a good business.

2) The pending spin should unlock significant value.

3) Management actions signal long term upside in the used auction business.

This is a good business

- KAR runs two separate and distinct auto auction businesses with a number two position in both oligopolies.

- The industry boasts high barrier to entry – zoning requirements make entry into this business very difficult.

- The auction business is a fee-based model with minimal working capital requirements, low capital intensity and strong cash flow.

Auto auctions benefit from attractive industry dynamics characterized by:

- Attractive oligopolies with no other major competitors.

- High barrier to entry, with strong network effects.

- A fee-based business model with no inventory risk.

KAR runs two auto auction businesses with a number two position in both oligopolies. There are no other major competitors besides KAR & its main competitor (Manheim in whole cars, Copart in salvage) in both segments.

KAR runs two auto auction businesses with a number two position in both oligopolies. There are no other major competitors besides KAR & its main competitor (Manheim in whole cars, Copart in salvage) in both segments.

See the full report here.

Article by Christopher Pavese, Broyhill Asset Management