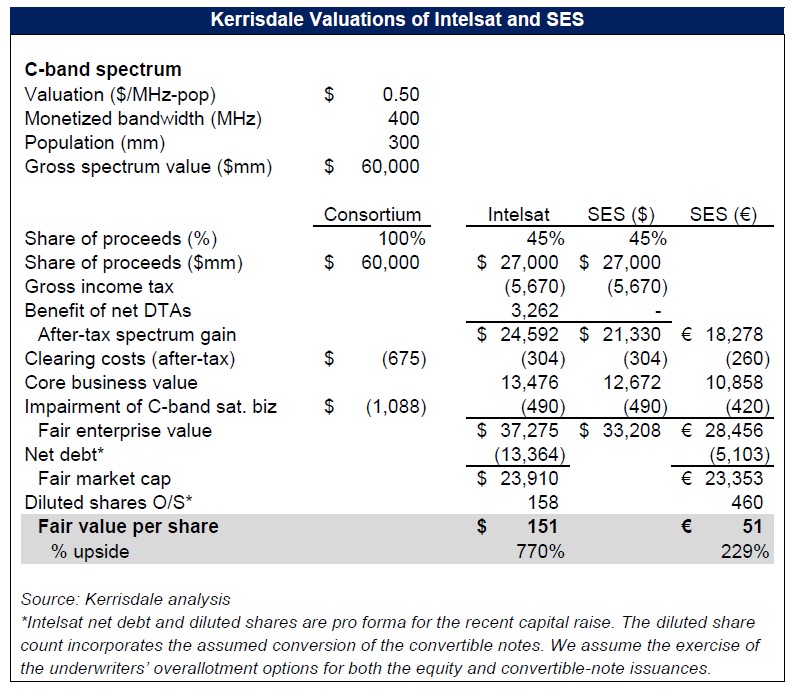

We are long shares of Intelsat and SES, two large satellite operators with significant and underappreciated 5G spectrum assets. For us, this is an unusual position to be in. For years, with our reports on Globalstar (2014), Straight Path (2015) and DISH (2016), we have publicly railed against the excesses of spectrum hype. Time and again, we have argued, equity investors have gotten carried away with their enthusiasm about offbeat frequencies and futuristic technologies, ignoring inconvenient details and weak business cases. But this time, it’s different. Intelsat and SES hold the keys to the right frequencies, in the right way, at the right time, without the irreconcilable interference issues that have beset other spectrum stories. The value they stand to reap is staggering: ~$60 billion. Intelsat is worth $151 per share, and SES, €51.

[activistinvesting]

Q1 hedge fund letters, conference, scoops etc, Also read Lear Capital: Financial Products You Should Avoid?

The spectrum in question is called the C band. This set of frequencies, used by certain geostationary satellite systems operated in the US almost entirely by Intelsat and SES, consists of two pieces: 3.7-4.2 GHz (for transmission from space to earth) and 5.925-6.425 GHz (for transmission from earth to space). The former band, 3.7-4.2 GHz, is now under consideration by the FCC for allocation to mobile use in addition to satellite use. Around the globe, spectrum in and around this range is emerging as the primary domain of 5G. With an ideal mix of ample bandwidth, good coverage (especially using the 5G technology known as massive MIMO), and international harmonization, the C band has been described as the spectral “sweet spot” for widespread 5G deployment. Whoever gets their hands on the spectrum first will immediately obtain a massive leg up on the competition.

Today, however, the C band isn’t just lying fallow: it’s a critical conduit between the creators of TV content, like Disney and Fox, and the distributors of TV content, like Comcast and DirecTV. To optimize the difficult transition from primarily satellite use to primarily mobile use, Intelsat and SES have proposed a clever and elegant solution: let the market decide. US C-band satellite operators, acting as a consortium, will effectively auction off portions of the band to mobile carriers like Verizon and AT&T; if the price is right, Intelsat, SES, and perhaps a few much smaller peers will roll up their sleeves and work with incumbent users to free up the spectrum. This market-based approach not only appeals to the FCC’s ideological bent; it’s also eminently practical, liberating meaningful amounts of bandwidth in a short period of time and helping the US win the so-called race to 5G. In our view, the Intelsat/SES proposal is by far the leading contender for C-band reform – a high-probability base case, not a longshot.

Based on recent international and domestic comps, we believe US C-band spectrum is worth at least $0.50/MHz-pop – valuing the entire band at roughly $75 billion. To seize an opportunity of this magnitude, Intelsat and SES would move heaven and earth. But they won’t have to. Based on realistic assumptions, we show that they can monetize roughly 400 MHz over 5-10 years, chiefly by rearranging channels across satellites and using up-to-date video encodings, all at a reasonable cost. It’s not rocket science, but shares in Intelsat and SES are set to launch.

I. Executive Summary

The Intelsat/SES plan for the C band will prevail. It’s abundantly clear that the FCC, in alignment with the Trump administration and the cellular industry, wants to see a material portion of the C band repurposed for 5G – and fast. Byzantine auction rules hammered out through round after round of lawyerly debate aren’t going to cut it. Only Intelsat and SES are in the right position to understand the nuances of current C-band usage and cost-effectively manage the transition to 5G; without their cooperation, the process will bog down. That’s why last week’s first step in the rulemaking process prominently featured the Intelsat/SES proposal and former opponents to the consortium’s plan keep preemptively modifying their own schemes to more closely resemble it: everyone can sense which way the wind is blowing.

While commentators often treat the Intelsat/SES plan as shockingly novel and thus unlikely to sail through, the history of FCC policymaking clearly indicates otherwise. Time and again, reformers have proposed reallocating underutilized spectrum to its highest and best use by simply giving incumbent licensees flexibility to sell off their rights and keep all of the proceeds.

These reformers are now in charge. In fact, they’ve been gaining influence for many years, even under Democratic administrations: the recent 600MHz incentive auction, for instance, was another product of the same underlying philosophy. From the perspective of mainstream

market-oriented spectrum wonks, the Intelsat/SES proposal is just common sense.

The C band is extremely valuable. Armed with 5G technology and ~160 MHz of Sprint’s 2.5- 2.7GHz spectrum, T-Mobile believes it can increase its users’ average download speeds by a factor of 15 over the next several years, creating a “world-leading, nationwide 5G network with more capacity than any network in existence today.” Intelsat and SES’s similar C-band spectrum offers the exact same potential but with even more bandwidth – a king-making asset that will be in high demand.

Recent auctions of C-band and adjacent spectrum in the UK, South Korea, and Australia have garnered intense interest from large carriers and valued the spectrum at $0.17-0.38 per MHz- pop. Notably, C-band prices have often exceeded prices for more familiar, lower-frequency cellular spectrum in the ~2GHz range. Since spectrum prices in the US have always been multiples of those in other developed countries, and since C-band spectrum using 5G massive MIMO can likely perform about as well using conventional cell towers as, say, Sprint’s spectrum, it’s easy to argue that the US C band should trade at or above $1/MHz-pop. Such a price is probably too high for the carriers to afford, but, even after applying a large discount, the C band will still generate tens of billions of dollars for Intelsat and SES – a valuation range that T- Mobile, for one, has directly endorsed.

Extensively repacking the C band is operationally and economically feasible. Is it actually possible for incumbent C-band users to condense themselves into just ~100 MHz of spectrum over time? We undertake a detailed satellite- and transponder-level analysis of current C-band activity to show that Intelsat and SES have many opportunities (given the right incentives) to do more with less spectrum. At a high level, for instance, fully upgrading to the latest compression techniques would ultimately enable all existing C-band video channels to coexist using less than 20% of aggregate satellite capacity. While extensively rearranging the mapping of video channels to satellite transponders will take time, effort, and negotiation, it’s clearly within the realm of possibility. Nor will the costs be astronomical: we estimate that even generous forecasts for installing improved receiver equipment and interference-mitigating filters will come in at less than a billion dollars.

Intelsat and SES are dramatically undervalued. With enormous embedded spectrum value than can be extracted at a reasonable cost and in reasonable time, Intelsat and SES should trade toward their fair values of $151 and €51 per share, respectively, over the next few years.

II. Company Overviews

Intelsat and SES are two of the world’s largest satellite service providers, with 30% combined market share in the commercial Fixed Satellite Services (FSS) sector (based on total 2018E FSS-sector revenue). The companies each own and operate fleets of over 50 geosynchronous equatorial orbit (GEO) satellites, primarily using frequencies in the ranges known as C band, Ku band, and Ka band. (SES’s wholly owned subsidiary, O3b Networks, also owns 16 medium- earth-orbit satellites.) Intelsat and SES use their satellites to provide a wide range of communications solutions to media companies, telecom operators, multinational corporations, and government agencies.

In areas where terrestrial telecommunications are unavailable or not cost-effective, satellite data networks form a critical layer of communications infrastructure – especially in emerging markets, the source of roughly a third of Intelsat and SES’s revenue (source: 2017 annual reports) and the target of 54% of Intelsat’s current capacity. Another key use case for GEO satellites is media (particularly TV) distribution, which accounts for 40% of Intelsat’s and 68% of SES’s revenue. GEO satellites allow video programming transmitted from a single point in space to blanket large coverage areas on earth, thereby simultaneously reaching multiple distributors, including cable companies and over-the-air broadcasters, which then re-transmit the signals out to consumers. Beyond emerging markets and media, mobile use cases – like providing broadband connectivity to cruise ships and commercial aircraft – have recently emerged as key sources of industry growth.

Historically, the FSS business was financially attractive, enjoying long-term contracts, high renewal rates, stable pricing, high EBITDA margins (75%+), mid-single-digit growth rates, and robust returns. This financial profile is what gave SES its traditional reputation as a “defensive growth” stock and what enticed private-equity sponsors to execute a leveraged buyout of Intelsat in 2008, saddling the company with high debt levels.

Over the last 3-4 years, however, the competitive landscape has transformed. First, the proliferation of new high-throughput satellites (HTS) has created excess capacity in some regions, leading to price declines for traditional data services. (Unfortunately, Intelsat’s own HTS fleet got off to a disappointing start because of these trends.) Second, as fiber-based terrestrial connectivity has become more common and less expensive, it has reduced demand for

satellite-based connectivity. Third, the growth of “over the top” internet video services like Netflix has eroded the value of traditional linear TV, a major source of satellite-industry revenue. This confluence of pressures has led to higher customer churn, lower prices, and lower volumes.

These problems are well documented and widely discussed. The tide may be turning, however. In Intelsat and SES’s core businesses, there are early signs of improvement. Intelsat’s free cash flow is set to increase as the company reduces capital expenditures while still maintaining its launch schedule; meanwhile, the company’s revenue trends are improving thanks to industry- wide pricing stabilization and the benefit of newly deployed satellites. For SES, underlying revenue growth already returned to positive territory in the first quarter of 2018, setting the stage for further improvement as more satellites enter service this year and next.

But, while we believe that investors do tend to undervalue Intelsat and SES’s core businesses, any upside from positive surprises on that front will be dwarfed by the upside from a source that, just six months ago, few market participants had ever considered: terrestrial use of the C band.

Article by Kerrisdale Capital

See the full PDF below.