L Brands (LB) is a specialty retailer whose primary brands are Victoria’s Secret and Bath & Body Works.

Q3 hedge fund letters, conference, scoops etc

The company’s 3rd quarter earnings release showed the following:

- 6% revenue growth versus the same quarter a year ago

- Adjusted EPS of $0.16 versus $0.30 for the same quarter a year ago

- Increased adjusted EPS guidance for fiscal 2018 to $2.70 from $2.58

- Reduced its dividend 50% from $2.40 to $1.20

On the positive side, an increase in adjusted earnings-per-share estimates for fiscal 2018 shows the company is doing better than it previously expected.

On the negative side, the dividend cut shows the company did not take its dividend seriously. The dividend was still covered by adjusted earnings, although a reduction was likely warranted to ive the company extra cash to pay down debt.

Key Metrics

Overview & Current Events

L Brands traces its roots back to 1963, when it was known as The Limited. On August 10th, 1963, The Limited opened its first store in Columbus, Ohio. The company went public in 1969, when it had five stores. By 1976, The Limited had opened 100 stores and in 1982 the company purchased Victoria’s Secret for $1 million. Today, L Brands is a specialty retailer with a variety of brands including the flagship Victoria’s Secret, as well as PINK, Bath & Body Works, La Senza, and Henri Bendel. The company operates more than 3,000 company-owned specialty stores and 800 franchised locations around the world. The $9.3 billion market cap business is on pace to generate $13 billion in revenue this year.

On September 13th, 2018 L Brands announced that it would be closing all 23 Henri Bendel stores and the e-commerce website in January 2019 (2018 revenues and operating loss are expected to be $85 million and $45 million respectively).

In addition, on October 11th, 2018 L Brands said it would be “exploring all alternatives” for its La Senza business.

On November 19th, 2018 L Brands announced Q3 2018 results. Revenue came in at $2.775 billion, a 6% increase compared to the prior period. The company reported a $0.16 per share loss for the quarter due to a $20.3 million cash charge related to the closure of the Henri Bendel business and an $80.9 million non-cash charge related to Victoria’s Secret store assets. Excluding these charges, adjusted earnings-per-share came in at $0.16 against $0.30 in the year ago period. The company provided fourth quarter earnings-per-share guidance of $1.90 to $2.10 and full year adjusted earnings-per-share guidance of $2.60 to $2.80, up from $2.45 to $2.70 previously.

In addition, the company announced a 50% dividend cut from $2.40 per share down to $1.20.

Growth on a Per-Share Basis

From 2007 through 2015 L Brands put together a commendable record, growing earnings-per-share by 10.6% per annum. However, since the peak in 2015, earnings are now anticipated to be ~36% lower per the mid-point of management’s guidance.

L Brands faces a bevy of concerns including the decline in mall traffic, being late to e-commerce, changing body image views, aggressive advertising without increased traffic, the rise in online shopping and two CEO departures (from the Victoria’s Secret and PINK segments). Further, the dividend has been halved to $1.20 per share.

On the positive side, closing the unprofitable Henri Bendel business and potentially selling the La Senza segment could help L Brands focus on its Victoria’s Secret and Bath & Body Works core (which together already make up ~90% of sales). Further, the dividend cut is bad news for current income investors but ought to help the company deleverage its balance sheet moving forward. We believe it was a necessary move.

Valuation Analysis

Given the uncertainty around L Brands businesses (with a specific nod to mall traffic and e-commerce competition) we are not comfortable awarding the security a premium multiple. While the share price is down more than 60% since the end of 2015, earnings-per-share have declined by a significant amount as well. We have assigned a fair value P/E ratio of 14.0 to account for the company’s difficulties, well below its historical average P/E of 17.0.

Moving forward the new dividend should provide a reasonable, albeit now much lower, income stream. We find L Brands to be a cautionary dividend tale in the face of high debt and a high payout ratio coupled with declining earnings.

Safety, Quality, Competitive Advantage, & Recession Resiliency

L Brands took a drastic step to work on its balance sheet – cutting the dividend by 50% from $2.40 per share down to $1.20. This should free up ~$325 million annually to work toward deleveraging the balance sheet. We’re hopeful that this will come to fruition, but naturally we are waiting to see progress in this area. In the interim, the company still has debt payments of ~$400 million per year against underlying earnings power of ~$750 million. Should a downturn come sooner rather than later, further dilutive action may need to be taken.

L Brands earnings-per-share declined 66% from 2007 to 2008. The company is not recession resistant. If earnings-per-share were to take a similar plunge again, the dividend would not be covered by earnings, even at the new lower rate.

Final Thoughts & Recommendation

L Brands has many headwinds and unknowns at the moment – namely, closing segments, lackluster results in its flagship brand, a high debt-load and a trend away from malls. We rate L Brands as a hold at current prices.

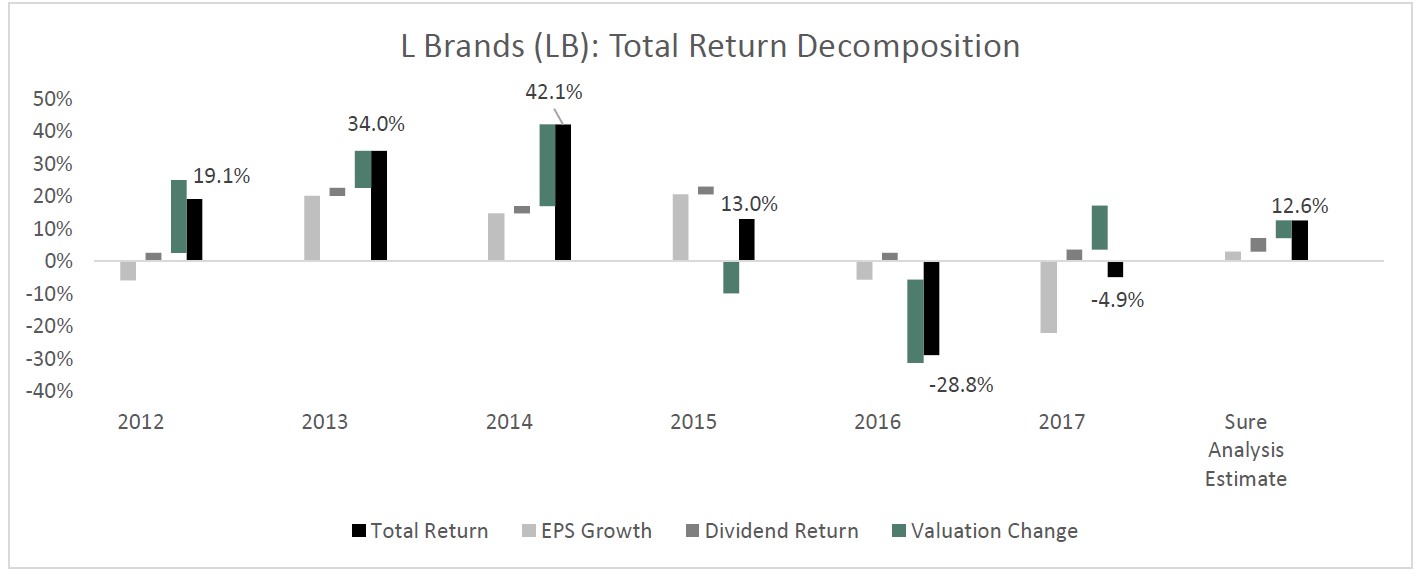

Total Return Breakdown by Year

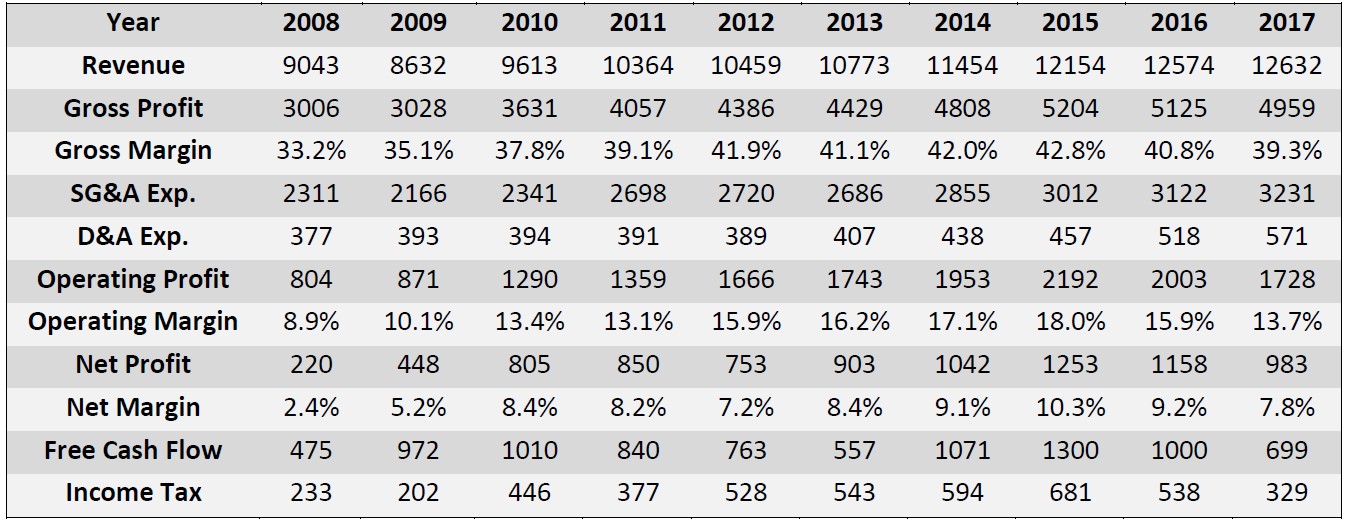

Income Statement Metrics

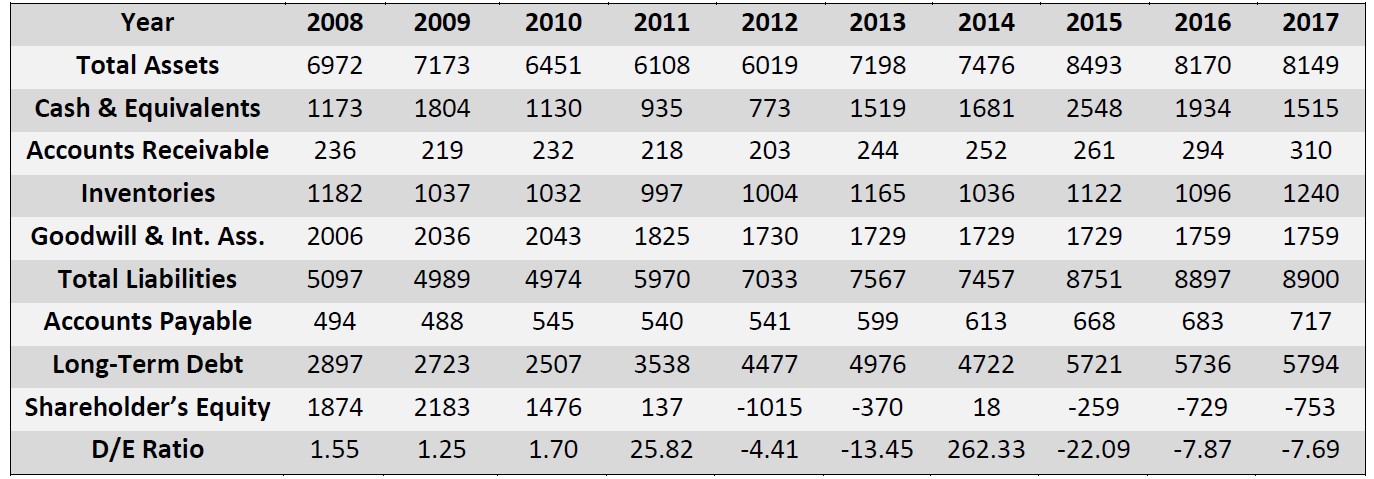

Balance Sheet Metrics

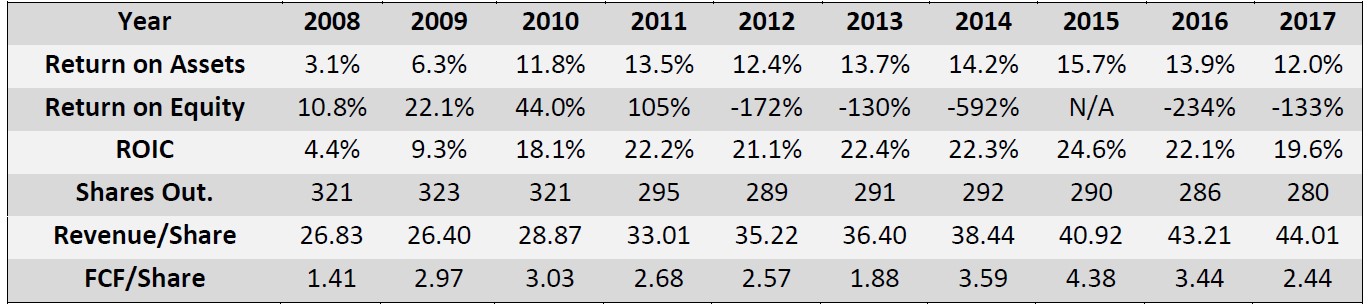

Profitability & Per Share Metrics

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.