The first score of the century is in the history books. It was the best and worst of times, but in the reverse order. The lost decade was followed by the longest bull market in history. Overall, it was not so good for U.S. stocks, downright bad for international stocks and outstanding for high-quality bonds.

Q4 2019 hedge fund letters, conferences and more

Let’s walk through the first 20 years of the new millennium and the lessons for the next 20 years.

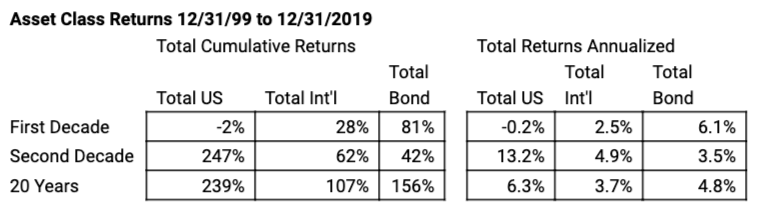

Those 20 years came in as follows, based on total returns including dividend reinvestments:

These results use the broadest index funds, after fees. I used the more expensive investor class Vanguard funds as 20 years of history is available only for these funds. Actual returns would have been a tad better using lower-fee Admiral funds or ETF share classes when they became available.

From the dawning of the new age economy to the bursting of the dot-com bubble

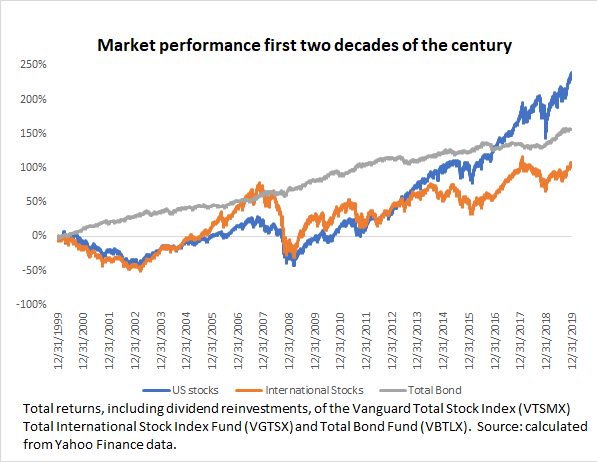

The century began with the widely held belief that we were in a new era where cash-flow no longer mattered. Internet companies with little revenue and huge losses had valuations in the tens of billions of dollars. Critics of those valuations were scolded for their old-school thinking and failure to understand that things were different in the new economy. U.S. stocks peaked on March 24, 2000, and quickly plunged by nearly 50%. Many thought this would be the most painful period of the century, but it was only the first plunge of that decade.

Clients came to me bewildered. How could they have lost over 70% of their stock portfolio when they owned several mutual funds they thought were diversified? The answer was obvious; example were the several Janus mutual funds that all owned the same dot com companies. A total-stock index fund was far more diversified. High-quality bonds, REITs and precious metals and mining stocks had low to negative correlations and did well during this bear market. The plunge ended in in October 2002, and though U.S. and international stocks had each lost about 49% of their value, high-quality bonds helped ease the pain, gaining 28%.

The real estate and financial bubble

The pain of the dot com bubble was soon forgotten as stocks soared to new heights. This time, the bull wasn’t based on billion-dollar IPOs with little revenue – it was real, as in real estate. You can’t print more real estate, right? If people default on mortgages, they are secured by real assets and real estate goes up in value. Between October 2002 and March 2007, U.S. stocks gained 133% and international stocks gained 240%. Bonds lagged, gaining only 22%.

Back then, I told clients a third of their equities should be in international stocks and the typical response was “why only a third – isn’t all the growth coming from overseas? We want whatever is hot.”

This bubble burst and was many times more painful than the earlier plunge. The magnitude of the decline was only slightly more than the dot com bubble, with U.S. stocks losing 55% and international dropping 60%. What made it so much more painful was that it burst twice as fast as the last bubble, making it far more vivid. In a stroke of bad luck, I happened to be in New York near Wall Street on the bloodiest week in October 2008, where the fear was contagious.

Total bond funds hung in, gaining over 7%, but Morningstar reported that the average bond fund in 2008 lost 8%. In fact, many bond funds lost more than stocks. And those REITs and precious metals and mining stocks that worked so well when the dot com bubble burst failed miserably during this plunge. Every plunge has its own cause and effect.

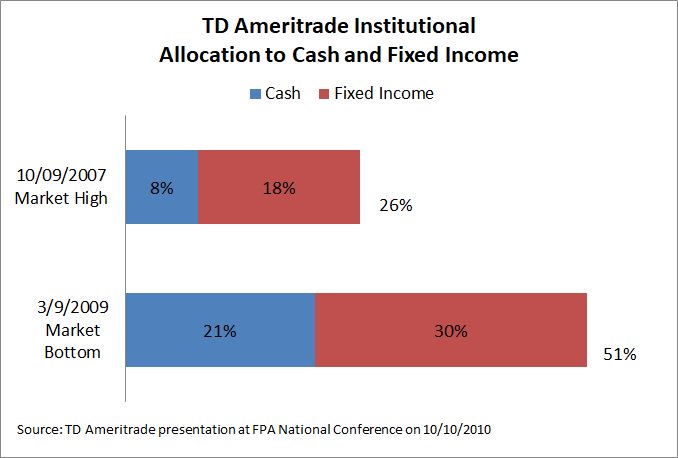

A critical role of financial advisors is to keep their clients disciplined with a relatively stable asset allocation between risky assets (stocks) and low-risk assets (bonds and cash). But advisors timed the market poorly. T.D. Ameritrade Institutional accidentally disclosed allocations on its advisor platform. The average allocation to risky assets was 74% at the height of the market on October 9, 2007 and only 49% at the bottom on March 9, 2009. “My client made me get more conservative” was an excuse I often heard from advisors.

Read the full article here by Allan Roth, Advisor Perspectives