Spruce Point Capital Management is pleased to issue a report on their website outlining their concerns how LHC Group, Inc. (“LHCG”) faces 35% – 65% downside risk to approximately $60-$90 per share.

Q4 2019 hedge fund letters, conferences and more

Through forensic accounting and a close analysis of company filings, Spruce Point finds evidence that performance at Almost Family (“AFAM”) – another home health service provider with which LHCG conducted a merger of equals in 2018 – has seriously deteriorated since the acquisition. With AFAM now seemingly experiencing negative sales growth, Spruce Point also observes signs that management is taking measures to obfuscate this contraction, and to avoid including AFAM in its calculation of company-wide organic growth. We believe that the market misunderstands LHCG’s true growth profile as a result, and harbor serious doubts as to management’s credibility and the continued viability of its roll-up strategy.

Executive Summary

Short LHCG: Spruce Point Sees 35%-65% Downside to $60-$90 per Share

LHC Group (“LHCG” or “the Company”) is a roll-up of post-acute home health centers which, in Apr 2018, completed a transformative merger of equals with fellow home health services provider Almost Family (“AFAM”). The merger was pitched to investors as a highly-synergistic deal which would produce a company capable of consistent mid-single-digit organic growth. However, Spruce Point’s forensic analysis of Company filings suggests that, whereas AFAM was expected to grow annually at 5-6% following the deal, the business is now contracting. At the same time, management appears to have taken steps to obfuscate AFAM growth and to avoid including it in organic sales, despite the fact thatthe deal closed ~21 months ago. With AFAM included in LHCG organic sales, as it should be, organic growth would fall from a reported ~7% to less than 2%. Meanwhile, surreptitious purchase accounting adjustmentsand questionable “one-time” acquisition-related chargeshave erased nearly 15% of the announced deal value. With LHCG’s true organic growth far below reported levels, and with management appearing to have serious problems integrating AFAM into LHCG, we question not just LHCG’s reported organic growth and adjusted earnings figures, but the continued viability of management’s roll-up strategy itself –and, consequently, the growth-driven narrative underpinning the bull case for the stock.

- AFAM Appears To Be Contracting:Disclosures regarding acquired inorganic revenue imply that AFAM has severely underperformed both Company and sell-side expectations. We estimate that AFAM revenue is now contractingafter it was first expected to grow 5-6% per year. Management appears to avoid reporting AFAM growth, orhas cherry-picked unrepresentative metrics which superficially project the appearance of improvement.

- Management Jumping Through Hoops To Flatter Organic Growth?:Management excludes AFAM from organic sales even though it was acquired ~21 months ago. This omission inflates reported organic growth by ~500 bps, from less than 2% to ~7%. Selective divestments of underperforming locationsalso inflate reported organic growth. This has saved a key LHCG metric –one followed closely by sell-side analysts –from collapsing at the hands of AFAM headwinds.

- The Cause –Bungled Integration? Or Customer Reallocation?:AFAM throughput appears to have suddenly collapsed immediately after the deal’s closure, andhas since fallen more than 30% below pre-deal levels. Throughput at legacy LHCG locations has simultaneously expanded by close to 10%. Could AFAM’s apparent contraction be explained by the cannibalization (purposeful or not) of AFAM locations by legacy LHCG locations? If so, LHCG’shigh single-digit reported organic growth is being supported directly by cutbacks at locations not yet included in the organic base, which will inevitably weigh on organic growth once they are in fact included(as they should be already). We also find that, after claiming that the integration would be extremely swift, management has since subtly pushed forward its integration timeline on an almost quarterly basis. Today, more than two years after management first stated that the integration was already nearly complete, it is stillin the process of integrating AFAM into LHCG’s software, andhad integrated only about halfof AFAM locations by the end of last quarter. We harbor significant doubts as to the competence of LHCG management and the continued viability of its roll-up strategy given these apparent integration issues.

- Concerning Purchase Accounting Adjustments:Management appears to have gradually increased AFAM’s bad debt allowancefrom $27M to $65M, suggesting that nearly half of acquired AFAM receivables may be uncollectible. The post-M&A purchase accounting adjustment window may also be giving LHCG a chance to take effective asset write-downs which do not flow through the income statement, and, therefore, which do not hit earnings. This, combined with ~$67M worth of integration costs through ~2 years and counting, has destroyed over $100M of shareholder value for holders of LHCG, nearly 15% of the AFAM purchase price.

- We See 40%-60% Downside After Taking Into Account LHCG’s True Organic Growth, Earnings, And Business Risks:LHCG remains a popular “buy” among analystsenamored by the Company’s seemingly-robust organic growth profile and runway for tuck-in M&A, particularly following an Oct 31 update to Medicare’s Patient-Driven Groupings Model which was broadly perceived to be supportive of continued industry consolidation. Even then, the average analyst price target implies only 3% upside from current levels. Why should investors own stock in a Company which, in our opinion, misrepresents itsorganic growth profile by 500bps, and whose management cannot effectively carry out its strategy at large scale? We expect organic underperformance anddisappointing earnings to result in significant valuation compression from LHCG’s current 20.6x ‘20E EBITDA multiple–an all-time high for the stock.

Naive LHCG Bull Case vs. Spruce Point Findings

A close forensic investigation of LHCG’s underlying organic growth and true profitability profile leads us to have a far morebearish view on the Company than the bullish industry consensus, which remains blind to major issues with its performance, strategy, and management team.

Organic Growth Vastly Overstated Due To Omission Of Almost Family

Whether AFAM’s poor performance can be attributed to mismanagement or underlying flaws, Spruce Point believes that management’s omission of AFAM from LHCG organic sales after the merger’s anniversary datepresents a severely skewed view of LHCG organic growth.

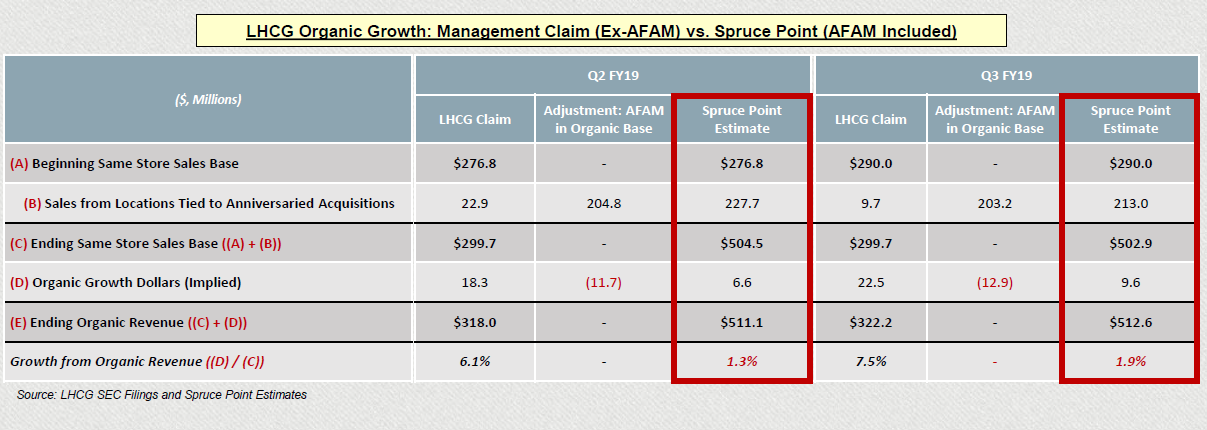

Whereas management reports that LHCG has grown organic sales by 6.1% and 7.5% in Q2 and Q3 FY19, respectively, its true organic growth rate is less than 2% when AFAM locations are included in the organic sales base –as they should be, with the acquisition having anniversaried in April of this year. Spruce Point estimates that, by excluding the contribution of Almost Family locations from organic growth, LHCG has inflated its reported organic growth by close to 500 bps in both Q2 and Q3.

LHCG Organic Growth Artificially Inflated By A Sudden (And Suspicious) Shift In Mix?

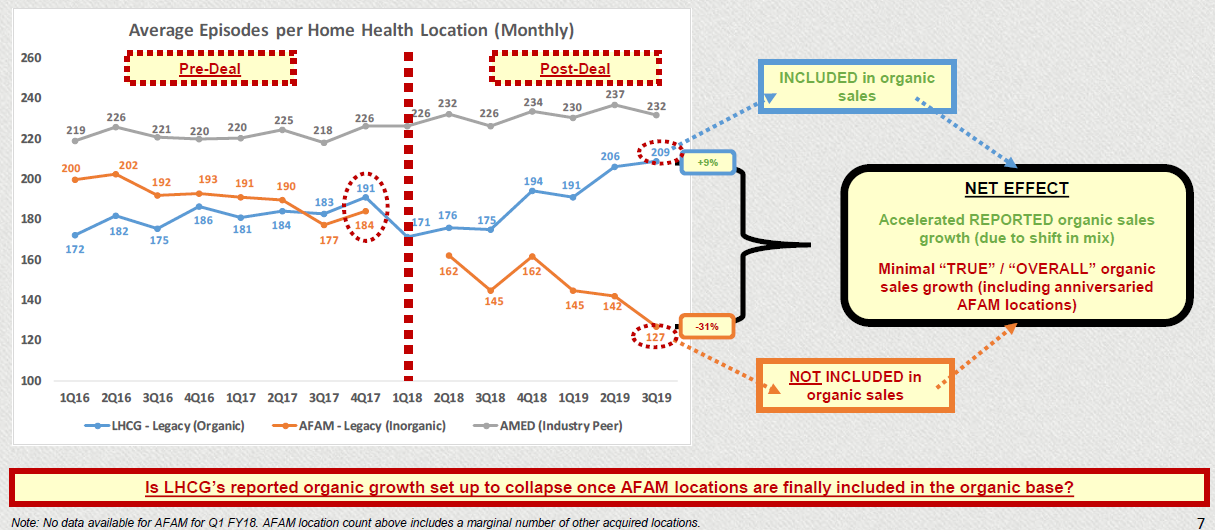

A close analysis of LHCG’s financial statements reveals a sudden and growing divergence between throughput at AFAM locations andlegacy LHCG locations. Immediately following the acquisition, home health episodes per location declined sharply among former AFAM locations, and have since fallen by 57 events per month (31%) from pre-deal levels. Meanwhile, average throughput among legacy LHCG locations has risen by 18 events per month (9%). Why did AFAM throughput fall so significantly following the acquisition, and, crucially, why has itcontinued to fall even as management moves closer towards completing the integration?

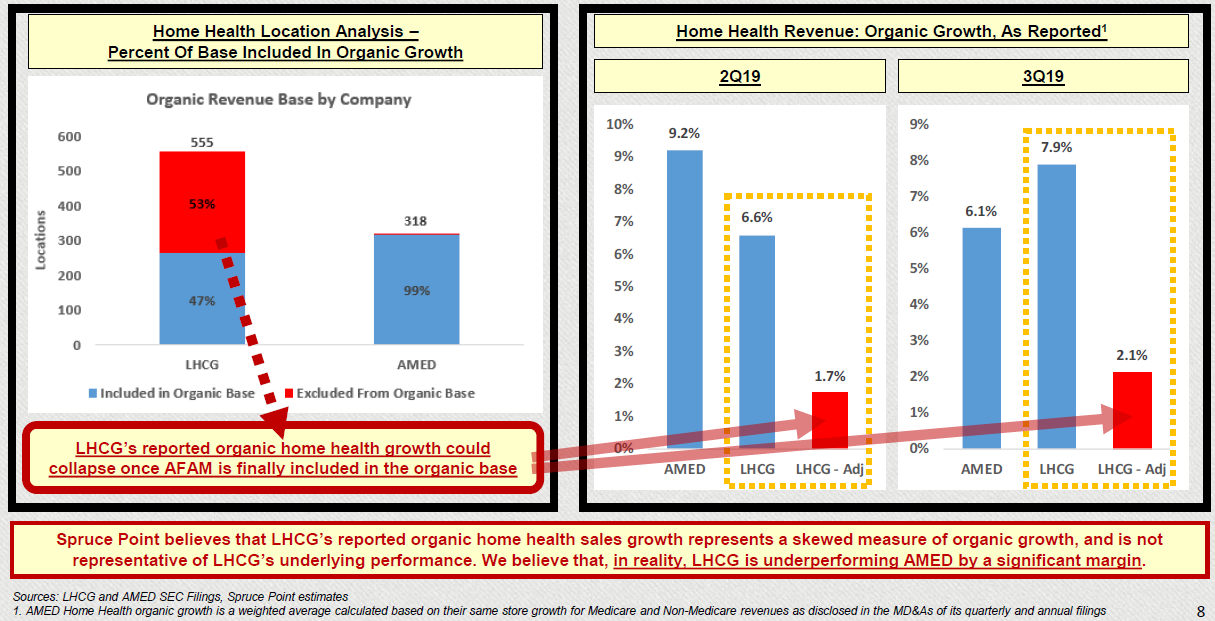

Importantly, as of Q3 FY19, LHCG has more locations excluded from organic growth (292) –the vast majority of which are AFAM locations –than it has organic locations (263). Accordingly, the contraction in throughput at AFAM –which is excluded from REPORTED organic sales growth –has a larger proportional impact on “TRUE” organic sales growth than does the increase in throughput at legacy locations. Theresult: “true” organic sales growth is far lower than management’s reported figure, which excludes more than half of its locations (and its worst-performing).

LHCG Organic Home Health Growth Is Not Representative Of Underlying Growth Rate

While LHCG reports levels of organic home health growth roughly on par with AMED, its closest peer, Spruce Point believes that LHCG’s organic home health growth figure is misleading as reported, and is not a meaningful reflection of underlying Company performance. Importantly, with management continuing to exclude AFAM from organic sales, LHCG’s organic base temporarily includes less than half of its total locations. Meanwhile, AMED’s organic base includes 99% of its locations, making its own reported organic home health growth figure a much stronger indication of sustainable sales growth. Including AFAM locations in LHCG’s organic home health growth calculation (as they should be) reduces LHCG organic home health growth in Q2 and Q3 2019 from 6.6% and 7.9% to 1.7% and 2.1%, respectively – far behind AMED’s reported figures.

Read the full report here by Spruce Point Capital Management