What an adaptive worldview means is that whenever you learn a new concept in an ill-structured domain, you know not to oversimplify — that is, to represent it as a single principle or concept. You do not try to reduce. You instead know to search for new, different cases in order to collect a cluster of prototypes in your head, and let that cluster inform your understanding of the concept. If you encounter a new case, you update the concept, because the concept is only useful when you know how it is instantiated in reality. ~ Cedric Chen via the post “Investing’s Big Blind Spot” by Tom Morgan

In this week’s Dirty Dozen [CHART PACK], we cover more recession signals, bullish price action in the main markets, a BIG set up in the US dollar, a major compression regime in bonds, and more…

Q1 2023 hedge fund letters, conferences and more

- Summary bullet points from BofA’s latest Flow Show with highlights by me.

- BofA is quite bearish… We think a recession later in the second half of this year is likely but excess consumer savings, amongst a few other cycle peculiarities, means the lead/lags this time around are not typical. So weak opinions weakly held.

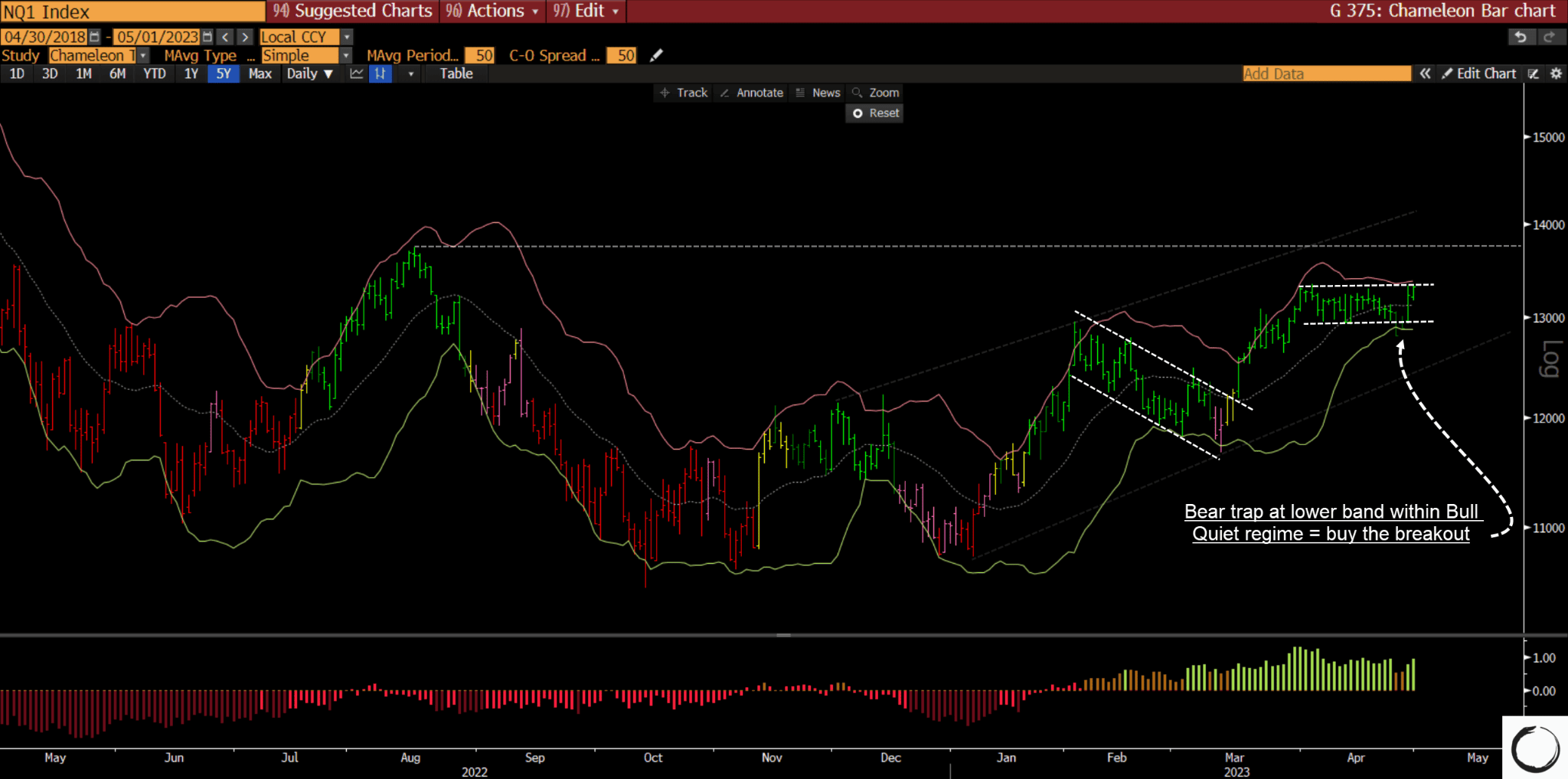

- Respect the tape… The Qs continue to trap bears and steadily rise in a Bull Quiet regime. This is not a tape you want to be short.

- Market internals present a mixed picture, neither overwhelmingly bearish nor strongly bullish. Semis and cyclical vs defense plus discretionary vs staples are trading weak to neutral while credit and the VIX curve support the uptrend.