Senior Investment Strategist Steve Lipper analyzes the recent decline through style, dividends, earnings, and cyclicals.

Q4 hedge fund letters, conference, scoops etc

Can you help us situate the latest decline in its historical context?

While there are many things about the decline in 2018 that might have felt abnormal, from our perspective actually it was pretty normal.

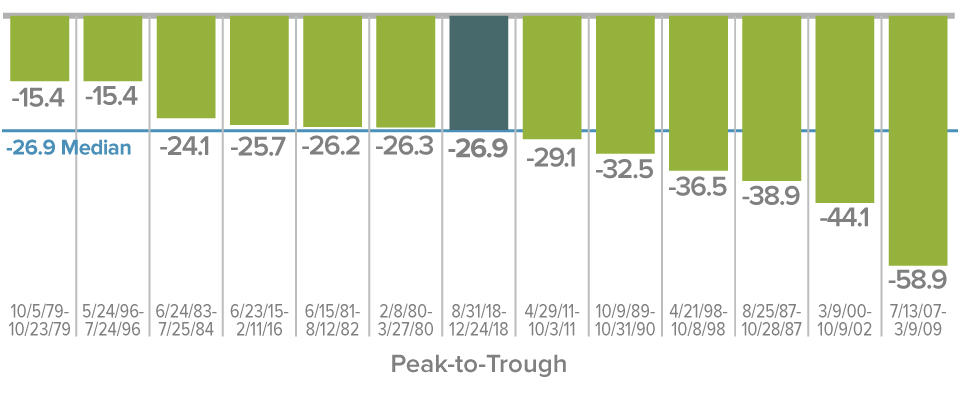

First let’s look at the depth of the decline. So in the 40-year history of the Russell, this is the 13th time we have had a decline of 15% or more. How does the decline in 2018 compare? It’s actually right in the middle of all 13. From a depth of decline standpoint, measuring from the peak at the end of August to the bottom of the decline so far towards the end of December, this is a pretty average decline.

If you’re looking for more timely hedge fund insight, ValueWalk’s exclusive newsletter Hidden Value Stocks offers exclusive access to under-the-radar value hedge funds and their ideas. Click here to find out more and signup for a free no-obligation trial today.

Current Decline Similar to Historical Median

Declines of 15% or Greater Since Russell 2000 Inception through 12/31/18 (%)

What factors also suggest that this was a typical decline?

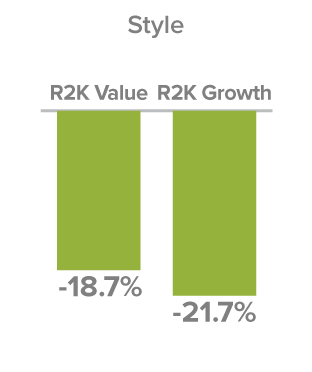

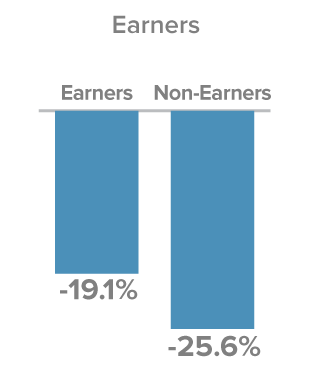

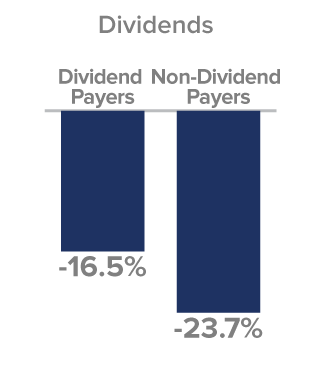

So we then looked within the market and contrasted different types of stocks and said, “Did they behave normally in a way we would expect?” and we looked at four different pairings. The first was value versus growth, and value did hold up better than growth in this decline, which is typical of most declines. Next we looked at companies that had earnings versus companies that didn’t have earnings. As you might expect and what happened this time, earners held up better than non-earners.

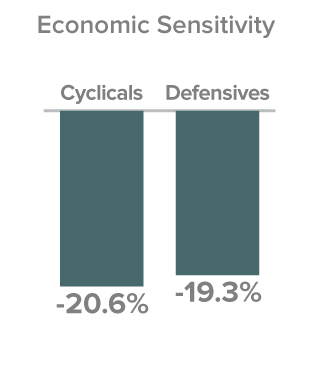

A Familiar Pattern in 4Q18 Decline

The next was a look at dividend payers versus non-payers, and dividend payers held up better than non-payers. And finally we looked at companies that were cyclical or in cyclical sectors versus companies in defensive sectors, and what you found was that cyclical did worse. Defensive held up better. This is not surprising because in market declines people get concerned about perhaps are we foreshadowing a recession, and they gravitate a little bit more to those stocks that are less cyclical. So across all four of those parameters—style, earners, dividend-paying, and cyclicality—the pattern we saw was consistent with history and what we would expect.

What does history suggest might be in store for small-cap stocks after this kind of decline?

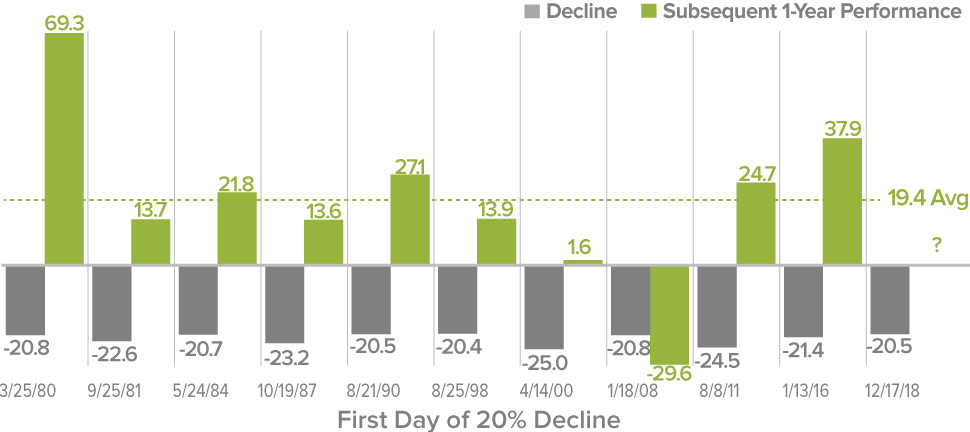

So when looking at history and saying, okay, this was a little steeper decline, 20% or more, how often have we had that, and what’s happened next? Well, this was the 11th decline since the beginning of the Russell. That’s been at least 20% since a prior peak. In nine of the previous 10, you’ve had a very substantial recovery over the following year. Actually, it’s averaged 19%. The one exception was 2007-2008, into 2009. So what we tell people is, if you think we’re headed to another great Financial Crisis, it’s probably not a great time to invest, but if you don’t think that that’s what’s coming—and here at Royce we don’t—history suggests this decline might be a good time to invest fresh money into small-caps.

After the Bear Market, Then What?

Subsequent 1-Year Performance of Russell 2000 after a 20% Decline as of 12/31/18

Article by The Royce Funds