“Davidson” submits:

[timeless]

Q2 hedge fund letters, conference, scoops etc

If it is going up, valuation goes out the window…NFLX.

Netflix (NFLX) is a good example of Momentum Investing on price trends without regard to valuation. 2 charts spell some of this out. Not shown is a proprietary study performed on the SP500 cycle from 2002-2008 (Recession-to-Recession) which showed that BV/Growth per share was the key driver to Price/Shr growth across a cycle when one used Recession Lows to factor out Momentum Investor enthusiasm. Momentum Investor optimism is low during recessions when prices become dominated by Value Investor psychology. The correlation of Share Price Growth to BV/Growth per share was ‘highly significant’ in the study. BV is another term for Shareholder Equity.

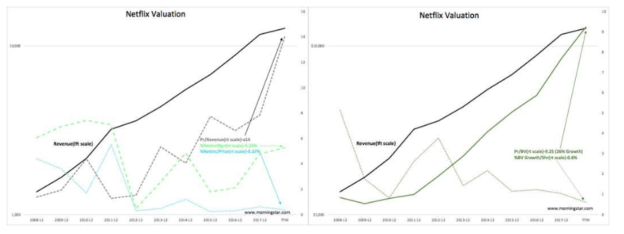

During market upcycles valuations often become justified by references to non-financial parameters simply because of the belief by many that market prices correctly incorporate all factors public and non-public efficiently. Eugene Fama received a Nobel Prize for his work on “Efficient Market Theory”. Netflix(NFLX) is a good example of Momentum Investing running to extreme valuation levels. NFLX’s Revenue has in fact grown rapidly from $1,365Bil to $12,575Bil and BV/Shr has risen from $0.85 to $9.25shr since 2008, 10yr Annual Revenue Growth ~25% and 10yr Annual BV/Shr Growth ~26%. Both are exceptional. Many ‘high-fliers’ have more ‘hat than cattle’.

The issue is what investors are paying for the growth of Shareholder Equity today? The Price/BV has risen to a multiple of 9.25 which reduces that ~26% growth of Shareholder Equity by that factor. The net effect is at current prices, new investors are buying NFLX at a 0.6% BV Growth rate.

If one performs a similar analysis on hundreds of company valuations, one will find the highest valuations on those companies most favorably mentioned in the media. Valuations of perfectly good performances as found at DHR are not comparable even though it is DHR-type of company which holds up across full market cycles than those more prized. This is the impact of market psychology during a long market upcycle.

Market psychology is what it is. One needs to be aware of how shares are priced vs. media attention and decide on how much market psychology risk one wants to assume in one’s portfolio.