“Davidson” submits:

Q1 2021 hedge fund letters, conferences and more

Headlines speak of rampant speculation in Bitcoin, meme-stocks like Game Stop and AMC, FAANG-type issues as indicating we are at or near a market/economic top, but market speculation is not economic speculation. Some believe that stock markets determine economic activity. They do not. Markets reflect economic activity after the fact! If one can identifies those economic indicators which forecast the topping of the economic cycle, then one can sort of predict the topping of markets in the next 6mos-12mos.

The basics of predicting markets and individual prices are best understood by recognition that prices are driven by market psychology after events or reports are known. There are many who believe prices confer what the future holds for prices. In my opinion, the truth is closer to fundamentals dictating the news headlines which in-turn dictates market psychology which finally dictates prices. How investors react to news and how often the same or similar news is repeated will drive prices higher/lower accordingly. If one grasps the underlying connections between economic and business fundamentals and prices, one can be 6mos-12mos ahead of prices, longer with deeper delves into long-term fundamentals. Sometimes one can be too early before market prices shift as expected, but better to be early than late.

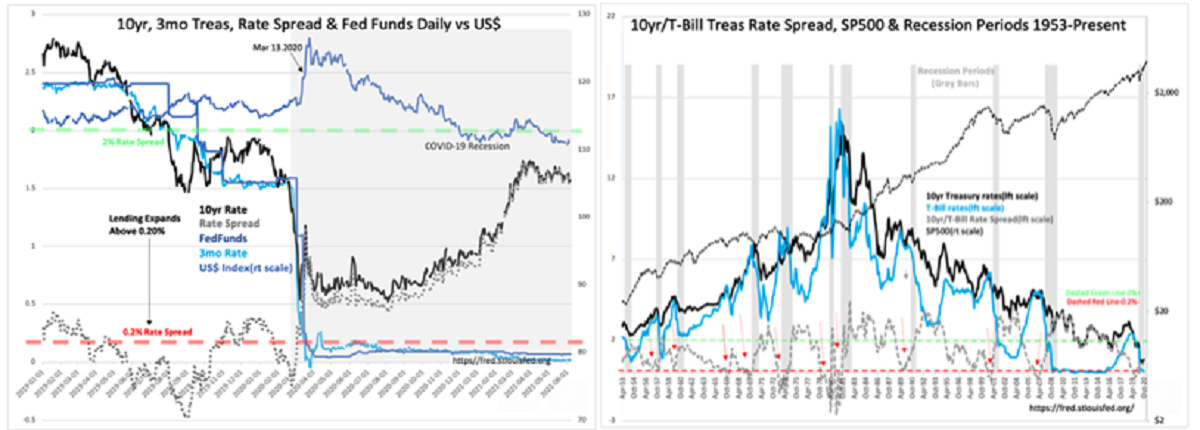

Among coincidental indicators which work reasonably well forecasting higher/lower equity prices is the T-Bill/10yr Treas Rate Spread(TB/TRS). Although this is always used in conjunction with Retail Sales, Employment, the Chemical Activity Barometer and a few others, the TB/TRS is one of the best in my experience if one knows the details of what it describes that makes it so useful as a market psychology indicator calling economic tops and bottoms.

The detail that TB/TRS reveals is capital shifts as the market cycle proceeds. In recessions, panic has flattened the TB/TRS such that T-Bill rates may even be higher than 10yr Treas rates. This is the feared inverted yield curve. It occurs because at economic tops investor enthusiasm become so optimistic that even the ‘safe money’ kept in T-Bills, i.e. Money Markets, has left its safe haven and become speculation. It is business speculation that drives T-Bill rates higher than the rate of the 10yr Treas. Bank and other financial institutions which have been lending for several years on a widening spread suddenly find it narrowed and lending slows markedly. Those projects which are more speculative suddenly cannot expand into profitability and default on existing debt. Default notices hit the headlines causing further lending slowdown as lenders recognize they had been too generous and optimistic about future prospects. One domino after another begins to fall. The economy enters recession fairly quickly. The equity markets follow on the first series of default headlines. Recessions have a history of lasting ~18mos. Businesses downsize and make other adjustments. After a few months of bottoming, the cycle lifts off again.

Investors speculate during every cycle. They speculate in multiple ways with multiple themes in multiple business sectors. None of these has ever called an economic top even though several mini-crashes may have occurred. Investor speculation in markets does not result in economic speculation. Markets have crashed many times during an economic cycle without impacting the cycle itself. It is when true economic speculation has occurred such that capital has been turned into business infrastructure in expectation of higher returns that recessions occur. T-Bill capital, meant for short-term business operations as a hedge for bouts of business weakness, becoming invested in illiquid business operations including plant equipment, real estate, inventories and etc is no longer fungible. If economic slowing occurs, the cash flows required to pay for these assets and the borrowings to fund them are no longer available. The business is forced to default because T-Bill capital has been committed elsewhere.

It is the rising of T-Bill rates to the level of the 10yr Treas rate which is the crucial detail. We have seen recently (2018-2019) the 10yr Treas Rate fall as capital flooded the US from foreign markets and cause yield curve inversion that did not reflect economic slowing by any other economic indicator. The T-Bill rate to the 10yr Treas rate is always accompanied by stalling Retail Sales, weakening Employment, falling Job Opening and Chemical Activity Barometer trends when business investment is speculative. Recessions follow! Markets top once the headlines reflect economics.

My best estimate is that the current cycle has 3yr-5yrs to go. The TB/TRS is still widening towards the 2% historical spread level(see charts). 2% spread appears to be the point at which the T-Bill rates then begin to rise as businesses get drawn in and become more speculative, eventually leading to yield curve inversion. It looks like we have some time yet to go before that occurs with ~7mil people still unemployed.