- The Earth is flat

- Cigarettes are healthy

- Leeches are the cure for everything

- The universe revolves around the Earth

- California is an island

- Red wine is healthy, unhealthy, healthy…

[timeless]

Facts are essential as they offer humans a sense of stability in a chaotic world. For instance, we find comfort in the “fact” that the life-sustaining sun will continue to shine for billions of years. If there were serious doubts about this fact, our lives would be very different today.

In this article, we debunk a “fact” that serves as the foundation for the pricing of all financial assets. It was not that long ago that people who thought the earth round were labeled delirious madmen. Today, questioning the “risk-free” status of U.S. Treasury securities (UST), as we do, will lead many financial professionals to decry our prudence as foolish irrationality. That said, we would rather assess the situation objectively than get caught “swimming naked when the tide goes out”.

Mesofacts

In a must-read article entitled, My Leitner-esque Moment, Kevin Muir of The Macro Tourist blog broaches the topic of sovereign debt risk and, in what must be a moment of temporary insanity, questions the so-called “risk-free” status of UST.

Sovereign debt risk exists and said bonds default from time to time. Despite history and facts, associating the word “risk” with UST is for some reason blasphemous amongst financial professionals. The yields of UST are treated by all investors, even those nay-sayers like Muir and ourselves, to be the risk-free rate. This argument does not refer to the risk of changing yields but more importantly to that of credit risk.

All financial and investment models and theories assume that UST have no credit risk which, by definition, implies zero chance of default. What in this world has no risk? If you can name something, congratulations, we cannot.

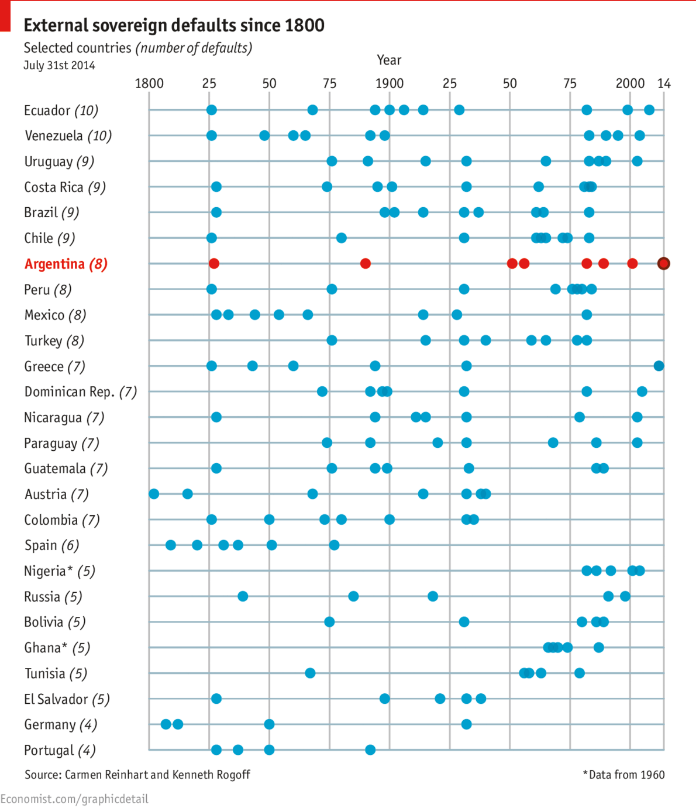

For background, consider that sovereign debt defaults have been commonplace among big and small countries. The graph below shows the frequency by country since 1800.

Graph Courtesy Carmen Reinhart and Kenneth Rogoff

Go back further in time, and almost all nations can be added to that list. The United States stands alone as an economic and military powerhouse that has never defaulted. (It is important to note that many people, ourselves included, believe the U.S. defaulted when it went off the gold standard.)

Despite America’s perfect credit record thus far, it would be false to assume that UST are “risk-free”. This type of fact, assumed by the masses, is what Samuel Arbesman, the author of The Half-Life of Facts, calls a mesofact. A mesofact, unlike the known effect of gravity, is not a fact of the natural order destined to last for eons. Nor will it have a very short existence, like the fact that the sun is currently shining on my garden. Essentially, a mesofact is one that has temporary permanence.

We refuse to debate whether UST are risk-free as we patently know that cannot be true. Instead, we consider the mindset of a bond trader and describe the ways we might measure U.S. credit risk.

The Mindset of a Bond Trader

“This next part of my post might be difficult to accept. Many will simply write off the theory as the ravings of a lunatic.”

Kevin Muir’s quote precedes a discussion about whether or not a U.S. corporate bond can trade at a yield below that of a similar maturity UST.

Can a corporate bond be even less risky than “risk-free”? The concept of “risk-free’ier” is mind-bending.

Fresh out of college, on day one on a trading desk, a bond market trainee is taught the practical (non-academic) concept of spreads. Unlike stocks, which trade at a dollar price and are not easily comparable to the price of other stocks or indices, all bonds trade at a yield spread to some benchmark, usually UST. Frequently, in fact, the dollar price of a bond is not even computed until after a trade is consummated.

To better describe this pricing methodology let’s relate it to the solar system. Bonds closest to the sun (UST) are the highest rated. As one travels away from our starting point, and the distance between planets and the sun increases, the perceived credit risk and therefore the yield spread over “risk free” Treasuries increases. In the fixed income universe, AAA-rated corporate and municipal bonds tend to trade with the tightest (or smallest) spread to comparable maturity UST as they have lowest default probability. Traveling further out the credit curve toward lower-rated bonds, the spread increases as default risk increases and the certainty of repayment decreases. The graph below shows the gyrations of various corporate bond indexes aggregated by credit ratings and their spread to UST over time.

Data Courtesy: St. Louis Federal Reserve (FRED)

In bond trader parlance, one would say the up and down movements of the lines above represent tightening (spread is declining) or widening (spread is increasing) relative to Treasuries. The graph below takes the orbit, or the percentage spread between BBB-rated corporate bonds and UST from 1997 to today, and plots it in a circular format to help further highlight this concept. (The orbit-like axis markers (0-8) are the percentage spread between BBB bonds and UST).

Data Courtesy: St. Louis Federal Reserve (FRED)

Back to the solar system. If we told you that, over the last few years, Mercury was tracking progressively closer to the sun, you would likely assume the orbit of Mercury is changing. Although inconceivable based on current scientific knowledge, what if it was determined that Mercury’s orbit was unchanged and the altered distance was due to the re-positioning of the sun? Similarly, what if the spreads of non-Treasury bonds were not 100% reflective of the factors that determine the yield for each security but also a change in the perceived risk in the benchmark itself?

Altered State

The U.S. Treasury Department is expected to issue over $1 trillion of debt in each of the next four years. This is additive to the $21 trillion debt load that is currently outstanding and must be refunded when bonds mature. Even more troubling, the growth rate of forecasted debt issuance is almost twice the size of the Congressional Budget Office’s (CBO) most optimistic economic growth forecast. As we have argued on many occasions, such a divergence between the debt burden and the means to service and payoff the debt cannot continue indefinitely. Deficits and debt do matter, and given this unsustainable situation, there is inherent credit risk in UST despite what finance professionals may tell you.

Ironically, there are currently two popular ways to measure the credit risk of the risk-free security, and neither of them currently reflect the absence of risk. The two commonly followed gauges are the credit ratings assigned to UST via the credit rating agencies and Credit Default Swaps (CDS) traded in public markets. Currently two of the three major credit rating agencies (Moody’s and Fitch) assign the highest credit rating of AAA to the debt of the United States. S&P rates them at a less than perfect AA+. Credit default swaps (CDS) are derivative contracts that enable an investor to buy insurance on the default risk of a debt issuer. If the issuer defaults, the insurance holder is made financially whole. The CDS of the United States currently trades at 27.5 basis points, which implies the odds of default are about 1.50-2.00%

A Third Way to Measure Default Risk

As Kevin Muir implies in his article, there is a third way to evaluate credit risk. Kevin wonders about the implications of a corporate bond trading at a lower yield than a U.S. Treasury of comparable maturity. We take that thought a step further. Could the spread between corporate bonds and UST, even though they are currently positive, be expressing heightened credit concerns for Treasury securities as opposed to less default risk for corporations?

What if the spread of AAA rated corporate bonds to UST were to tighten by ten basis points over the next month? Bond traders will robotically claim the spread tightening is a function of increased demand, reduced supply and/or a better economic outlook for the bond issuer. Given current circumstances, is it unreasonable to suggest that the yield on the corporate bond was unaffected and the yield on the U.S. Treasury increased due to credit concerns? Might it be possible the Sun has, against all conceivable logic, moved?

This concept is extremely hard to grasp, especially for those of us with decades of experience trading bonds. There are many instances in finance where a large majority of participants are gripped by muscle memory and habit. They are wed to the idea that the future credit history of the U.S. will be what it has been in the past. If we are to be successful investors over the long run, especially at crucial turning points, we must fight false assumptions, bad habits and challenge the durability of even the most basic “facts”.

Summary

Debunked facts are not only common but reflect a healthy progression of human knowledge. Such advancement, otherwise known as innovation and productivity, has led the human race to longer life spans, improved technologies, and greater economic well-being.

The fields of finance and economics, unlike most sciences, do not always seem to ascribe to the notion of incremental learning. Those in the financial community tend to repeat the same errors of the past. Just the past 100 years provides ample evidence of this through multiple boom-bust periods in which those Ph.D.’s from the best universities made the same critical mistakes. As such, the “growth” of logic and critical thinking in economics tends to be more cyclical than incremental. Mesofacts are presumed permanent, effectively stifling progress.

“I find it funny that the most vocal critics about the spiraling upward out-of-control government debt are often those investors’ most likely advocating positions in long-dated sovereign bonds as a place to hide. The surprise of this cycle will be that risk-free sovereign bonds provide no safety against the next crisis, but will instead themselves be the source of the instability. Think about hedging against the unthinkable happening.” – Kevin Muir

We concur with Kevin. No one has a crystal ball with the mystical ability to know when the imbalance of debt will overwhelm the nation’s ability to pay for it. We would argue that the United States is well beyond that point of no return and the missing piece of the puzzle is the point at which investors realize that fact. One glance at recent patterns of buyers of UST argues that some of our largest foreign sponsors may be asking these very same questions. That said, all investors should recognize that U.S. Treasury debt does indeed have credit risk and that risk is growing.

We intend to persuade you to think about things in ways that few do. In doing so, you will be able to rise above the large majority of investors that get caught in the sinkhole of cyclical thinking. Compounding your wealth depends on it.

Michael Lebowitz, CFA

Investment Analyst and Portfolio Manager for Clarity Financial, LLC. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Article by Real Investment Advice