An examination of the common belief that conflicts of interest contribute to the high cost of financial advice reveals most advisors invest personally just as they advise their clients, engaging in frequent trading, returns chasing, selecting expensive actively managed funds, and underdiversifying. Advisors’ net returns of −3% a year are similar to their clients’ net returns.

[timeless]

Q2 hedge fund letters, conference, scoops etc

On This Page

The Misguided Beliefs of Financial Advisors

Slides

Financial Advisors

- Households rely extensively on financial advisors to guide their investment decisions (ICI 2013, Canadian Securities Administrators 2012):

- 53% of households owning mutual funds in the U.S. held funds purchased through financial advisors

- Out of $876 billion of retail investment assets in Canada, 80% of assets managed by advisors

Cost and Quality of Advice

- Recent research raises concerns about the cost and quality of advice:

– Many investors paying 1.5% to 2.5% of assets per year for advice and management- Compounds to 15% to 25% reduction in retirement assets over 30-year horizon

- The Mullainathan, Nöth, and Schoar (2012) audit study:

“Advisers encourage chasing returns, push for actively managed funds, and even actively push them on auditors who begin with a well-diversified low fee portfolio.”

Impediments to Low-Cost Advice

- Focus has remained on conflicts of interest as explanation for high-cost and low-quality advice

- Retail financial advisors often compensated through commissions on the products they sell

- POLICY CHANGES: U.K.’s and Australia’s bans on commission-based compensation

- We investigate an alternative explanation with starkly different policy implications: misguided beliefs

- Advisors pursue active management and chase returns in high-cost funds because they sincerely believe those strategies improve returns

Our Paper

- Our Approach: Detailed data on advised accounts in Canada affords unique opportunity to compare advisors’ own trades to their clients’ trades

- Our Findings:

1. Clients and advisors both underdiversify, chase returns, and prefer higher-cost, actively managed funds; they earn similar net returns even after fees and rebates

2. An advisor’s own behavior is a strong predictor of his clients’ behavior

3. Advisors show similar trading patterns after they stop advising clients - Differences in advisors’ personal beliefs drive meaningful variation in client portfolio returns

Data

- Data from two (independent) Canadian mutual fund dealers

– More than 3,000 financial advisors and their half a million clients

– Total AUM = $18.9 billion–over 6% of the MFDA assets - All holdings, transactions, and fees from 1999 through 2013

- Demographic information for clients and advisors

– Know Your Client forms: age, risk tolerance, investment horizon, financial knowledge, wealth, income, occupation

Advisor Portfolios

- Three-quarters of the advisors in our sample are also “clients”

- Able to link advisor to personal portfolio if held at own firm

- Those who are not are typically younger advisors with few clients

- Clients would only see advisors’ portfolios if willingly disclosed

- Advisors pay the same mutual fund fees as clients, but do receive commissions for their own purchases and holdings

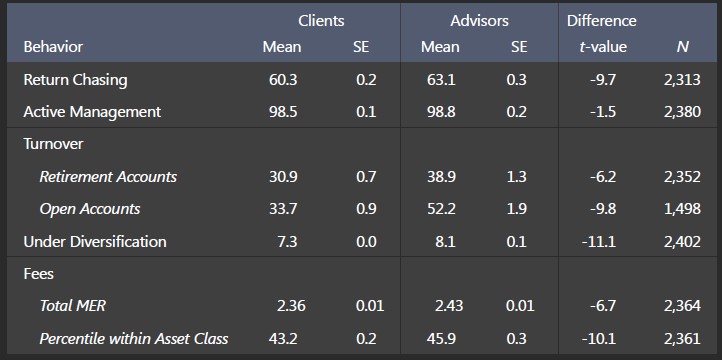

Measures of Behavior: Clients versus Advisors

See the full slides here by Research Affiliates