In Part III, we examined the role of economic paradigms in the equality/efficiency cycle. This week, we conclude this four-part series with a discussion on the flaws of Modern Monetary Theory (MMT) and market ramifications.

Q4 hedge fund letters, conference, scoops etc

The Flaws of MMT

All of the major economic paradigms previously discussed lead to eventual problems. Capital-friendly policies, such as Classical or supply-side theories, eventually lead to inequality. Policies less friendly to capital eventually become inflationary. MMT has a few flaws as well. Here are the ones we are most concerned about.

All investment is hard and public investment may be the hardest. There was a good reason why Keynes was so concerned about investment shifts. Investment is a bet on the future and no one can predict the future with certainty.

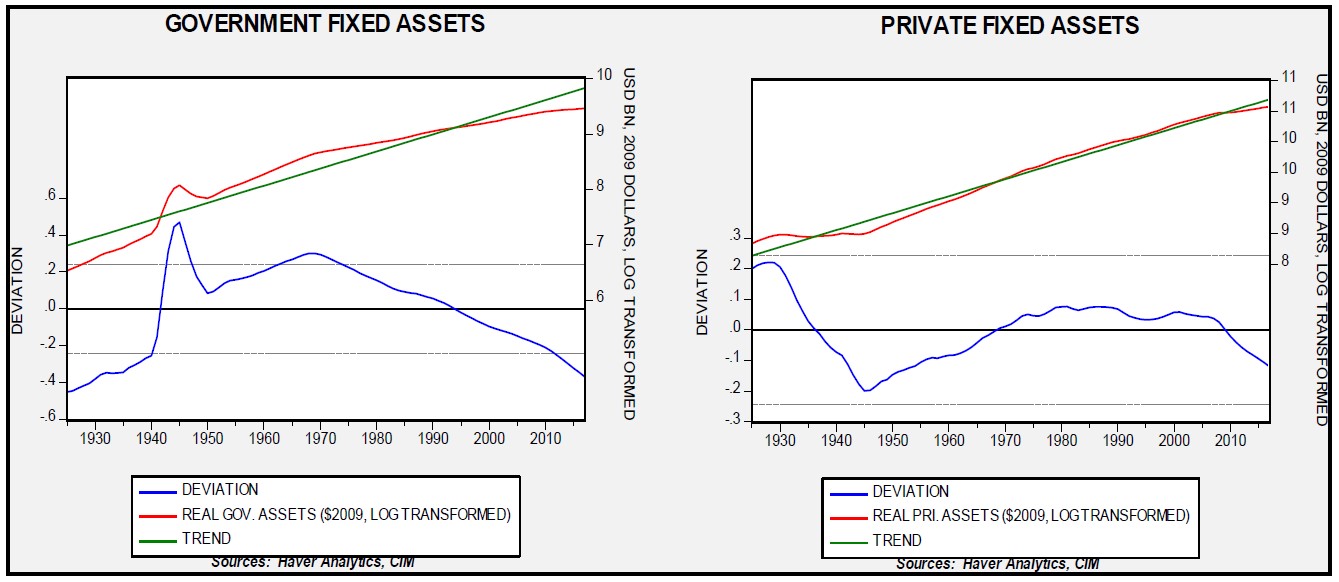

These charts show the level of inflation-adjusted fixed assets for government (left chart) and the private sector (right chart). Public fixed investment was increasing during the Great Depression, then soared during WWII and the early part of the Cold War. It made a secondary peak in 1970 and has been steadily declining since. Notably, private sector fixed investment also fell below trend after the Great Financial Crisis and remains weak.

These charts would suggest that public investment has been so “starved” that it should be feasible to find good projects to boost economic efficiency. However, public investment doesn’t have a profit test in the way private sector investment does. MMT could open the door to significant public investment and risk a problem like the “bridges to nowhere” program that Japan faced in the 1990s into the turn of the century. Public investment in an emerging economy can easily lift an economy because it starts from such a low base. Conversely, in a developed economy the challenge for making efficiency-boosting public investment is much more difficult. For example, adding additional lanes to major urban highways would be very costly but probably wouldn’t reduce bottlenecks, and there is the risk that high-speed passenger rail networks may lack riders. Getting investment right is really hard in the private sector, which has a profitability test. It’s even harder without such a test.

Taxpayers view taxes and government expenditures differently than MMT postulates. The U.S. has a voluntary selfreporting tax system that generally works well.1 The most likely reason, beyond the threat of incarceration, is that our taxes are thought to “pay” for something. Paul Samuelson worried that spending could spiral out of control and eventually lead to a serious inflation problem without the belief that fiscal budgets need to be balanced.2 If taxpayers begin to believe they are being taxed to prevent them from spending instead of paying for government services, the incentive to comply will end up relying solely on the fear of incarceration. In addition, state and local governments do face a real budget constraint; it is unclear if taxpayers will be able to distinguish the difference, or, if they do, they may ask why we have state and local spending at all? If taxes aren’t necessary for spending, then why not have the Federal government supply all services for “free”? Obviously, this argument against MMT is a bit of a “straw man,” in that MMT doesn’t say taxes are unnecessary; but, by saying they aren’t needed to pay for spending, there is the chance that a disconnect will develop for taxpayers and it may be hard to argue for taxing at all.

If taxing becomes functional for curtailing inflation, the shifts in policy may become impossible to implement. In other words, if taxing focuses solely on inflation control, then it will likely require a degree of flexibility that Congress probably can’t provide. It is possible that Congress could grant some of its spending and taxing powers to a technocratic body as it did to the Federal Reserve on monetary policy. However, pre-Volcker, there was great concern that the political will to allow the Federal Reserve to tighten monetary policy enough to bring down inflation was not possible.3 Although Volcker was able to implement monetary austerity, he did it through “sleight of hand” by focusing on the money supply and not the level of the fed funds target. It is quite possible that the Volcker era was an accident of history and will never be repeated again.

At the same time, the Fed has a very narrow set of tools; it can adjust some regulations and put up a rate target (and, as we saw over the past decade, it can buy up existing bonds). It would be unclear how much leeway Congress would give a fiscal body.

It isn’t hard to imagine a situation where inflation becomes a problem and the most effective way to bring it down would be to raise taxes on lower income households because they have a higher propensity to consume. That might be politically impossible. MMT looks attractive when inflation is low and growth is sluggish. As Keynesianism saw in the 1970s, no policy to bring down inflation is popular unless it is at extremes and MMT may be uniquely ill-equipped to respond.

There is an element of faith that underlies asset markets that MMT may underappreciate. Hyman Minsky suggested that a sovereign debtor may need to show that it is able to “achieve a cash flow net of operating costs that exceeds the commitments to pay on account of debt…” However, “has to be able” does not mean that it does.4 As MMT states, it is true that a government issuing debt in an unconvertible currency will not default on that debt. But, debt holders can panic and the most likely outcome would be a currency crisis. If a nation has a fixed exchange rate then the crisis can occur suddenly, as it did for many nations during the Asian Economic Crisis. Once investor sentiment is undermined, the decision to save may shift from financial to real assets. The history of hyperinflation makes it clear that faith in the currency can be undermined even if a government continues to pay out local currency on bonds and default is avoided.

The prescriptive bent of MMT proponents could undermine the descriptive theory. The arguments against MMT are difficult to make; assuming a government issues a non-convertible currency and issues debt in that currency, there is no good reason for a government to default on its debt. It has the avenue of effective default via inflation available to it so actually defaulting would be illogical. It is difficult to refute that logic. However, many of the supporters of MMT move well beyond that thesis, calling for all sorts of policies. For example, among leaders of the movement there is broad support for a government jobs guarantee (“government as employer of last resort”).5 The problem with being prescriptive instead of descriptive is that policies that simply fail because they are bad policies may be blamed on MMT and undermine the theory. Much of supply-side economics was very effective in lowering inflation; deregulation and globalization expanded supply and brought down prices. But, when the term is mentioned, most people probably believe that supply-side economic policy is only about tax cuts, or that Keynesianism was only about deficit spending. Neither one is a full description of the economic paradigm, but that is how the theory is “sold” to the public and policymakers.

MMT may only be effective for the developed world and especially for reserve currencies. Minsky’s concern about undermining faith in the currency by a reluctance to tax could lead to depreciation in a developed market currency, but it could also bring a crisis for emerging market financial systems. Although MMT’s insistence on borrowing in one’s own currency holds, there is a tendency among investors to have more faith in an emerging economy that borrows in a hard currency. It is obvious this faith is often misplaced, but that doesn’t stop investors from preferring hard currency bonds from emerging markets.

For developed economies, especially reserve currency nations, MMT could be very effective because alternative currencies are lacking. Although precious metals or cryptocurrencies offer some degree of store of value, neither option works especially well as a medium of exchange or as a unit of account (we don’t price cars in ounces of gold or units of crypto). Thus, a reserve currency nation may use MMT as a paradigm to boost economic growth and essentially force the adjustment on the rest of the world. To some extent, we saw this in practice after the fall of the Bretton Woods system. John Connolly, U.S. Treasury Secretary in 1971, remarked to European finance ministers that the dollar “is our currency but it’s your problem.”6

While it isn’t often characterized as such, MMT might actually be a tool of hegemony. If the U.S. wanted to reflate and weaken the dollar, it could use MMT as the underlying reason. Since much of the world relies on U.S. consumption for economic growth, a deliberate policy to depress the value of the dollar via reflation and fiscal deficits could force foreign nations to adjust in ways they would clearly prefer to avoid. Nixon’s decision to end the Bretton Woods system and gold convertibility was, in many respects, an exercise of raw power and Connelly’s observation captures that decision. Although many critics of MMT fear a dollar collapse, in reality, there isn’t a real alternative to the dollar for reserve purposes. If the U.S. decides it wants to reflate then the rest of the world will struggle to adjust.

Ramifications

The most obvious ramification of MMT is that it will justify reflation. Although this is a trend we have been expecting for some time as the U.S. tries to adjust its hegemonic role and address inequality, so far, there hasn’t been a new economic paradigm to support the transition.7 We suspect MMT will be that paradigm, which is why we published this series. The lack of concern about deficits from both parties could be a sign that, for all practical purposes, MMT has become the working theory of economics even without an overt acceptance of the theory.

At some point, we will see inflation return, but the timing is difficult to determine. The above chart showing the deviation from GDP trend growth could indicate that there is significant slack in the economy and therefore a binge of fiscal spending and public investment may not initially absorb productive capacity. Thus, it could take a while before inflation returns.

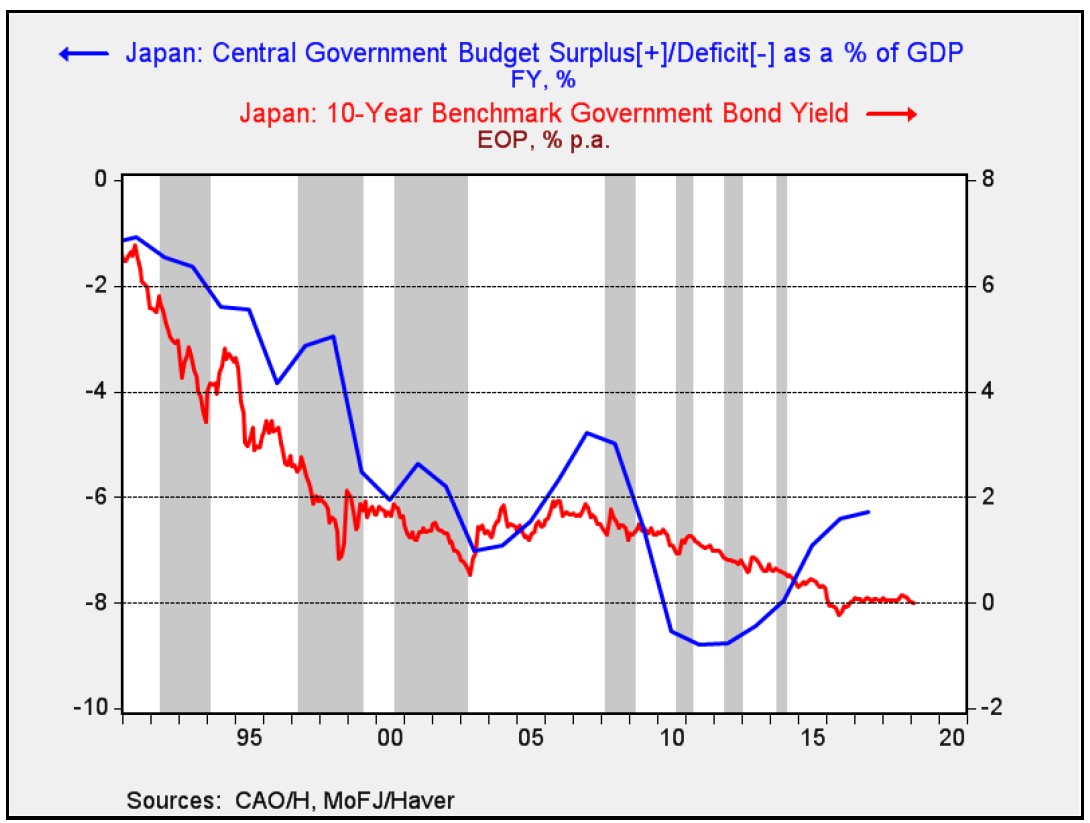

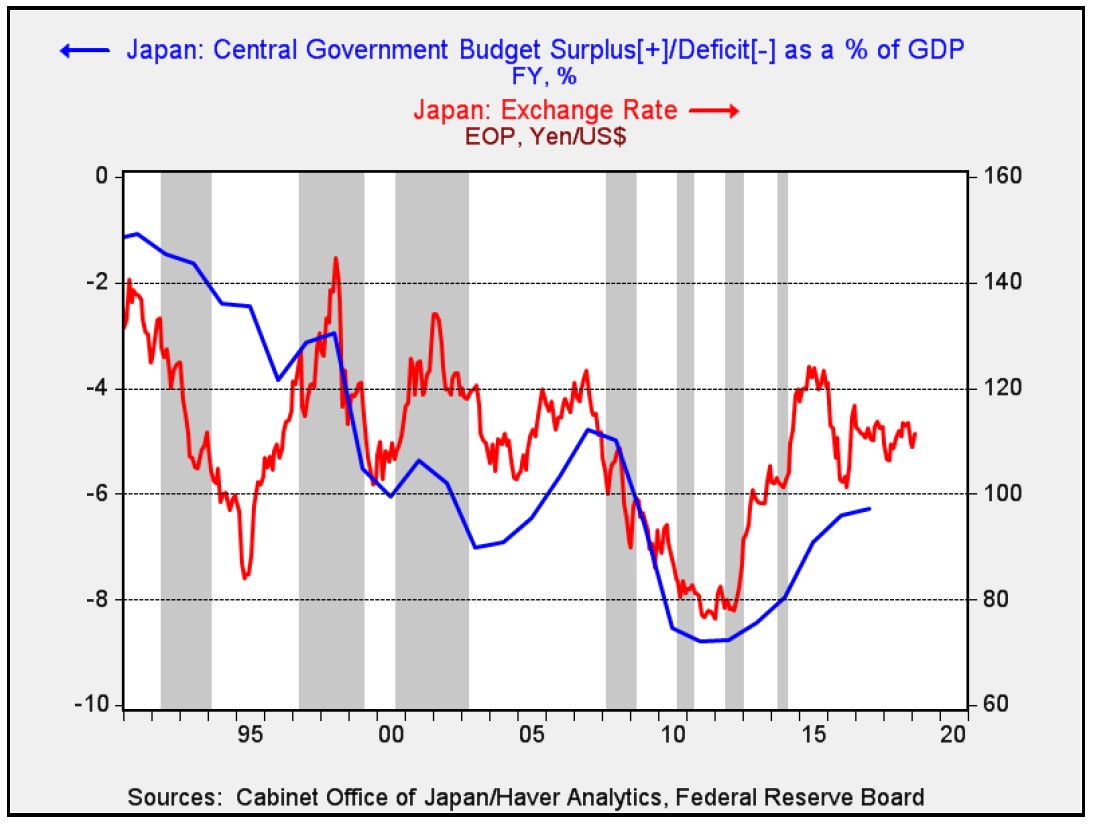

From a market perspective, it seems obvious that MMT would be bearish for the dollar and bonds. However, we would be cautious on this proposition. Exchange rates are not unilaterally decided; if the U.S. adopts MMT to expand fiscally, other nations may simply follow suit and create a “race to the bottom.” In that situation, gold and other precious metals should perform well. Some small nation currencies, such as the Swiss franc, could also benefit. Regarding bonds, Japan offers a cautionary tale. Despite massive fiscal deficits, 10-year yields remain near zero.

The chart above shows Japan’s government deficit with the 10-year soveriegn yield. As MMT would postulate, the rising deficit has expanded bank reserves and led to lower yields. To some extent, demographics likely play a role in this trend. But, this chart shows that rising fiscal deficits don’t mean that higher interest rates are inevitable. And, interestingly enough, fiscal deficits didn’t lead to a weaker yen either.

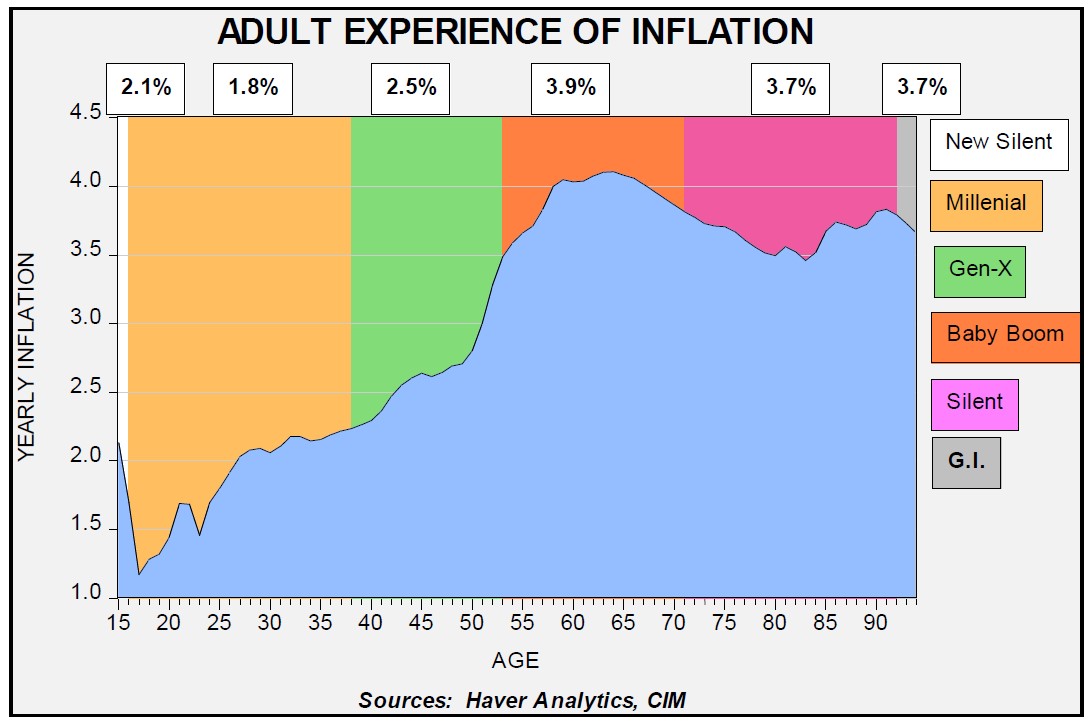

The key element for the financial markets is the role of expectations. The lesson from the 1970s was that if households and firms conclude that prices will be signficantly higher in the future then they will move saving into real goods as opposed to financial ones. Milton Friedman argued that inflation expectations are formed over a lifetime and it simply may take a while for them to change.

This chart shows the experience of inflation by generation from ages 16 through adulthood. The baby boom experienced the highest inflation of any age cohort; notice how rapidly inflation fell for subsequent generations. The lack of concern about inflation and the flirtation with socialism8 is partly due to the fact that those under 50 simply haven’t experienced the distortions that come from higher inflation.

Our position is that there are still enough baby boomers around to trigger inflation worries. Therefore, assuming reflationary policies are steadily adopted, bond yields will rise, the dollar will weaken and precious metals will benefit. But, these outcomes may take longer to occur than many expect. In the meantime, fiscal expansion will boost growth and, paradoxically, may actually lift the dollar in the short run if global economic growth remains sluggish. In the long run, MMT will likely foster reflation, a steeper aggregate supply curve, higher interest rates, dollar weakness, etc. Nevertheless, there isn’t much reward in being too early. Thus, we would stay tuned.

Article by Bill O’Grady of Confluence Investment Management