“More money than fools or more fools than money. When there is more money than fools asset prices go up. When there are more fools than money, asset prices go down.” – Louis-Vincent Gave, Founding Partner & CEO, Gavekal Research

Q4 hedge fund letters, conference, scoops etc

At last March’s Mauldin Strategic Investment Conference, Louis-Vincent Gave said, “The deflationary period we’ve been in has come to an end.” I began my April 6, 2018, On My Radar letter entitled China’s Game-Changing Policy as follows:

China and Trump escalated the Trade War fist fight this week and the markets are having trouble digesting the dire news. Is Trump picking a fight with the wrong guy at the wrong time? I’m all for a better deal but there is great risk in creating extreme to advance your negotiating position. And China has big plans. What you’ll find in today’s On My Radar is that what is happening in China has global implications. With or without a fist fight.

When Louis-Vincent Gave stepped on stage at the Mauldin 2018 SIC conference, I thought to myself, he’s sharp and smart, but here comes his annual “all things are bullish” China presentation. But he surprised me with his shift in view. I found his presentation to be outstanding. “The deflationary period we’ve been in has come to an end.” If he’s right, it has important implications for your portfolio and mine.”

I loved how my father used to teach me. He was a CPA and I’d come to him for help with my accounting studies. He would always take me first to the big picture conclusion. Let’s figure out what-and-why and then work our way to that conclusion, he’d say. I found that if I knew the end conclusion, I could better connect the dots on the way. At least, that seemed then and now to work for me.

“More money than fools or more fools than money.” Louis said his first client gave him that piece of advice. Great advice! There appears to be a low probability for resolution of the China trade war issues. The 90-day grace period ends at the end of February. The “fist fight” I wrote about last April battles on. The implications are global. Italy is in recession, France is near and Germany is a half-step behind both. On my economic dashboard sits a number of charts (see Trade Signals below). My favorite “Global Recession” watch chart says we are likely in a global recession. Trade wars and 25% tariffs are like throwing a monkey wrench into the wheels of the global supply chain. Evidence of which is surfacing. My U.S. recession dashboard remains favorable with no sign of imminent recession. We use monthly data so we’ll see what the data is telling us at month-end. I expect some weakening.

In 1999, more fools were heavily allocated to tech stocks. Investors were “all in.” More fools than money. In 2006-07, the fools were able to get no-doc mortgages, which led to housing speculation gone wild. Until the liquidity dried up. Today, the fools, in my view, are all in on corporate bond debt and certain popular stocks, such as Facebook, Amazon, Apple, Netflix and Google (the so-called FAANG stocks). The question is liquidity drying up? Louis suggests it is and I agree.

The problem today is that it is very hard to know the end conclusion. We just don’t yet know what central bankers will do and how elected officials will respond. Or even which elected officials and central bankers will be in place. Populism is a growing concern. So we watch price action, stay risk focused and stand ready to adapt. There are a range of possible outcomes.

Dad would take me first to the big picture conclusion. Today, I think the big picture is the challenges that present at the end of long-term debt cycles. What does well… what does not do well. Profiting is simply being on the right side of the trend or avoiding getting run over. I believe we’ve got a pretty good feel for what the moves may be… which levers might be pulled. We don’t know when or which will be implemented. So we step forward, stay risk minded and ready to adapt.

Below you’ll find my summary notes from the excellent Financial Sense podcast with Louis-Vincent Gave from Gavekal Research. Gavekal Research is one of the world’s leading independent providers of global investment research. I’ve met Louis a number of times over the years at John Mauldin’s annual Strategic Investment Conference. He’s humble and smart, and I recommend you keep him on your radar screen.

Grab that coffee and find your favorite chair. Louis-Vincent does an excellent job painting the picture for the period ahead. I also take a quick look at the latest unemployment level and discuss what that means in terms of potential stock market performance. Lastly, you’ll find the link to the latest Trade Signals post… no significant changes.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- Low Liquidity – Louis-Vincent Gave

- Unemployment and the Stock Market

- Trade Signals – Testing Overhead Resistance (Red Zone)

- Personal Note – Going Skiing

Low Liquidity – Louis-Vincent Gave

Following are my summary notes from the recent Financial Sense podcast featuring Louis-Vincent Gave:

We’ve had back-to-back years of increasing budget deficits in spite of good economic growth. Why is this happening? The U.S. is aging, which means entitlement spending increases. Medicaid, Medicare and Social Security expenses are going up. That has to be funded.

The U.S. government is running a $1 trillion deficit. That is, the federal government is spending $1 trillion more than it receives from tax revenue (and fees). The government is funding operations and expenses by issuing new debt.

Given that the Fed is no longer printing money and no longer going to fund the increasing U.S. budget deficits, it means that the private sector has to fund it.

The U.S. government will always get funded. They are like the 350-pound linebacker at the front of the buffet line who cleans up all the food and the rest of us are left to grab the scraps. And the reality is that the scraps last year weren’t big enough to push up asset prices. (In English, what Louis-Vincent is saying is the Fed is no longer printing money and there is far less liquidity in the system to drive asset prices higher.)

Gavekal’s “Track Macro System” is their attempt to produce a dashboard. It’s a way to look at the markets country by country. The outlook can be positive or negative. Today, most of the markets are flashing negative. The reason most of them are negative is that the liquidity situation most everywhere is negative.

It is not only in the U.S. that budget deficits are growing; it is almost everywhere and the major central banks are saying, “I’m not going to feed the beast anymore.” The Federal Reserve started expressing this a year ago. The ECB is now saying the same thing.

This is problematic now because you have recession in Italy and you very likely soon will have recession in France and Germany. And each time you have recession, budget deficits go through the roof so there will be further need to fund (borrow) and pay for the budget shortfalls.

The big challenge the world is confronting is how do we pay for this growing increase in government spending when the central banks don’t want to do it?

The private sector will have to and that’s a real challenge for asset prices. This means there is a crowding out effect going on where the marginal dollar isn’t going into investment assets, they are going into government coffers. And we are seeing that in country after country after country.

Now, it doesn’t mean the end of the world. It doesn’t mean we are going to have a major financial crisis; it doesn’t mean that growth is going to crash. What it does mean is that this presents are real hurdle to higher asset prices to go up in that environment.

Dynamite Fishing

Louis-Vincent was asked who the big fish (i.e., the victim) might be in the next crisis. Using an analogy that when you throw dynamite in the water, the idea is that when liquidity squeezes present, you first see the impact on the little guys. In this cycle, the little guys are people in the crypto space, countries like Argentina and Turkey. All of whom hit the wall last year. Usually a liquidity squeeze doesn’t end until you see a change in policy by central banks and/or policy makers.

In 2008, the real whale was AIG. When AIG appeared, the U.S. government said forget mark to market. In 2013, the whale was Italy, Spain… when these guys hit the wall, the ECB said, “You know what, I used to have a rule book but it won’t work so let’s tear it apart. I’m going to have a new rule book and the new rule book says I have no rules.” (Draghi’s “Whatever it takes.”)

When the big fish appears, policy basically changes the rules and you move on. [SB here: note that it usually takes crisis to change the rule book and that is what likely happens the next time as well.]

In the current cycle, we’ve had a little show up at the surface but we haven’t yet had the whale that will cause a change in policy (from the Fed, the ECB or anyone else).

There are a lot of potential whales out there. If you ask a French client, they point their finger at Italy. If you ask an Italian client, they point their finger at Deutsche Bank. If you ask a German client, they point their finger at France. When I talk to U.S. clients, most of them point their finger at China. They see China as having unsustainable levels of high debt and as being an accident waiting to happen.

My biggest concern today is the U.S. corporate bond market. I’m concerned for several reasons:

- We’ve had a growth in the U.S. bond market that has far outstripped the growth in U.S. GDP over the past 10 years.

- When you talk about the corporate bond market, there are really two markets. One is investment grade (high quality) and the other is non-investment grade and both have different investors, different behaviors and different characteristics. The challenge today is that part of the massive growth has taken place in the triple-B (investment grade) space. If you start seeing a turn down in the economy and the usual types of rating downgrades that occur in an economic downturn, then all of a sudden you have that lowest level of investment grade become non-investment grade at a time where there will be no demand for non-investment grade bonds. General Electric (GE) is a perfect example. They have $115 billion in outstanding debt. GE bonds were A rated but are now rated just one notch above the junk bond (non-investment grade) category. If they get downgraded overnight, you have more than a 10% increase in the size of the non-investment grade debt market. For this very reason, I don’t think GE will get downgraded, even if it means wiping out equity shareholders. I don’t think GE will be the big whale but behind GE, you have many other companies. Energy debt issued by a lot of negative cash flow companies in the energy space, industrial sector debt and the real estate debt. Now we know the auto sector is rolling over, the housing sector is rolling over, the energy sector is rolling over…

- The third reason is that a lot of the debt we’ve seen issued is used for the massive rise we’ve seen in share buybacks and financial engineering. We have balance sheets that are way more stretched than they’ve been in prior cycles.

Asked a question on bond market liquidity, given a downturn or a financial disruption, what happens to individual investors when they find out their leveraged loan or high yield bond funds or ETFs are not as liquid as they think? Where does the liquidity come from? Louis-Vincent said the answer is, “I don’t know.” We are in uncharted territory here. The reality is we have a bond market that is three times larger than it was 10 years ago with inventory that is not even a quarter of what it was 10 years ago. Ten years ago you could call your broker (Goldman Sachs, JPM, Merrill Lynch, Morgan Stanley) and get a price on your bond. You may not like the price, but there was always somebody there to make a market. The point is there was always liquidity. Today there isn’t even a market. Post-2008, investment banks can’t warehouse risk anymore. They can’t take onto their balance sheet the other side of your trade. They can’t buy things you want to sell that you no longer want. So that creates uncertainty. You have a whole new set of market participants who have reached out for yield into riskier and riskier things than they ever have before.

Much of the bond market is no longer just high net worth investors, insurance companies and pension companies. It is mom and pop. This all increases the level of uncertainty in the market. And to me the bonds are not really priced for the level of uncertainty that comes with them.

Asked: The Fed is shrinking the balance sheet by $50 billion per month and the ECB is backing away. How do we get liquidity back into the system? Louis-Vincent said, “First it depends on who the whale is. If it is Deutsche Bank, for example, the Fed could say, ‘It’s not my problem, it is Germany’s problem.’ So if DB is the whale, the German government will likely nationalize the bank and the change in policy will be the German government allows itself to run much bigger budget deficits than it has allowed up to now and that could be relatively bullish for Europe (though not for the DB shareholders). That is one scenario.”

Another and more likely scenario. In May, we have European elections that bring in highly skeptical European Union parties in the leadership. This makes the turnover in the European Commission very challenging. And with that, basically Europe gives up on its 3% budget deficit rules and all the countries, whether it is Italy, Spain, Portugal, France, and Germany, start running even bigger deficits. At this point, the ECB has a choice to monetize the deficits (print and provide the liquidity). If they decide not to monetize and stick to a strict monetary policy, you could have an even bigger liquidity squeeze that could kill off the whale of the European markets. More likely the ECB will choose to go along and print a lot of money and you would have a big outperformance of Europe.

If the problem is in the U.S. corporate bond market, does the Fed do what the ECB did and start buying up all of the troubled U.S. corporate bonds directly? Maybe, after all the Fed is now supposed to be the new regulator. And if the U.S. corporate bond market dislocates, it could be viewed as the Fed’s fault based on their plans that were implemented that took away the liquidity from the banks. If the banks can’t do it, then maybe the Fed has to step in. [SB here: That seems most likely to me…]

So you can go into any kind of scenario with any kind of probable outcome; we just don’t yet know what is going to play out. [Which leads us to Louis-Vincent’s main point.] Investing is about adapting. You look at the situation and you adapt.

Today, we are in a liquidity squeeze. I don’t know who the victim will be. I have some ideas… there are a few places I can look at but I really don’t yet know. I’m not going to forecast who the victim is. Once we know the victim and the policy response, then we can adapt to that.

It seems likely to me and I tend to believe that with the next wave of central bank easing, and that may not be that far away, gold ends up doing pretty well (though I’m not a gold bug). I also tend to believe that with the next wave of central bank easing, the markets will start to worry about the sustainability of ultra-loose fiscal policies (governments spending out of control – high budget deficits pretty much everywhere) combined with worry about ultra-loose monetary policy. Usually if you think there is a crisis coming, one of the best things you can do is be short financials because they are highly levered and somehow historically they tend to be in all the wrong places. Today I’m not so sure because if the markets start to worry about the sustainability of ultra-loose policies, we see long-term rates go up (that tends to benefit the banks).

One of the simpler rules, as you go into an environment where there is not enough money around (a liquidity crisis), you want to avoid the crowded trades. This is the story of the last few months with the Apples and Netflixs of this world fall back significantly. Well, you could say they’ve bounced back aggressively in January but to me that is an opportunity to let go of them, if you didn’t let go of them before because in a tough liquidity environment, you don’t want to be in the overpriced, over-owned assets. Those are the guys where there is the most risk. Bottom line: you want to be defensive right now. But defensive may mean you want to own some Emerging Markets exposures at 9 P/Es or Latin America or value stocks (similar to 1999).

“More money than fools or more fools than money.”

“A significant drop in the weekly U.S. jobless claims on Thursday likely signals another blowout month for job creation, despite the prolonged government shutdown… “It suggests very strongly that the jobs report for January will be up.” – Larry Kudlow, Director of the National Economic Council. Source: Fox News Interview

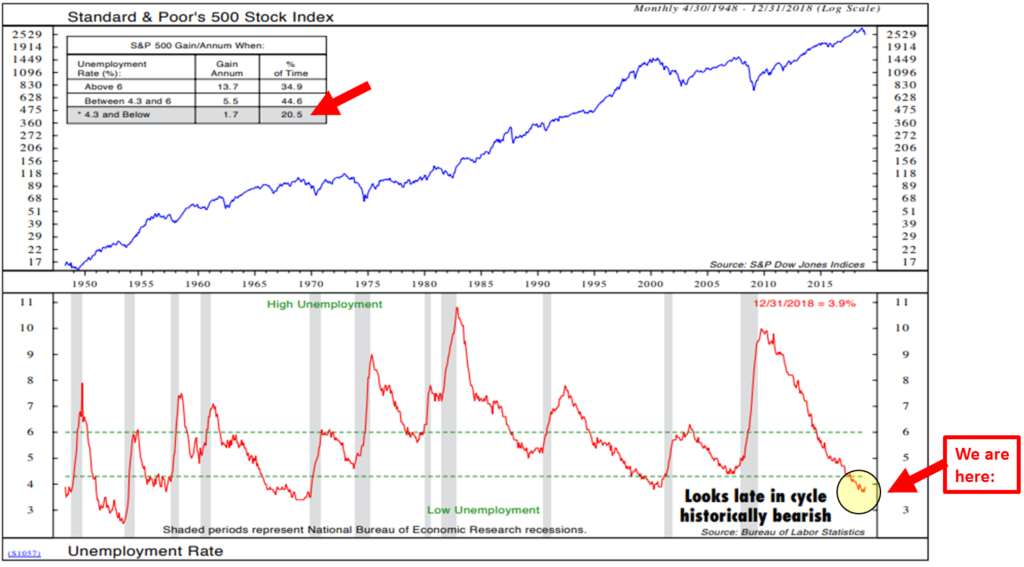

There are a number of data points we can look at to see where we are in the economic cycle. One is the level of unemployment. We often hear people pointing to the fact that the economy is strong so stocks will do well. Listen for that argument from politicians and other talking heads when you are watching CNBC, Fox News or CNN. Larry Kudlow was on Fox Business News last night talking about low unemployment and that wages are going up for the middle class. Unemployment is low… good for stocks? The data tells us otherwise.

Yet Another Sign We Sit Late Cycle

Take a look at the following chart. It plots the level of “Unemployment.” Yes, unemployment is very low (see the “We are here” annotation). The gray bars mark periods of recession. Those periods are bad for stock investors as the biggest losses come when the economy is in recession. High unemployment presents after recession because businesses lay off workers. Many businesses fail. Defaults rise. Earnings decline and stocks drop in price. The red line tracks unemployment.

Now focus in on the data box in the upper left (red arrow). It points to the “gain per annum” of the S&P 500 Index when unemployment is low… a 1.7% annualized return if the unemployment rate is 4.3% and below. The 20.5% number tells us that unemployment has been in the low zone (below the green dotted line) 20.5% of the time for the period 1948 to present.

Bottom line: we are late cycle and the best opportunity for stock gains will present after recession when unemployment is high. A game of opposites. Don’t bite on the Kudlow head fake.

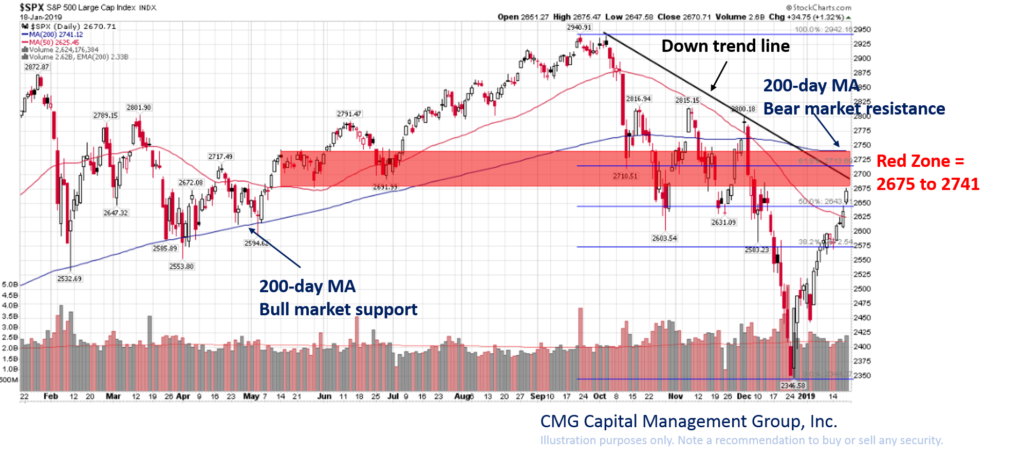

Trade Signals – Testing Overhead Resistance (Red Zone)

January 23, 2019

S&P 500 Index — 2,643

Notable this week:

The equity markets have rallied back and are testing their 200-day moving average lines. I tweeted the following chart out over the weekend. It shows the overhead resistance (or red zone) the market must get above to establish a new bullish trend. Note the “Down trend line” annotation and the arrow pointing to the 200-day MA line.

aaa

Investor sentiment is improving off of “extreme” bearish sentiment. Extreme pessimism is short-term bullish for stocks. Pessimism reached near record levels in late December. I noted it then and suggested we should see a short-term rally that would rally us back to the broken prior level of support (marked in red above). We are now testing that level.

There are no changes in the equity market signals since last week: the Ned Davis Research (NDR) CMG Large Cap Momentum Index is signaling equity exposure of 40% and the balance of the equity market signals remain in sell signals.

The CMG Managed High Yield Bond Program moved to a buy signal last week. The Zweig Bond Model remains in a sell signal (suggesting short-duration high quality bond market exposure over high quality long-duration ETFs and mutual funds). Gold remains in a buy signal.

We remain on global and US recession watch. Risk of global recession is high, while there’s low current risk of recession in the US we believe risk is rising. We’ll continue to remain data dependent.

Click here for this week’s Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note – Going Skiing

“Anything worthwhile takes time to build. We all want success now, but that’s not how success works. After all, if we had immediate success, we wouldn’t build the character we need to sustain true success. The struggle, adversity, triumphs, and victories are all part of the building process and we must embrace all of it.” – The Carpenter, by Jon Gordon

We’ll be on the road early tomorrow morning. It is about two-and-a-half hours from Philadelphia to Elk Mountain. It’s probably the best ski resort in Pennsylvania. Susan, Kieran and I are heading up to watch Matthew’s ski competition. It’s a two-day event and the first heat starts Saturday at 9 am. I remember when cousin Tommy sent me a video of Matt landing his first back flip. You can imagine if you come off short, your ski tips hit causing you to face plant into the snow. Not optimal. In the video, Tommy cheered so loud it gave me chills watching. What he later learned was that the first four attempts were failures and he landed the fifth. Ugh.

But anything worthwhile takes time to build and it’s more about the journey, living fully and attempting to create for ourselves that makes life so rich to live. Struggle, adversity, triumphs… losses, victories… Life! We are really looking forward to the fun ahead this weekend.

NYC follows early next week. A few exciting meetings on Monday with the team at Syntax. Talk about building something worthwhile.

Also, put the Mauldin Strategic Investment Conference on May 13-16 in Dallas on your calendar. I’m admittedly biased, but I can honestly say it is the single best investment conference I attend each year. This year, CMG will be hosting a breakfast where we’ll share some of the investment opportunities we are seeing.

To give you an idea of what I mean, here are a few of the confirmed speakers and experts:

- President George W. Bush

- Howard Marks, CFA and co-chairman at Oaktree Capital

- Carmen Reinhart, world-renowned economist and best-selling author

- Felix Zulauf, hedge fund manager and 30+ year Barron’s Roundtable member

- Jim Mellon, hedge fund manager and billionaire investor

- Plus, long-time SIC favorites David Rosenberg, Grant Williams, Mark Yusko and more.

Thank you for reading On My Radar. Please know how much I appreciate you and the time you spend with me each week.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Best regards,

Stephen B. Blumenthal

Executive Chairman & CIO