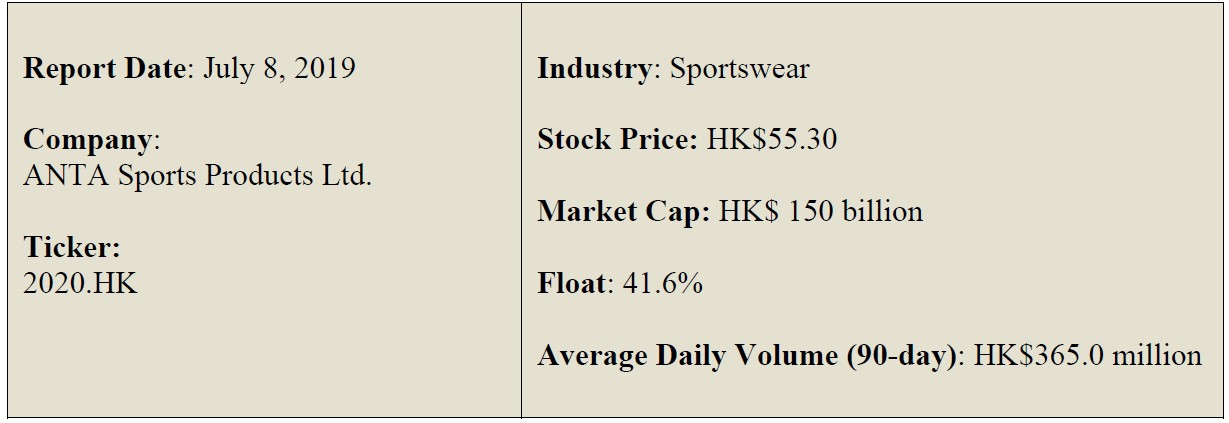

Muddy Waters Research’s short report on ANTA.

Q2 hedge fund letters, conference, scoops etc

We thought long and hard about the title of this report, which is the first in a series evidencing endemic fraud at ANTA. We kept coming back to “Turds in the Punchbowl.” ANTA is a real business, and in terms of operations and marketing, there’s much to be admired. Presumably, this is why accomplished sportswear entrepreneur Chip Wilson recently agreed to invest in it.1 But within all this goodness, there’s a distinctly awful truth. Investors cannot rely upon ANTA’s financials. We believe that ANTA posts industry-leading operating margins not because it’s so well operated; but, rather because ANTA uses numerous secretly controlled Tier 1 distributors to fraudulently boost its margins.

We have “Smoking Gun” evidence that ANTA secretly controls a material number of its distributors. In this report, we present documentary evidence that ANTA secretly controls 27 distributors. At least 25 of these of these appear to be Tier 1 distributors. The total number of Tier 1 distributors ANTA controls could be over 40 of the approximately 46 the company has.2 The secretly controlled distributors collectively appear to account for approximately 70% of ANTA brand sales.

ANTA resolutely claims that its Tier 1 distributors are independent third parties. This is a lie. The fact that ANTA controls its Tier 1 distributors is well-known among senior ANTA executives. ANTA’s senior executives know that ANTA conceals its control of the distributors by using proxy owners. However, this notion of independent distributors is such a charade that ANTA’s senior executives frequently refer to the distributors as “subsidiaries”.3 We believe ANTA controls these subsidiaries in order to manipulate its reported financials.

During our research process, we first followed paper trails, such as SAIC files, credit reports, and online articles. This research evidenced control of numerous Tier 1 distributors. One of many examples is that for a number of years, the Supervisor of one of the largest distributors was ANTA’s Executive Director with responsibility for sales, Wu Yonghua. Four former senior managers of ANTA and one former manager of a major distributor then expressly stated in interviews that ANTA controls the distributors.

We organized this report in three sections. In A, we explain how the fraud works. We include brief excerpts of our interviews with sources to corroborate the high-level points. In B, we show the extensive paper trail that demonstrates Anta’s control of 25 Tier 1 distributors and two smaller distributors. C is the Appendix, which contains more evidence and larger excerpts of source interview transcripts.

A: How the Fraud Works

ANTA began as a manufacturer of sneakers for other brands. When it wanted to become a domestic brand of its own, large distributors would not work with it. ANTA had to create its own network of distributors and retailers. ANTA’s controlling shareholder used his capital to invest in a network of distributors to give the brand traction. The strategy worked, and ANTA grew.

As ANTA planned for a 2007 IPO, a more nefarious strategy took hold. ANTA insiders realized that they could create the illusion of independent distributors. ANTA made a big show of reorganizing its distributors into purportedly independent, arms-length parties. Rather than merely re-naming their companies, distributors that had used ANTA in their names actually deregistered their entities.4 Individuals then formed new entities that did not use the ANTA name.

ANTA claims that its ANTA brand distributors are arms-length parties. The company accordingly insists that it has only limited visibility into its distributors’ financials because it does not own them.5 ANTA also recognizes revenue at the point of sale to distributors.6

However, this is a charade. In the substantial majority of cases, the owners of these distributors are merely proxies for ANTA Chairman Ding Shizhong. In March 2008, a company called Jinjiang Yundong Business Consulting Co. Ltd. (![]() , “Yundong”) was formed. Yundong is nominally owned by Peng Qingyun, but he is a proxy for Chairman Ding. Chairman Ding controls Yundong, while senior ANTA executive Wang Huayou is its General Manager.7 Yundong, in turn, controls many of ANTA’s Tier 1 distributors. ANTA executives frequently refer to this arrangement as a “left hand-right hand relationship” (“

, “Yundong”) was formed. Yundong is nominally owned by Peng Qingyun, but he is a proxy for Chairman Ding. Chairman Ding controls Yundong, while senior ANTA executive Wang Huayou is its General Manager.7 Yundong, in turn, controls many of ANTA’s Tier 1 distributors. ANTA executives frequently refer to this arrangement as a “left hand-right hand relationship” (“![]()

![]() ”), with ANTA the ListCo being the “right hand”, and the distributors being the “left hand” (via Yundong). Throughout the web connecting these “hands” are multiple people with the surnames Lin, Ding, Wu, and Peng, many of whom appear to be related.

”), with ANTA the ListCo being the “right hand”, and the distributors being the “left hand” (via Yundong). Throughout the web connecting these “hands” are multiple people with the surnames Lin, Ding, Wu, and Peng, many of whom appear to be related.

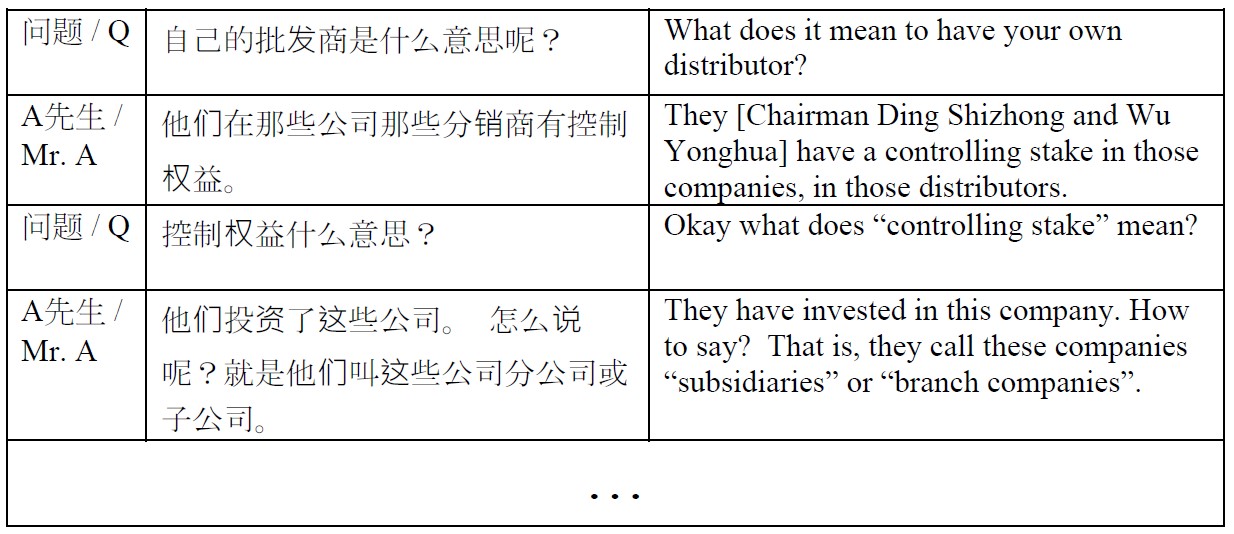

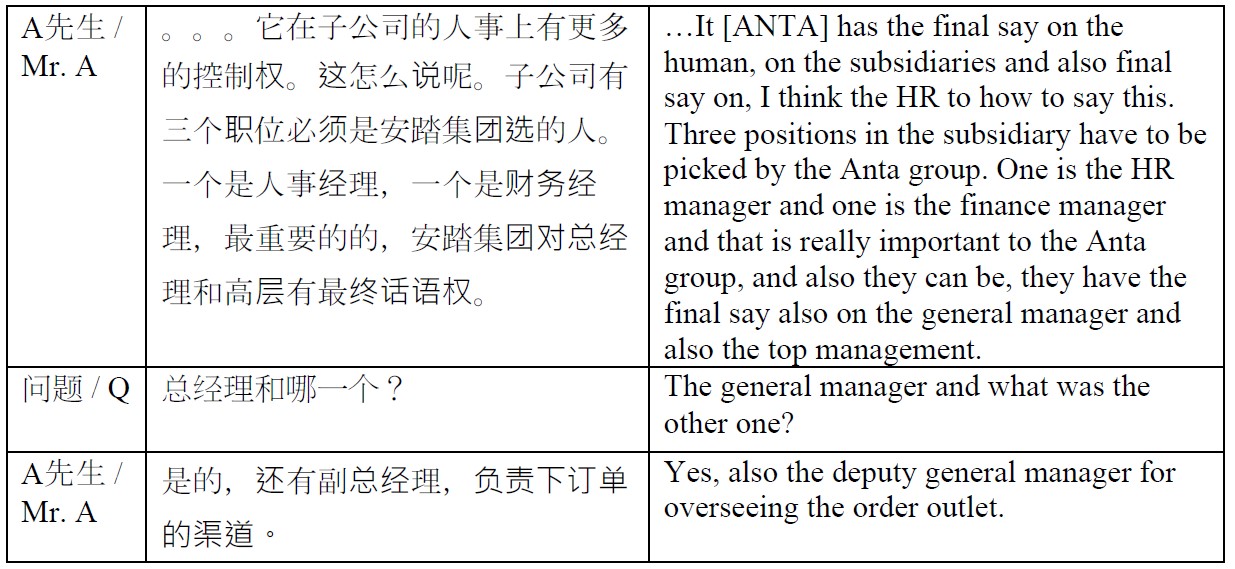

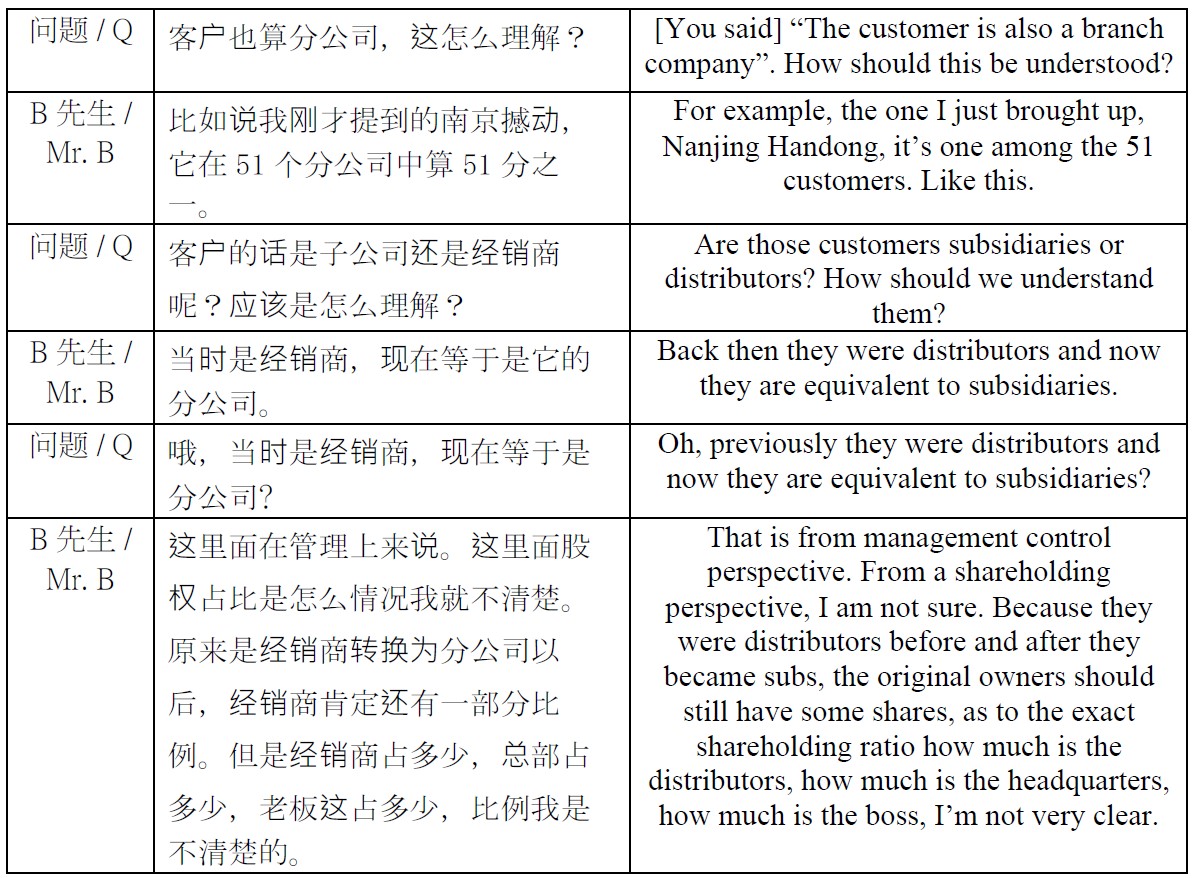

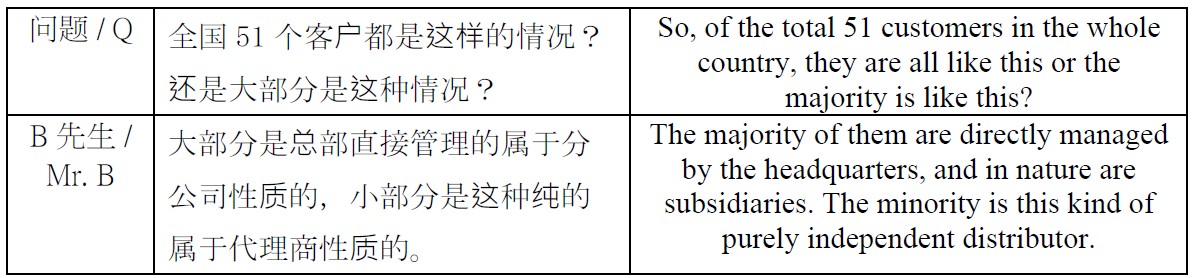

ANTA’s control over the distributors is an open secret among senior ANTA executives on the distribution side of the business. Senior ANTA managers commonly refer to the purportedly independent distributors as “subsidiaries” (![]() ). The subsidiary distributors, we understand, account for at least 70% – and possibly as much as 80% – of ANTA brand sales.

). The subsidiary distributors, we understand, account for at least 70% – and possibly as much as 80% – of ANTA brand sales.

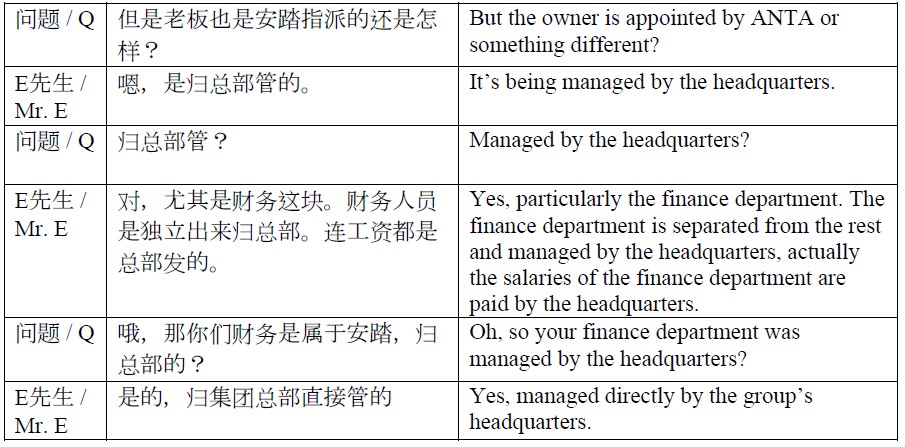

The manner in which Yundong exerts control over the distributors is through their human resource and finance departments. Yundong hires the HR and finance personnel. We understand from one source that ANTA – either through Yundong or directly – pays the distributors’ finance department personnel. By controlling human resources, according to a former ANTA executive, ANTA can control the hiring of staff.8 By controlling the distributors’ finance departments, ANTA can fraudulently manipulate the financial statements of the ListCo.

The purpose of controlling the distributors, we believe, is to fraudulently inflate ANTA’s reported revenues and/or decrease its reported expenses. ANTA’s operating margins have long outperformed those of its Chinese comps.9 We firmly believe that this apparent margin superiority is due to fraudulent manipulation of ANTA’s financials through the relationships with the distributors. In other words, ANTA’s margin outperformance is not real in our view.

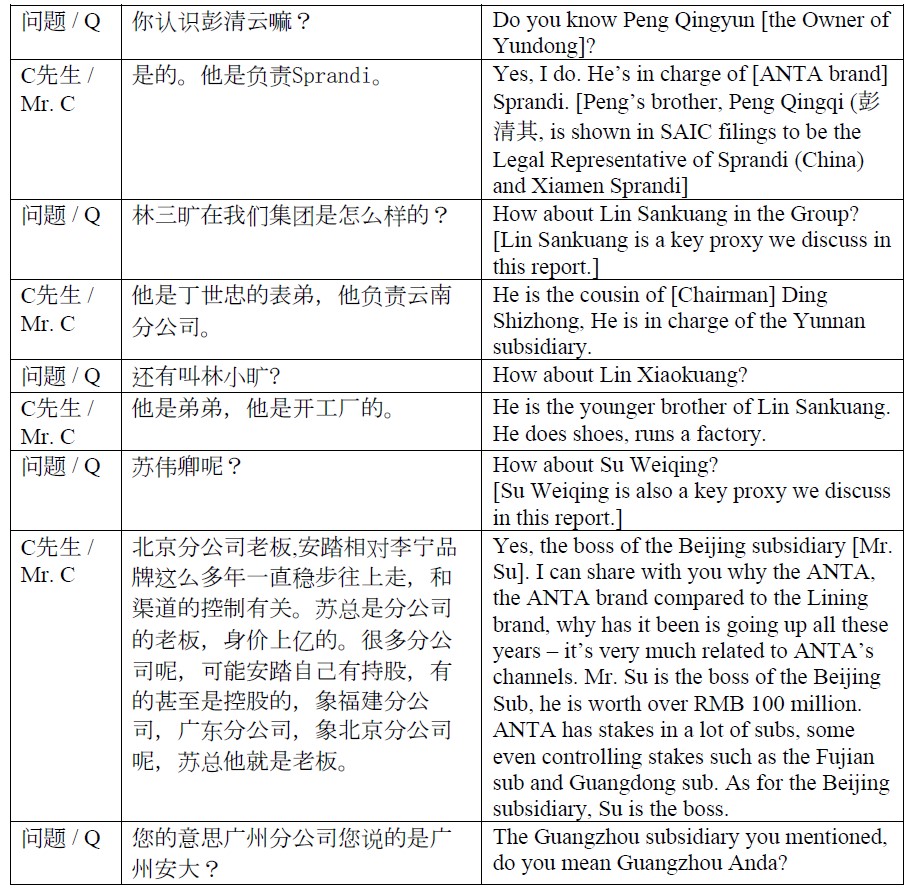

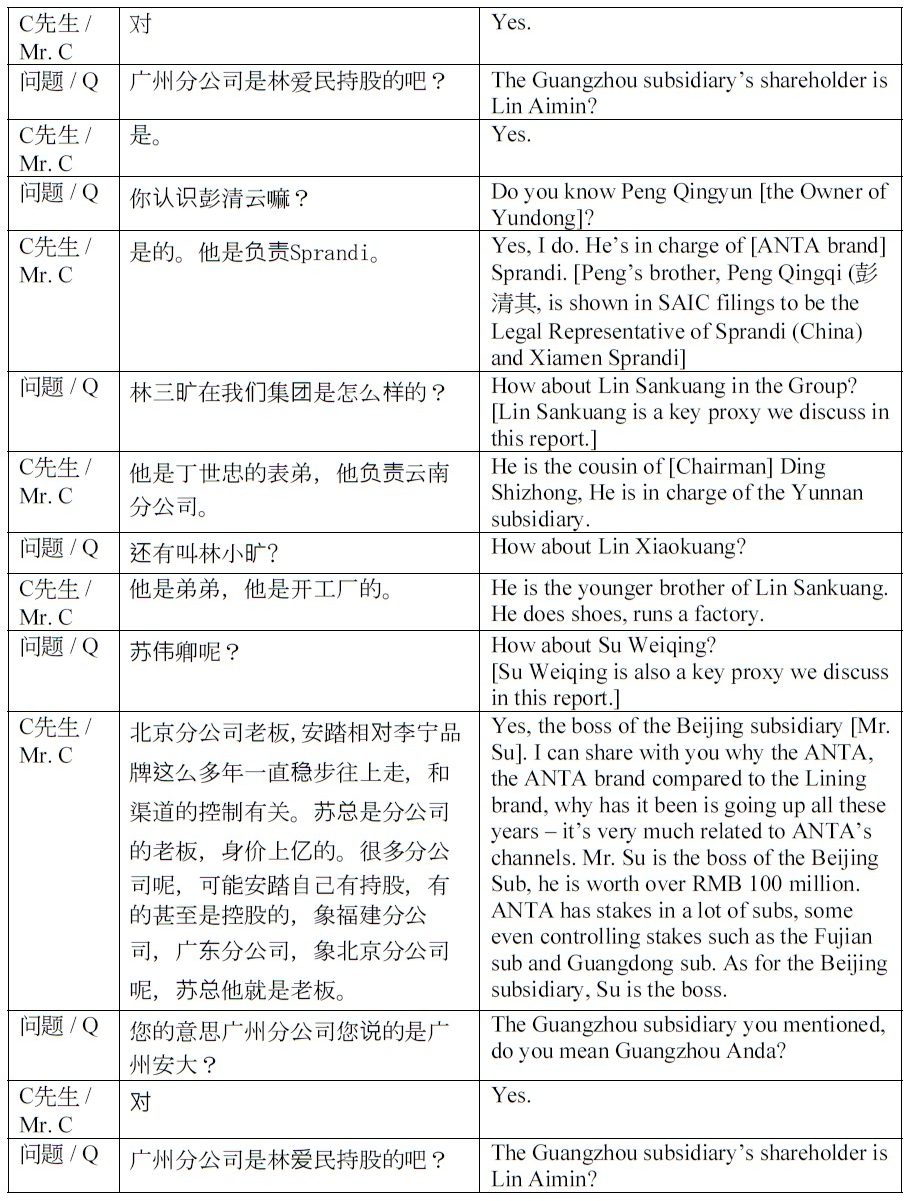

We spoke with four former senior ANTA managers involved in distribution, and one former senior manager of a large distributor, Guangzhou Anda Trade Development Co. ![]()

![]() . We refer to these sources as Messrs. A, B, C, D, and E. They were unanimous in confirming that ANTA controls the distributors. The following are excerpts of these conversations (there are lengthier excerpts with more detail in Appendix B.) Mr. A (former senior ANTA executive):

. We refer to these sources as Messrs. A, B, C, D, and E. They were unanimous in confirming that ANTA controls the distributors. The following are excerpts of these conversations (there are lengthier excerpts with more detail in Appendix B.) Mr. A (former senior ANTA executive):

Mr. B (former senior ANTA executive):

Mr. C (former ANTA senior executive):

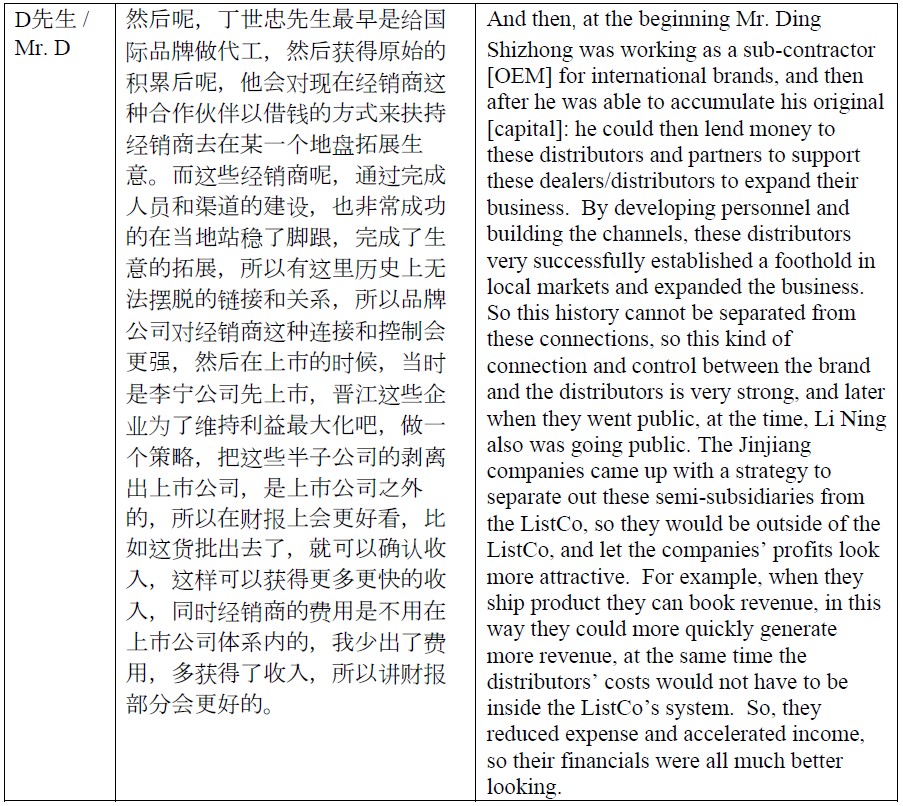

Mr. D (former ANTA senior executive):

Mr. E (former senior executive from major distributor Guangzhou Anda):

Jinjiang Yundong Business Consulting Co. Ltd.

Yundong is an arm of the ListCo, which is shown by the senior roles played in Yundong by two ANTA managers, Li Dan and Wang Huayou. Yundong’s Supervisor is Li Dan ![]() , and she appears to have been so since establishment in March 2008.10 Ms. Li is presently the Legal Representative of nine Fila branches (11 additional branches for which she had been the Legal Representative have been de-registered).

, and she appears to have been so since establishment in March 2008.10 Ms. Li is presently the Legal Representative of nine Fila branches (11 additional branches for which she had been the Legal Representative have been de-registered).

Yundong’s General Manager is Wang Huayou ![]() , who was listed in ANTA’s prospectus as a senior company manager.11 Similar to Li Dan, Wang Huayou has been the Legal Representative of 82 FILA stores, 39 of which were de-registered.

, who was listed in ANTA’s prospectus as a senior company manager.11 Similar to Li Dan, Wang Huayou has been the Legal Representative of 82 FILA stores, 39 of which were de-registered.

As shown below, Yundong is located in ANTA’s Jinjiang industrial park, and its recruiter uses an anta.cn email address.

Read the full article here by Muddy Waters