A Recipe Only As Good As Its Ingredients

This research note was originally published by Investments & Pensions Europe (IPE). Here is the link.

Q4 hedge fund letters, conference, scoops etc

Summary

- Investors have leaned towards multi-factor over single-factor products in recent years

- The factor selection and portfolio construction of multi-factor ETFs can be challenged

- Multi-factor ETFs often feature factors, such as growth, which are not supported by academic research while lacking exposure to established ones such as quality and momentum

Introduction

Investors showed a strong preference for multi-factor over single-factor products in 2017 and 2018, according to FTSE Russell’s annual industry survey, especially if new to factor investing. Some 87% of these allocated to multi-factor portfolios.

This trend can partially be explained by the poor performance of the value factor over the past decade, which has historically been the favorite factor-investing strategy. Investors experienced that factor investing, also referred to as smart beta, does not necessarily imply better beta. Combining value with other factors would hopefully lead to outperformance with a higher consistency.

However, a similar survey by EDHEC indicated that investors demand further development of multi-factor products, indicating either a lack of instruments or dissatisfaction with existing products.

This article examines the universe, performance, and composition of multi-factor exchange-traded funds (ETFs) focused on the US stock market.

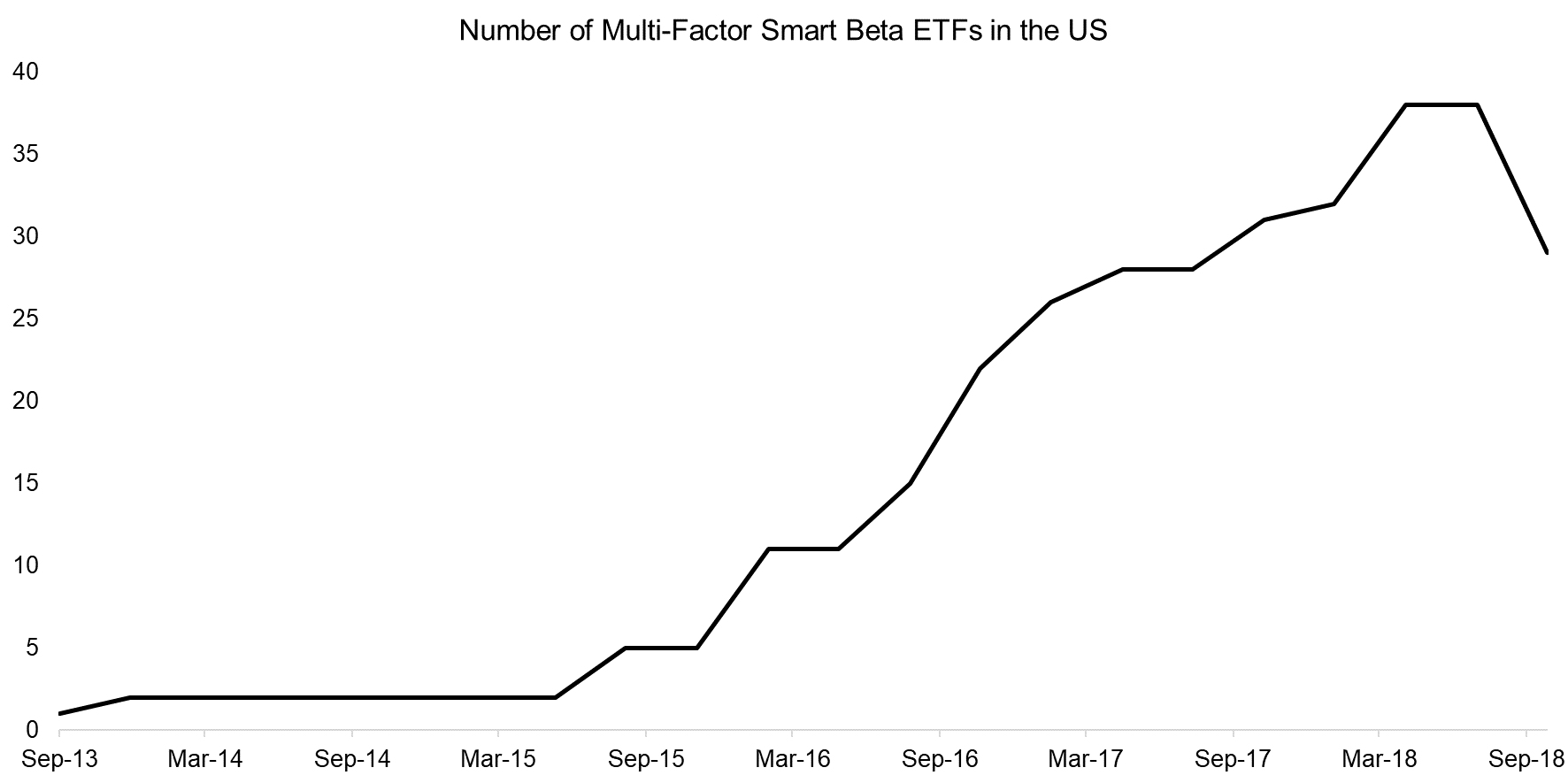

Universe Of Multi-Factor ETFs

The first multi-factor ETF in the US was launched in 2013 and the number of product launches has been relatively moderate, compared with the rapid growth of ETFs for countries, sectors and asset classes, which ranged over 5,000 at the end of 2018.

Furthermore, it is unusual to observe last year’s decrease in available multi-factor products, given the strong investor interest. Product issuers only liquidate ETFs when they fail to reach meaningful assets under management, which is typically a result of poor performance.

Source: FactorResearch

It is worth noting that multi-factor is defined here as providing exposure to at least three factors. There is about double the number of products that focus on two factors like a small-cap value ETF that provides exposure to the size and value factors. Although technically these can be considered multi-factor portfolios as well, they often provide limited diversification benefits, which is the key reason why investors consider multi-factor products in the first place.

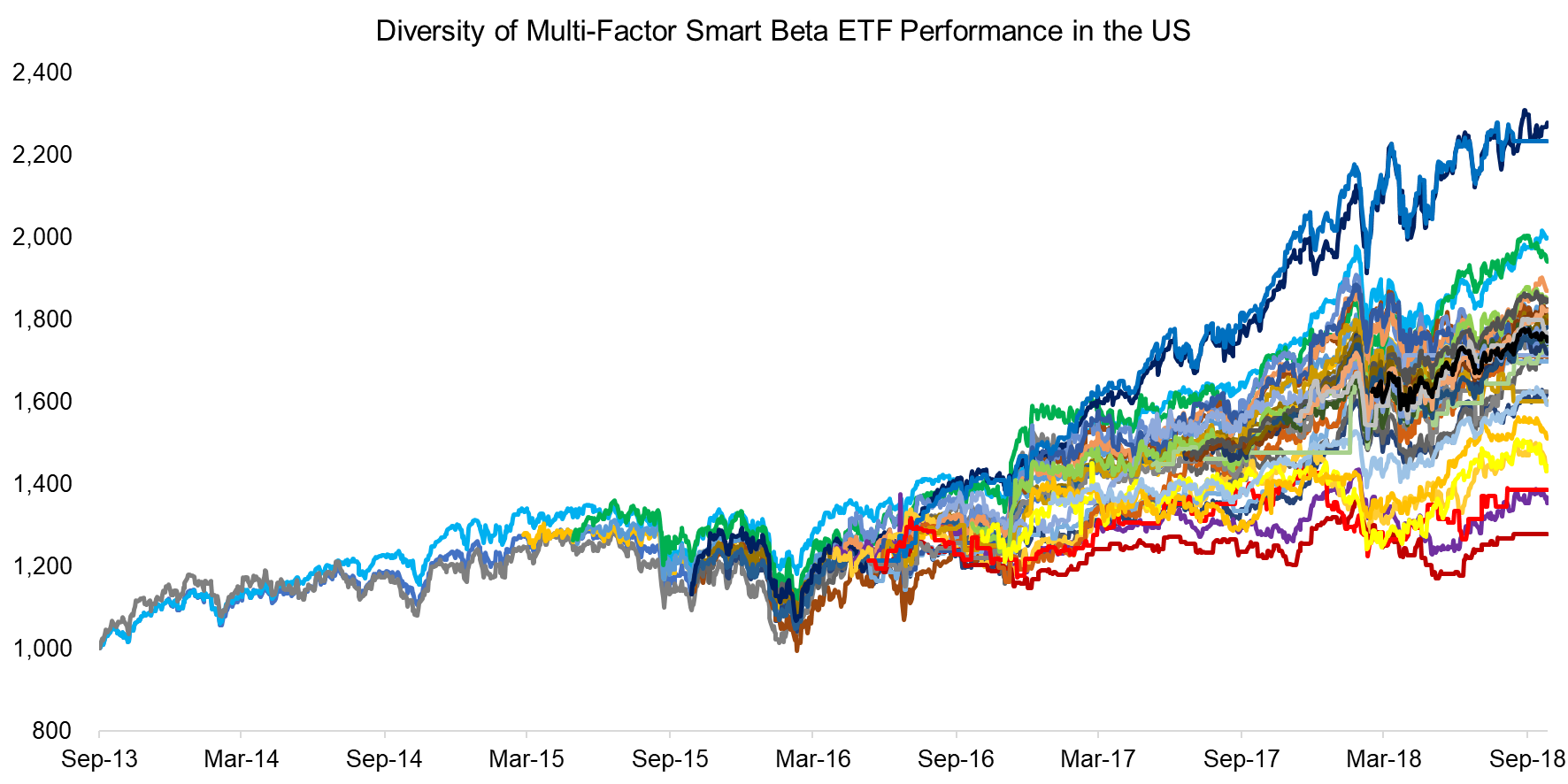

The performance of multi-factor ETFs in the US has been quite diverse over time, which is explained by the fact that these are available for each of the main sectors of the US stock market. Since these ETFs are long-only products they are much more influenced by the sector than factor performance. For example, technology stocks outperformed energy stocks significantly since 2013.

Source: FactorResearch

Analysing Multi-Factor ETFs

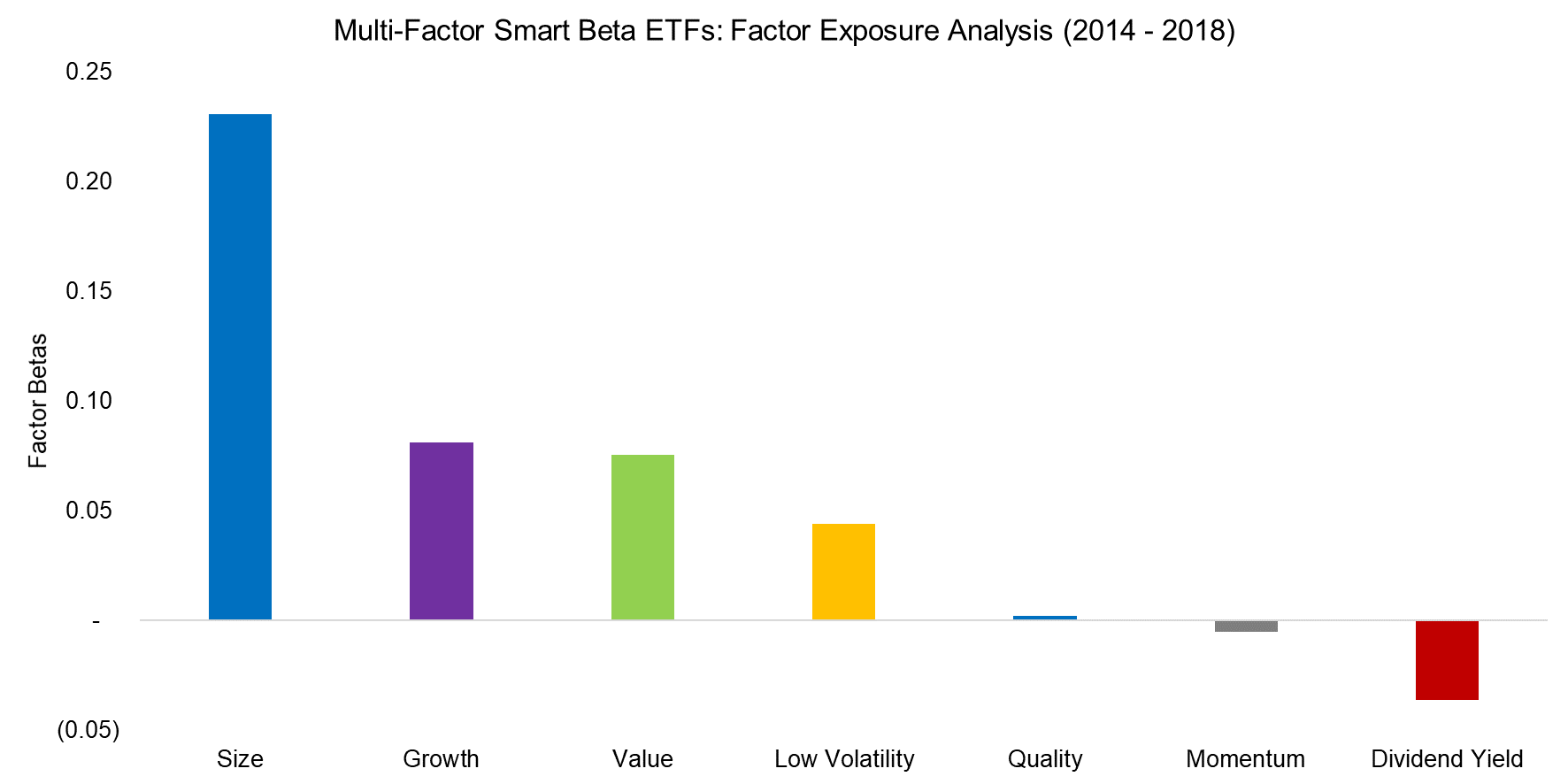

As the name implies, multi-factor ETFs provide exposure to multiple factors. However, the factor selection, definitions, and portfolio construction are discretionary choices of the ETF issuers, which have a meaningful impact on performance.

A factor exposure analysis highlights exposure to common equity factors that we define in line with academic and industry standards. Surprisingly, some exposures do not reconcile well with academic research on factor investing.

Source: FactorResearch

The high exposure to the size, value, and low-volatility factors is to be expected since these are all supported by academic research but the exposure to growth is unusual, as there is no theoretical foundation that supports positive excess returns from this factor.

Some factors show low correlations and are synergistic when combined – value and momentum, for example. Sorting for cheap stocks that are rising helps to avoid businesses that have no future, so-called value traps. However, there are few stocks that are trading at low valuations and are showing strong growth in earnings or sales. Stocks such as Amazon or Netflix tend to trade at high valuations. Therefore, growth and value are partially the inverse of each other, which makes combining these more challenging.

However, it is worth noting that the growth factor also features prominently among single-factor ETFs. The assets under management in growth products eclipsed those in value last year, indicating that investors seem to be ignoring the academic research that created the theoretical foundation for factor investing.

There is also a lack of exposure to the quality and momentum factors that are supported by research. Quality can be defined in many ways, which perhaps explains the low exposure, as measuring it becomes more difficult. In contrast, the momentum factor features highly homogeneous definitions across index providers that make the lack of exposure challenging to explain.

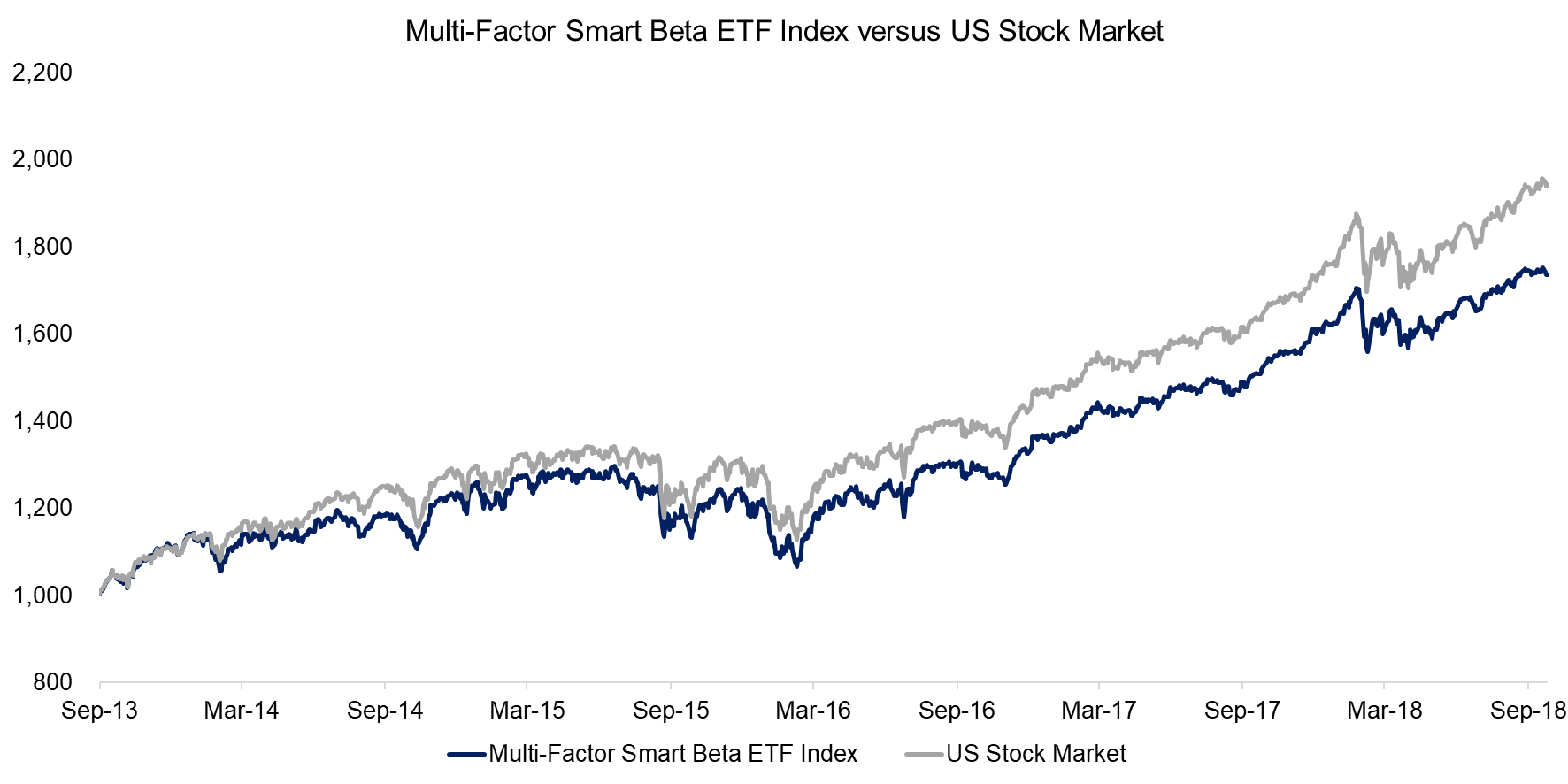

Performance Of Multi-Factor ETFs

Investors allocate to factors to beat their benchmarks by harvesting abnormal returns. Given that single factors are as cyclical as equity markets and experience multi-year drawdowns, it is intuitive to combine these and hope for a more consistent outperformance.

The analysis below highlights that an equally-weighted index of multi-factor ETFs in the US performed comparable to the stock market between 2013 and 2016 but underperformed thereafter. The lack of outperformance can likely be explained by management fees and factor exposure. The ongoing price war between ETF issuers has reduced fees for plain-vanilla equity ETFs such as for the S&P 500 to almost zero, with the first true zero-fee ETFs appearing on the horizon. Factor-based ETFs are much cheaper than actively-managed mutual funds but charge from 9-70bps in fees a year, which impacts performance negatively compared with an almost zero-fee index.

The factor exposure analysis indicated high exposure to the size and moderate exposure to the growth, value and low-volatility factors. Although growth stocks have done well since 2016, the low-volatility factor was essentially flat, while small and cheap stocks underperformed.

Source: FactorResearch

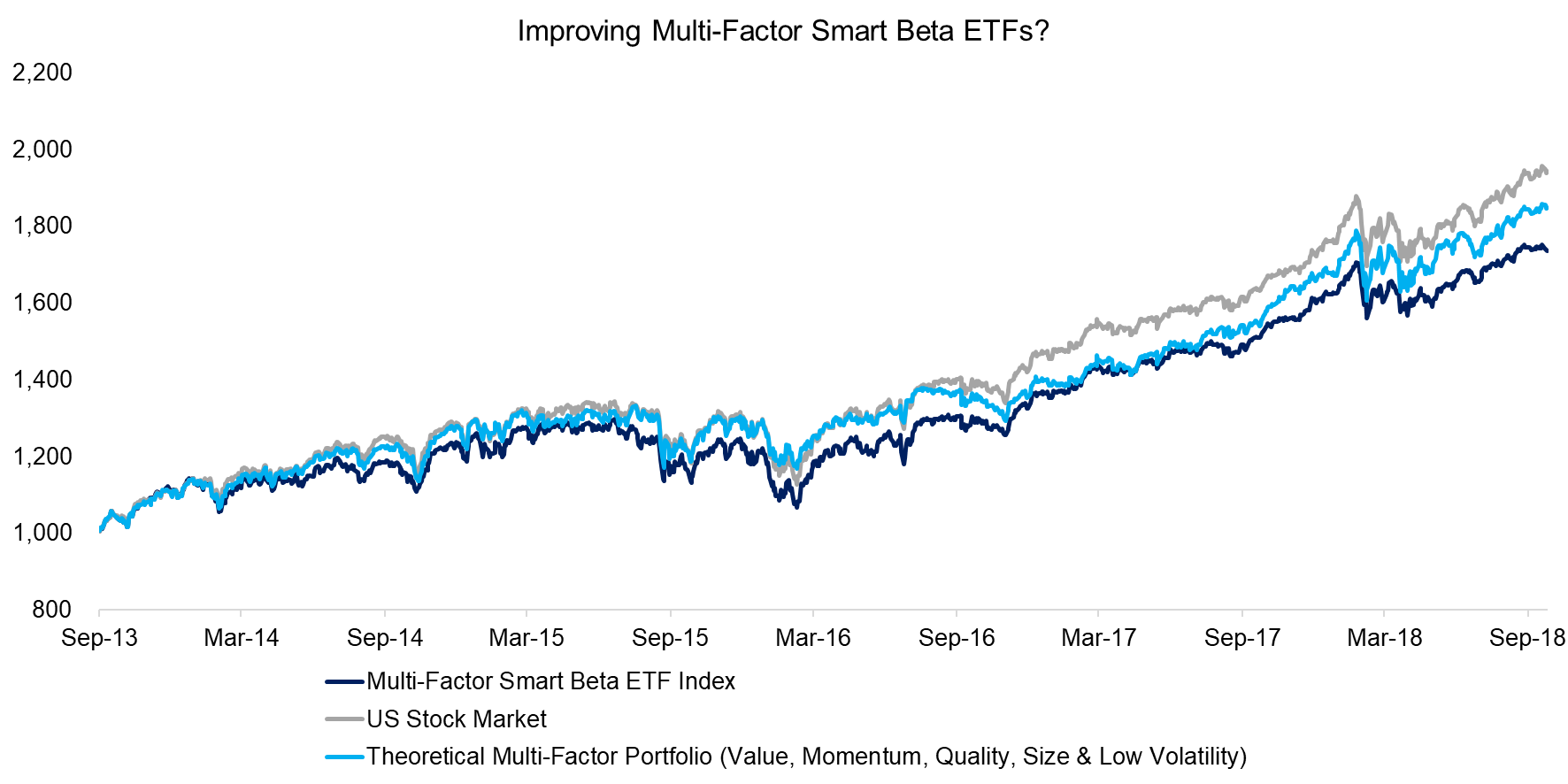

The factor selection and portfolio construction of multi-factor ETFs can be challenged. Investors might question if a portfolio more in tune with academic literature would have fared better. Factor investing research supports the following five factors: value, size, momentum, quality and low volatility.

Naturally, none of these factors works all the time and each experienced long periods of underperformance as evidenced by value over the last decade. Some factors such as size have become less popular, while others like low volatility gained in status in recent years. However, broadly speaking, these five factors are supported not only in equities, but also across asset classes.

We therefore construct a simple multi-factor portfolio based on these five factors and weigh allocations equally with monthly rebalancing. We include transaction costs of 10 basis points on stock level when creating the factors, an annual management fee of 0.50%, and only focus on stocks with market capitalizations of larger than $1 billion.

Although this portfolio did not generate higher returns than the market, it showed less underperformance that can likely be explained by a more diversified factor exposure.

Source: FactorResearch

Further Thoughts

There is a lot to consider in relation to the composition and performance of multi-factor ETFs in the US stock market. Perhaps the most interesting insight is that these products feature factors such as growth that are not supported by academic research and lack exposure to established ones like quality and momentum.

Although the factor selection and portfolio construction of these products can be challenged and improved, there is no easy fix for the lack of performance. Common factors such as value and momentum struggled to generate attractive returns over the last decade. It is difficult to produce a delicious dish even with a great recipe when the basic ingredients lack flavour.

Related Research

About The Author

Nicolas Rabener is the Managing Director of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Article by Factor Research