The challenges of regression analysis

Q3 2020 hedge fund letters, conferences and more

SUMMARY

- There are few alternatives to regression analysis when explaining investment performance

- Too few as well as too many independent variables can be problematic

- The results are often not intuitive, but also encourage asking further questions that may prove insightful

INTRODUCTION

The older I become, the less I feel I know anything with certainty. Almost every aspect of life seems to have various degrees of grey rather than being black and white. Most knowledge seems to peel away like an onion at closer inspection and highlights different shades, but rarely an ultimate truth.

For example, eating sushi for lunch feels better from a nutritional and calorie perspective compared to eating a cheeseburger or a pizza. However, tuna tends to contain heavy metals and salmon nasty pesticides that are both likely detrimental to our health. So, is eating sushi good or bad for our health? Or should we prefer the cheeseburger? Tough to say.

Similar questions arise when analyzing the performance of investment portfolios. Even simple portfolios, e.g. a traditional one comprised of equities (60%) and bonds (40%), can be dazzling complex when inspected closely. Isn’t the equity allocation responsible for most of the portfolio risk? Which asset class contributed most of the returns? And are those explained by plain beta or a tilt to certain factors?

The classic approach to answering such portfolio analysis questions is by conducting a contribution analysis via factor exposures. However, this often raises more questions than it provides answers to.

In this short research note, we will explore some of the challenging aspects of regression-based factor exposure analysis.

PORTFOLIO SELECTION

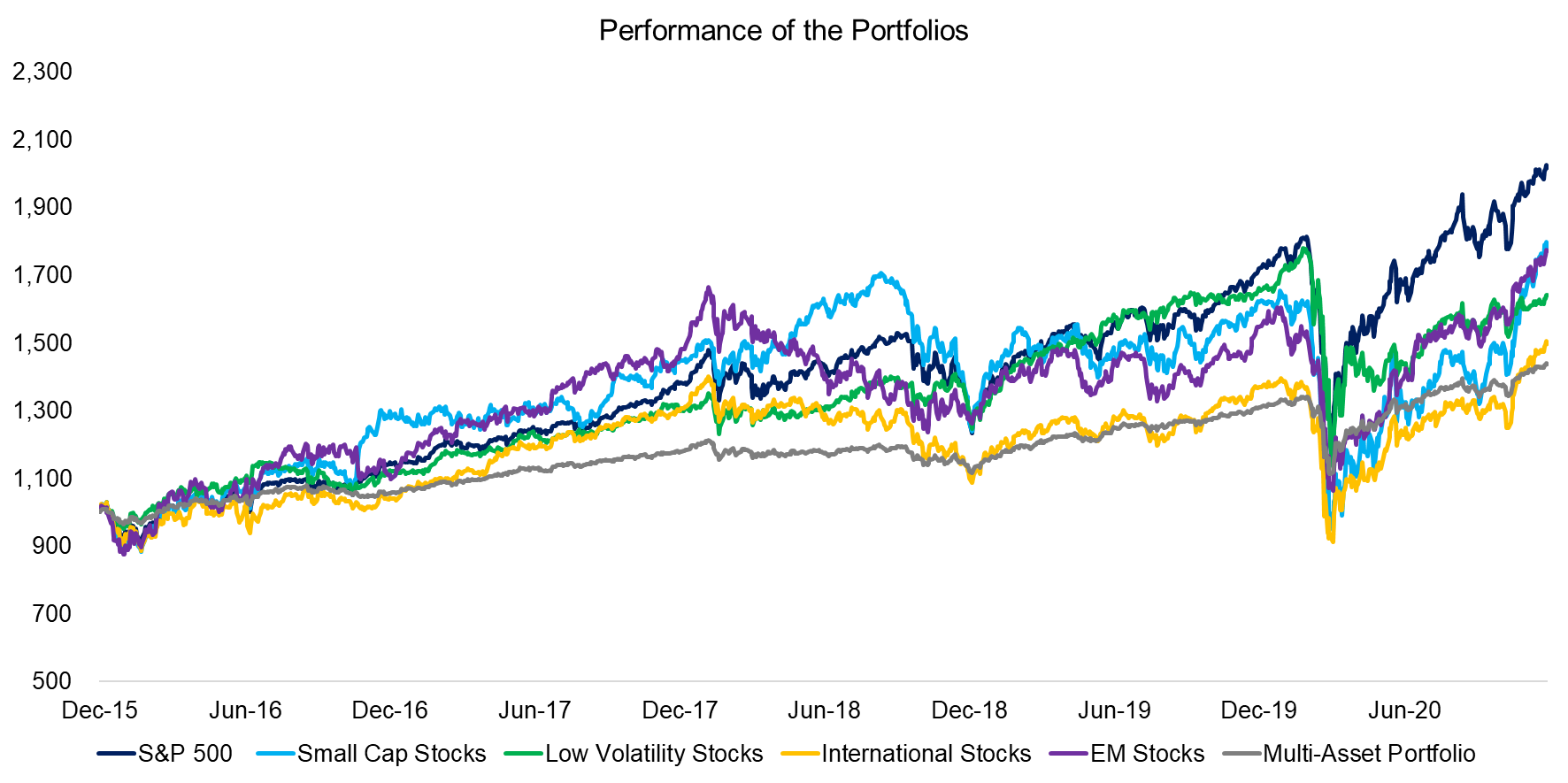

We will explore factor exposure analysis by primarily focusing on six simple portfolios comprising US large-cap stocks (S&P 500), US small caps, US low-risk stocks, international as well as emerging market (EM) stocks, and a multi-asset portfolio.

Comparing the performance of the six portfolios in the period between 2015 and 2020 highlights similar trends. The S&P 500 generated the highest returns, but it depends on the lookback period, e.g. EM stocks outperformed in the first two years. It is interesting to note that even the multi-asset portfolio exhibited the same performance characteristics, which indicates a significant allocation to equities.

Source: FactorResearch

SIMPLE FACTOR EXPOSURE ANALYSIS

First, we conduct a simple regression-based factor exposure analysis using only two indices, which are a market capitalization-weighted index for global stocks and a composite bond index that is comprised of US government, corporate, and high yield fixed income securities.

We observe that the R2 was high for US large caps, international stocks, and the multi-asset portfolio, but slightly lower for the other portfolios. Given that five out of the six portfolios are exclusively comprised of stocks, it is not surprising to see a high positive exposure to the global equity index.

Somewhat more unusual is the negative bond exposure of small caps and positive exposure of low-risk and EM stocks. Intuitively, equity portfolios should not have exposure to fixed income. If there was positive exposure, then this would imply reduced diversification benefits when combining stocks and bonds. Thus, negative exposure means additional exposure to similar drivers as those of equity exposure.

Source: FactorResearch

DETAILED FACTOR EXPOSURE ANALYSIS

Next, we separate the global equity index into US, international, and emerging markets and the composite bond index by the type of fixed income instrument. Rerunning the factor exposure analysis with more independent variables seems to result in factor exposures that are more precise, e.g. the equity exposure of emerging market stocks is allocated to the emerging markets equity index.

The aggregate bond exposure reduces for all of the portfolios, except for the low-risk stock portfolio and the multi-asset portfolio. The exposure of the former might be explained by low-risk stocks often coming from sectors like real estate or utilities that are interest-rate sensitive due to high corporate leverage. In the latter case, this simply indicates that the multi-asset portfolio contains bonds.

Source: FactorResearch

DETAILED FACTOR EXPOSURE ANALYSIS WITH FACTORS

Finally, we add five additional equity factors to the regression analysis. Specifically, we include factors that have been identified by academic researchers to explain almost all the out- and underperformance of active managers, namely value, size momentum, low volatility, and quality.

The inclusion of these additional independent variables leads to further changes in the factor betas. We observe that the small-cap portfolio shows a large positive exposure to the Size factor. The bond exposure of low-risk stocks decreased while the exposure to the Low Volatility factor increased.

Source: FactorResearch

IMPROVING R2

We can contrast the changes in the regression analysis by comparing the R2 of the results, which increased consistently when the number of independent variables was increased. However, more variables are not necessarily better as it is difficult to find variables that are independent and also have a sound theoretical foundation for inclusion.

The more independent variables, the higher the probability that the analysis is subject to multicollinearity. For example, the correlation between US, international, emerging stocks, and high yield bonds is relatively high as these provide similar risk exposure. This can partially be addressed by residualizing the variables or changing the type of regression, e.g. by using a Lasso instead of a simple linear regression.

Furthermore, index construction matters. Many factor indices in the public domain are constructed dollar- and not beta-neutral, which implies that the factors have implicit positive or negative beta exposure. Naturally, this distorts the results of the factor exposure analysis as equity indices represent the market beta.

Source: FactorResearch

CHALLENGES OF FACTOR EXPOSURE ANALYSIS

So far we analyzed portfolios that were relatively simple and where returns could clearly be attributed to well-known sources of returns. However, often even stock-based portfolios make contribution analysis challenging.

In order to highlight this, we create three additional portfolios that have more unique characteristics. One portfolio comprises companies that generate almost all revenues in the US while the other two are focused solely on international markets and are differentiated between US and foreign-headquartered firms that have listed their stocks on US exchanges via ADRs, e.g. Alibaba.

Conducting a detailed factor exposure analysis highlights that the returns are primarily explained by the US stock market and the Size factor, which seems reasonable given that the stocks are traded in the US and have small market capitalizations on average. However, it is interesting to note that the portfolio of companies conducting almost all their business outside of the US has almost zero exposure to international stocks markets. Why is there no positive exposure?

Furthermore, there is also positive exposure to US government bonds. Why? Given that these portfolios are comprised of risky equities, it is difficult to fathom why these stocks should behave like safe US treasuries.

Unfortunately, there are often no obvious answers for explaining some of the unusual results of factor exposure analysis. However, it is worth paying attention to the R2 and p-values as these indicate that in many cases that the model overall is not good at explaining the returns, like for the ADR-based portfolio, or that some of the individual factor betas are statistically not significant and can therefore be ignored.

Source: FactorResearch

FURTHER THOUGHTS

The earliest form of linear regression calculations were conducted more than 200 years ago by the French and German mathematicians Legendre and Gauss, in 1805 and 1809 respectively. There have been some advancements in the methodology since then, but these were rather evolutionary than revolutionary.

The exponential increase in data and better computing power have led to significant learnings in the machine learning space, where many concepts are based on regression analysis. However, none of these newer methodologies seems to be a better alternative to plain vanilla regression analysis for analyzing the returns of investment portfolios.

The methodology has plenty of flaws and often results in output that is not intuitive. However, it also leads to asking additional questions and conducting further analysis, which often results in a better understanding of what has been driving the portfolio performance.

RELATED RESEARCH

ABOUT THE AUTHOR

Nicolas Rabener is the founder & CEO of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Connect with me on LinkedIn or Twitter.

Article by Factor Research