You may have heard the news that Abbvie (ABBV) is in talks to acquire biotech Allergan (AGN) in a transaction valued at $60 billion. Abbvie will offer $120.30 in cash plus 0.8660 in Abbvie shares for each Allergan share.

Q1 hedge fund letters, conference, scoops etc

As someone who already owns shares in Abbvie, it is good to monitor any developments around the company. I am a buy and hold investor who will hold through anything, as long as my dividends are at least maintained. My position in AbbVie is a result of the split of legacy Abbott Laboratories in 2012 into AbbVie and Abbott. I haven’t added to my position in either company since. I do monitor both companies however, as part of my ownership rituals.

When I analyzed Abbvie in September of last year, I did mention the following:

Perhaps Abbvie could similarly acquire growth through acquisitions as well. Hopefully they do not overpay for those acquisitions, and do not decide to cut the dividend in the meantime.

This deal will allow Abbvie to diversify its revenue stream away from blockbuster drug Humira, which accounts for a very large portion of revenues and earnings. Humira is losing its exclusivity in the US after 2023. This deal will also bring in synergies, and bring in new drugs in various stages of development. The synergies will be mainly from a reducing duplication in SG&A, R&D, and consolidating manufacturing operations. The acquisition price is roughly half what Allergan was going for, when Pfizer walked out of its deal to acquire it a few short years ago. It will reduce the revenues derived from Humira from 60% to 40%.

After the announcement, Allergan shares went up, while Abbvie’s share price nosedived by over 16%. This decline pushed the dividend yield to 6.50%. The dividend is at 6.10% today. I do not like chasing yield however. I sincerely hope that investors who are buying AbbVie today are doing objective analysis of the situation, and are not being blinded by the high yield, while ignoring potential risks to the future sustainability of the dividend payment.

It looks like the market participants did not like the deal. That is surprising, because the main issue behind AbbVie was its over-reliance on Humira, whose protections have been extended for a while, but are likely to run out in 2022 – 2023. After that, revenues will fall of a cliff, unless new drugs are brought to market to offset the declines, or an acquisition is done. It is possible that investors did not like the deal because of increased debt, because the acquisition price is high, or because the company will have less flexibility in case something goes wrong.

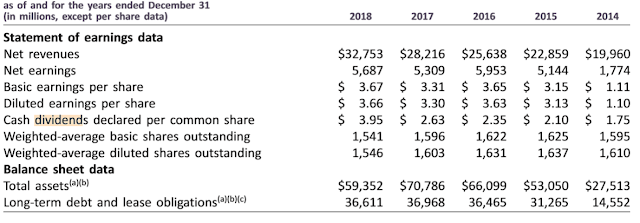

Perhaps it is because this deal will increase Abbvie’s debt significantly, and reduce financial flexibility. My research has identified increased debt following an acquisition spree as one of the factors behind a future dividend cut. I am not predicting that Abbvie will cut dividends, but I do believe that the market considers the risk of a dividend cut to be elevated today, versus last week. Currently, AbbVie’s long-term debt stands at $35 – $36 billion. The company will issue $38 billion in debt to complete Allergan’s acquisition. Allergan also has roughly $26 billion in long-term debt on its balance sheet. That is close to $100 billion in debt.

We cannot just look at debt in isolation of course. AbbVie generated $12.80 billion in free cash flows in 2018, while Allergan generated a little over $5.3 billion in free cash flows in 2018. At least until 2022, the combined company could very likely generate roughly $18 to $19 billion in free cash flows per year. I believe that the number of shares outstanding for AbbVie will increase from 1.546 billion. Allergan has 337 million shares, which would translate to 292 million new AbbVie shares added to the pile, for a grand total of 1.838 billion shares. At the current rate of $4.28/share, we are looking at $7.9 billion going for dividends payments every year. I doubt that the new company will do much in terms of share buybacks. They will be able to reduce the debt by $5 – $10 billion/year, assuming that they do not make another acquisition. Of course, after 2022, Humira’s sales and profits will decline, which means that the situation will get tighter around the ability to pay and grow the dividend. I believe that the dividend is too high today, and that management will likely increase it further from here. This will make the tight situation even tighter by 2021 – 2022. So I do not believe that AbbVie will make a huge dent in its debt by 2023. Perhaps, that will be a catalyst for another acquisition by then.

This analysis of cash-flows is not taking into consideration any cost savings that will be generated by eliminating duplicate functions in corporate departments, R&D and manufacturing. However, it also doesn’t take into consideration increased interest expenses.

It is also possible that the deal strikes as desperation, because Abbvie does not have the drugs to offset the effects of declining sales and profits from Humira after 2023. This is their way of prolonging the existence of Abbvie, and kicking the proverbial can down the road. The price for Allergan is roughly 11 times Free Cash Flow, while AbbVie is selling for roughly 8.50 times free cash flows. Is AbbVie overpaying for Allergan?

Allergan has not grown revenues for a couple of years either however.

| AGN | 2015 | 2016 | 2017 | 2018 |

| Revenues in millions | 15,071 | 14,571 | 15,941 | 15,787 |

The real question for dividend investors today is, “how safe is the dividend”?. My answer is that it depends on how each individual investor decides to evaluate sustainability.

At current rates, the annual dividend is at $4.28/share. As I mentioned above, it is a little high, and could possibly get even higher. But that could pose problems down the road, assuming that revenues and earnings hit a ceiling in 2022, and then start declining. But lets look at GAAP and Non-GAAP earnings first ( after looking at cashflows above)

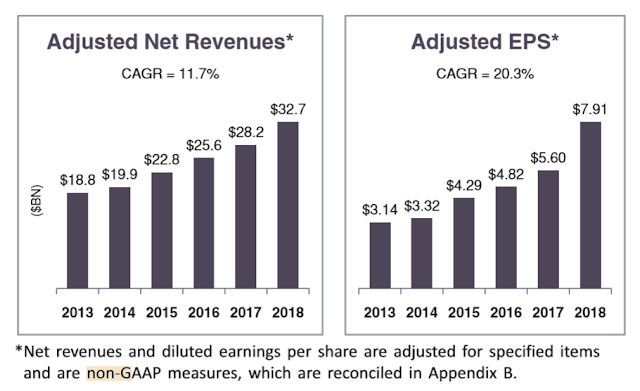

Based on Non-GAAP earnings per share, Abbvie has managed to grow the bottom line since it separated from Abbot at the end of 2012.

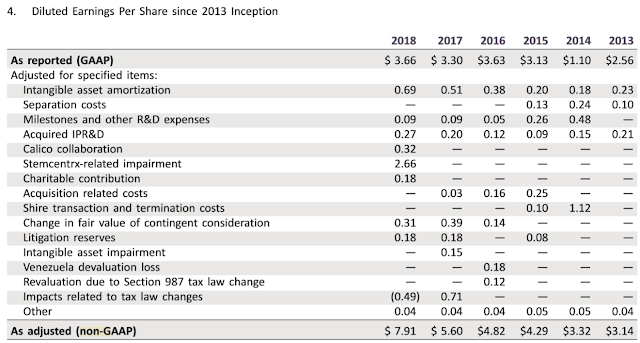

However, if you focus on GAAP earnings per share, it looks like the profits did not increase at all since 2013.

It looks like annual dividends have increased from $1.75/share in 2014 to $3.95/share in 2018. Abbvie hiked its quarterly dividends to $1.07/share in the last quarter of 2018. This brings the annual dividend to $4.28/share.

I do believe that the answer to the questions ” how safe is my dividend” is somewhere in the middle. However, I do believe that the combined company has a lower margin of safety in dividends than before due to increased debt, and more shares being added at the high dividend rate due to the acquisition. It is very likely that any short-term pressures on management due to a more challenging competitive position, or a more challenging economic or financial environment may prompt them to freeze dividends and even cut them if they have to. That being said, the dividend is relatively safe for the next three years or so. My concerns are for the period after that.

The stock price is lower, and could be a bargain today at 8.70 times adjusted non-gaap earnings and a dividend yield of 6.10%. The adjusted non-gaap payout ratio looks ok at 54%. Using GAAP earnings, the P/E ratio is at 19.10 but the dividend payout ratio is above 100%.

However, there is a higher risk of a dividend cut down the road due to increase in debt by an estimated $38 billion, from the current level of long-term debt of $36 billion. There are always risks in integrating two separate cultures, which may reduce the amount of synergies that are actually realized. We also have risks that the existing revenues for Humira decline faster than expected and sooner than expected, pressuring management to pay off debt using funds for dividends and buybacks.

Ultimately, I think that Abbvie may be worth monitoring further. I will monitor the situation and decided if I want to add to my position. For the time being, I am digesting the facts. and weighing the risk of a dividend cut against the possibility for diversifying the revenue stream and the potential for today being a bargain price for the stock. The stock price has been going up since the big decline, which is clouding my judgment even further, creating a fear of missing out mentality.

I am hesitant, because I am evaluating my success based on my ability to generate recurring dividend income that increases above the rate of inflation. If you are an investor who may not worry if a company they buy cuts dividends on them, perhaps Abbvie could be worth further researching. If it turns out ok, similar to how Pfizer turned out after its 2009 dividend cut, good returns could be generated. If it doesn’t however, you will have the double whammy of lower dividends and lower net worth for the portion allocated to Abbvie a few years down the road.

The conclusion I had at the end of my last analysis is still fitting for today’s situation. I stated the following:

I am unsure about adding more to Abbvie at present levels. Abbvie seems like a company that needs closer monitoring, because it is not the type of business where future growth can be taken for granted. On the other hand, the dividend seems sustainable at the moment, and will likely grow for the next four – five years at a high single digit rate. Investors today need to decide for themselves whether the current valuation is attractive enough to outweigh future risks. Either way, investors are getting paid generously to hold onto their Abbvie shares.

What is your opinion on the stock? Are you a buyer of Abbvie, are you holding on to it or are you considering selling? I would love to hear from you! You can hit reply or email me at dividendgrowthinvestor@gmail.com

Relevant Articles:

- Abbvie Dividend Stock Analysis

- Should dividend investors hold on to Abbott (ABT) and Abbvie (ABBV) following the split?

- Six Companies Growing Dividends for Shareholders

- 2019’s Dividend Aristocrats Revealed

Article by Dividend Growth Investor