Introduction

I am a firm believer and ardent supporter of conducting comprehensive research and due diligence on any company (stock) you might consider investing in. However, I have also experienced the reality that far too many investors make their decisions based on opinions, emotions or vague ideas about a company, instead of on comprehensive knowledge and understanding of the business they are considering. Consequently, far too many investors expose themselves to being prone to making significant investment mistakes because they simply do not have the knowledge to keep them from allowing their emotions to rule. In other words, volatile stock price movements can cause them to buy when they should sell – or sell when they should buy.

Q1 hedge fund letters, conference, scoops etc

In contrast, those prudent investors that conduct the requisite research and due diligence are empowered to make rational and sound investing decisions. Furthermore, understanding the business behind the stock also empowers investors to make intelligent and reasoned forecasts of what the business can generate on their behalf in the future. Not the stock price, but the business. In simple terms, these more prudent investors know what their businesses are truly worth. Therefore, they are unlikely to sell when the market is pricing their business lower than it should be, and conversely, unlikely to buy when – and if – the market is pricing their desired company too richly.

Moreover, another issue that I have often come across is the idea that people really don’t know how to comprehensively research a stock. Consequently, they often are deluded by simple statistical references such as P/E ratios or dividend yields without a solid understanding of how those statistics apply to the actual company in question. It’s important that investors recognize that valuation levels, i.e. multiples of earnings, cash flows, etc. are relative. In other words, a company can be trading at, for example, a P/E ratio of 20 and can mathematically be cheaper than a company trading at a P/E ratio of 15. Ultimately, fair valuation is functionally related to the level of future cash flows (earnings) that each respective company can potentially generate. Earnings and/or cash flow growth rates are the keys to understanding fair valuation levels.

Comprehensive Research and Due Diligence: Here’s How to Do It

With all the above said, I was inspired to produce this article because of the excellent research produced by my friend Adam (Dividend Sensei) on the big-box home improvement chains Home Depot (HD) and Lowe’s (LOW). People ask me all the time to explain what comprehensive research and due diligence is. The article found here recently published by Dividend Sensei is a classic example of how research and due diligence should be done. The article provides great insight into the underlying businesses, past, present and future of both Lowe’s and Home Depot.

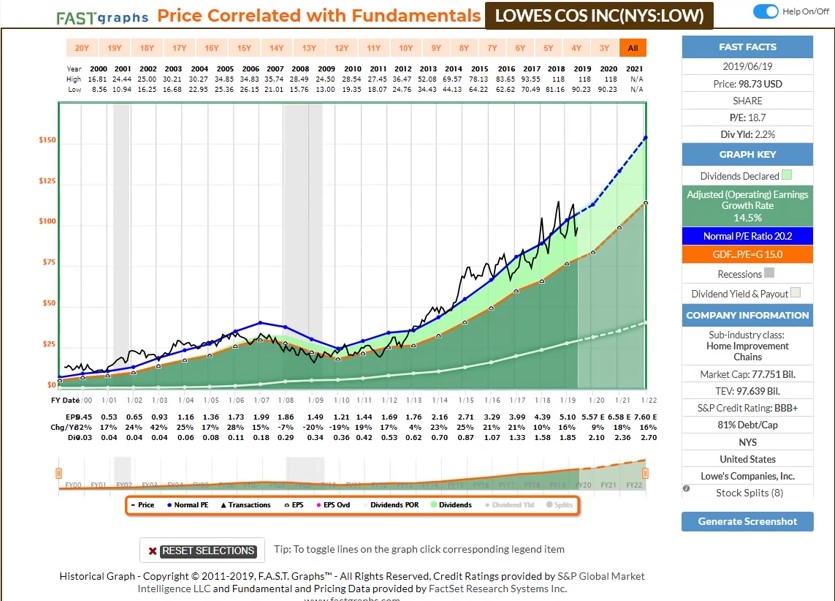

Therefore, I don’t feel that I need to add any further insights into the businesses behind each of these two blue-chip dividend growth stocks. Adam has done an exemplary job with that. However, I do feel that I can contribute an enhanced understanding of the dynamics that both these fast growing big-box retailers provide. In other words, my contribution to Adam’s excellent work is simply to analyze Lowe’s by the numbers. To add further clarity, before I would go through the time and effort that Adam clearly engaged in, I would first run the numbers in order to determine if it justified the effort. Or as I like to say, is the company in question research worthy-or not. To me personally, in the case of Lowe’s, I think it is. However, Adam didn’t convince me to go further with Home Depot. Although I like Home Depot the business very much, I would have to see it at a slightly better valuation before I would be interested in researching it further.

FAST Graphs Analyze Out Loud Video: Lowe’s Cos. Inc.

Summary and Conclusions

From a valuation perspective, I consider Lowe’s fully valued based on intrinsic value calculations and moderately undervalued based on historical normal valuation multiples. However, I would also add that you can pay more (a higher valuation) for a faster growing company then you can for a slower growing one. To put that into a clear perspective, there have been many times throughout Lowe’s history that it traded at a significantly higher valuation than it does today. However, if you did not sell out your position, you would have still made a reasonable amount of money even if you bought it at its highest valuation.

A business capable of growing their earnings as fast as Lowe’s has historically, and more importantly as fast as it is expected to continue growing, will cover up a lot of bad timing decisions. Stated differently, you almost can’t pay too much for company if it grows fast enough. On the other hand, and I consider this critically important, you will make significantly more money and take on less risk if you are more prudent with valuation on the buy side. I believe the above video clearly demonstrates the veracity of those statements. Caveat emptor.

Disclosure: No positions.

Article by F.A.S.T Graphs