Rough notes of Elizabeth Lilly, Allan MacDonald, Paradigm, and Mason Hawkins presentation from the Ben Graham Centre’s 2018 Value Investing Conference.

We will be adding more from both this and Sogn later today so stay tuned

Klarman On

The danger of Chinese leverage

Discipline while value investing in bubby times

Also check out our Sohn Conference notes right here. We will also be adding much more extensive coverage of the event in coming days for Premium readers in particular.

Q1 hedge fund letters, conference, scoops etc

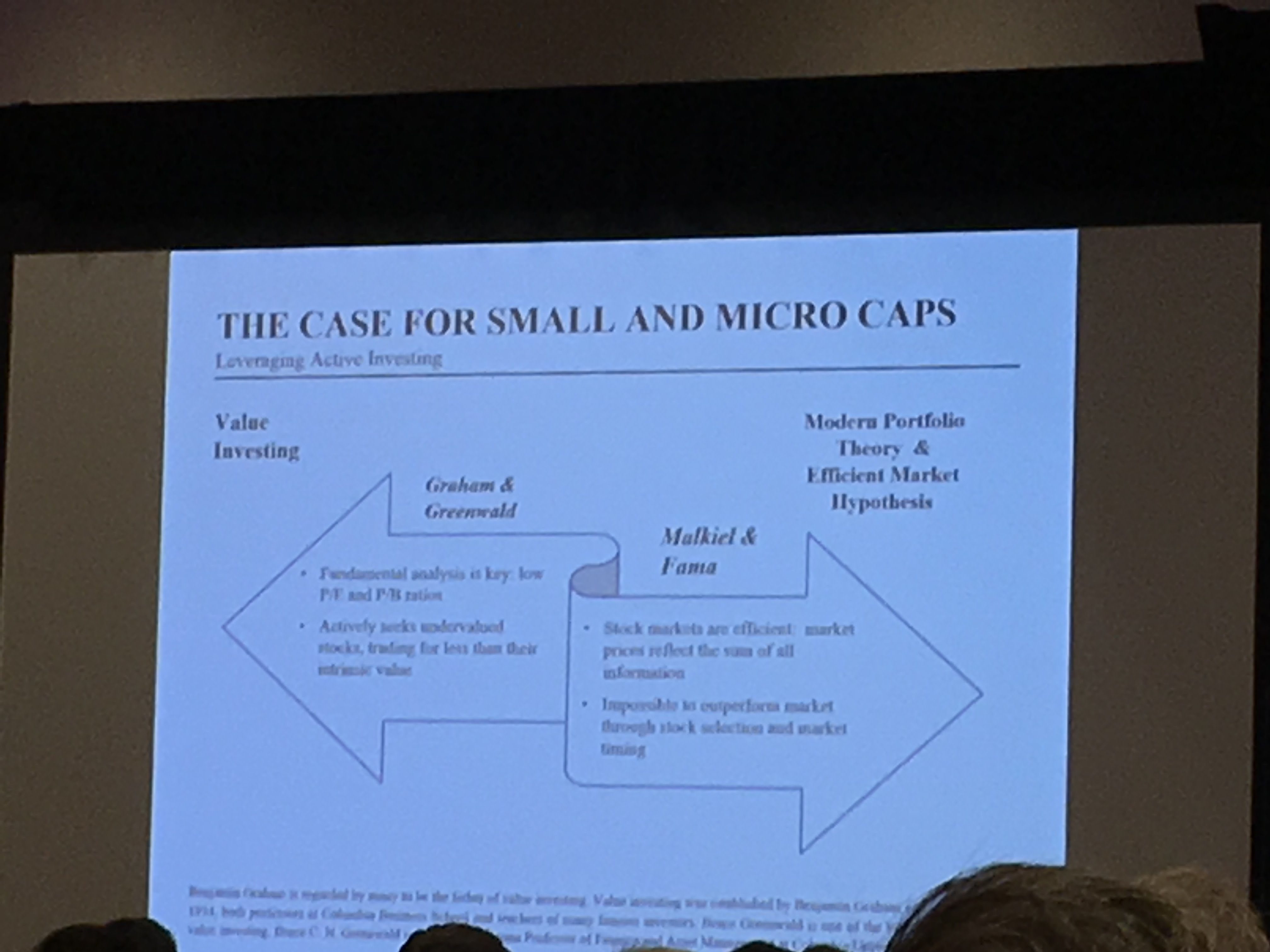

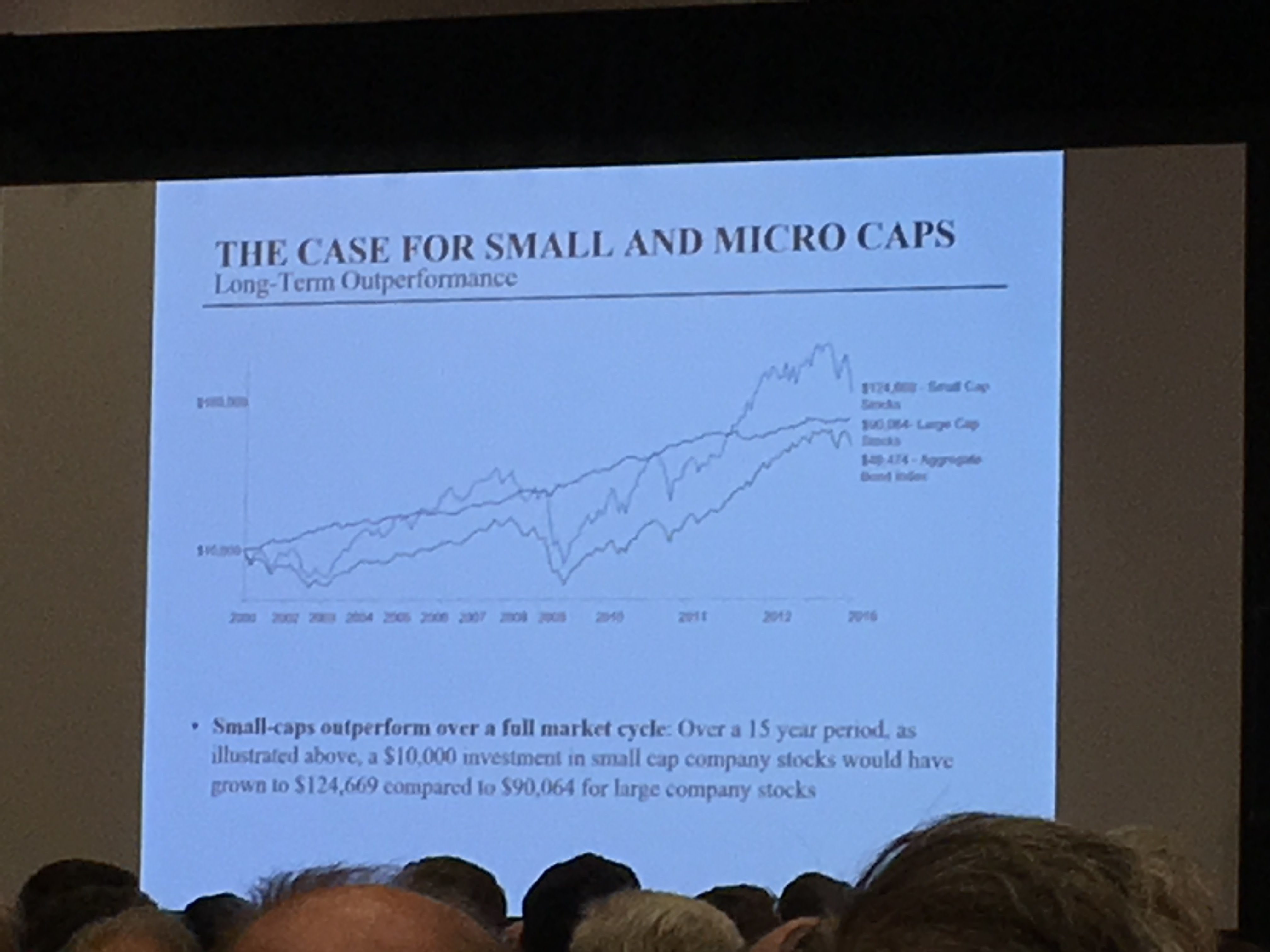

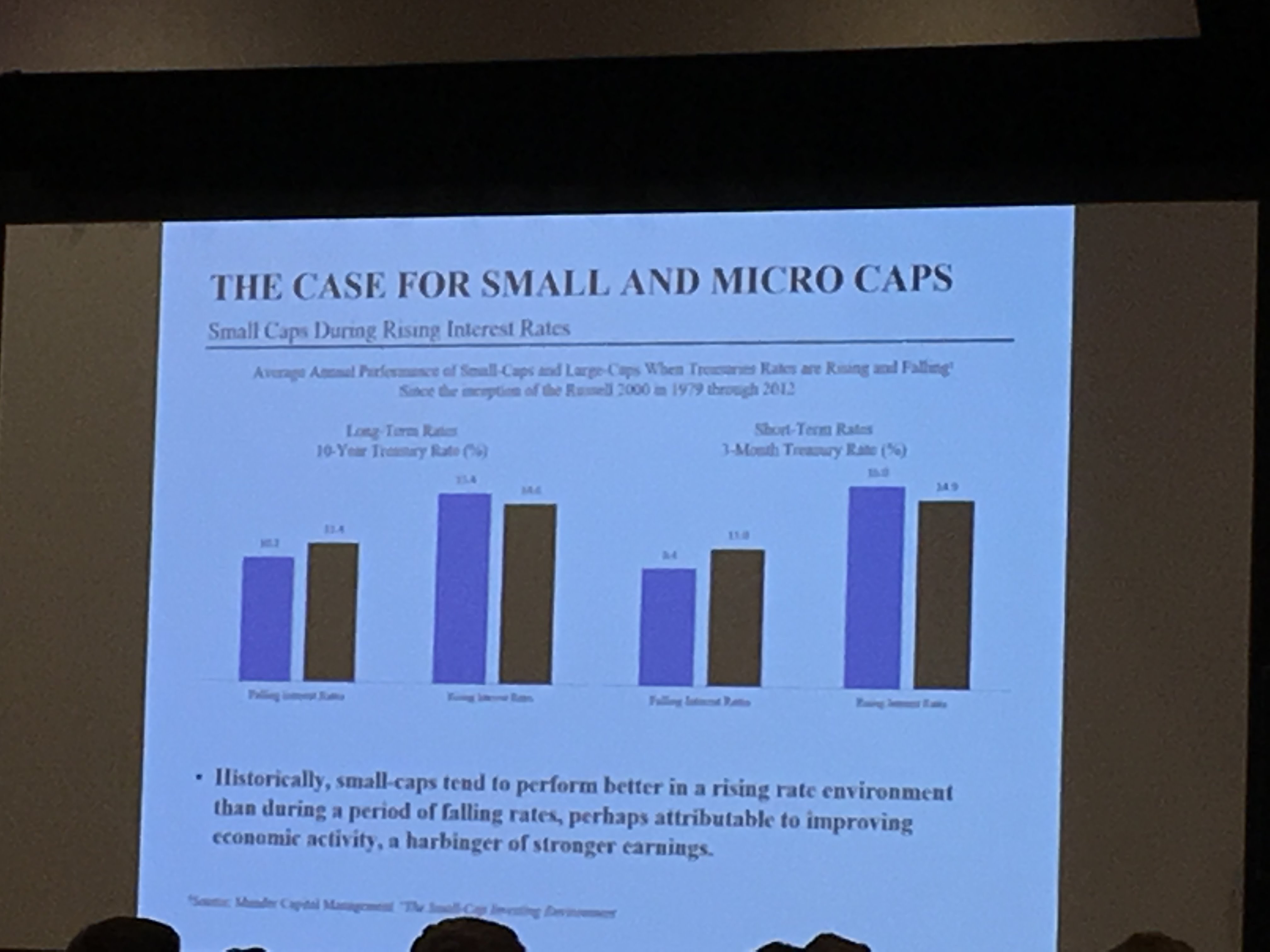

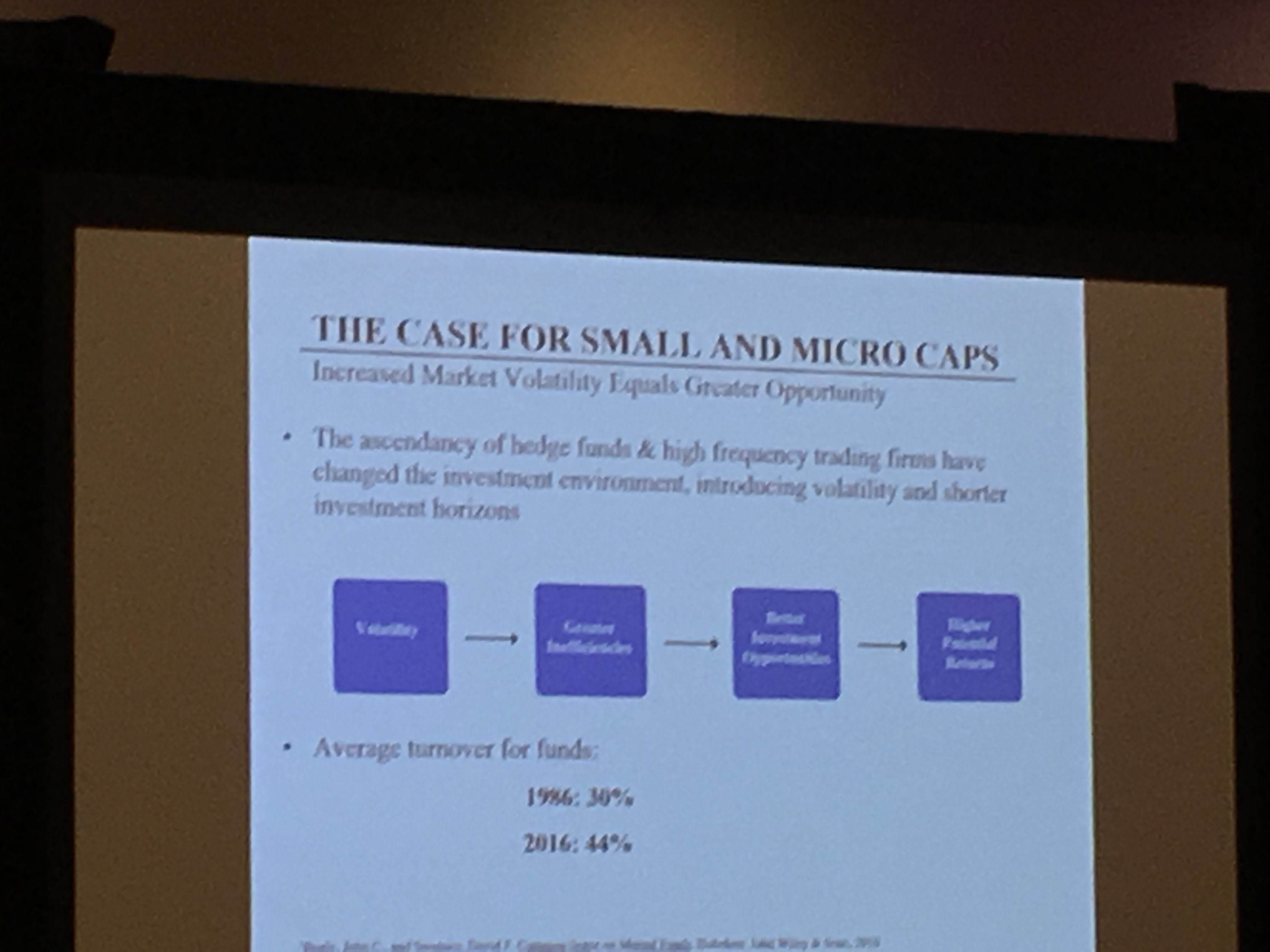

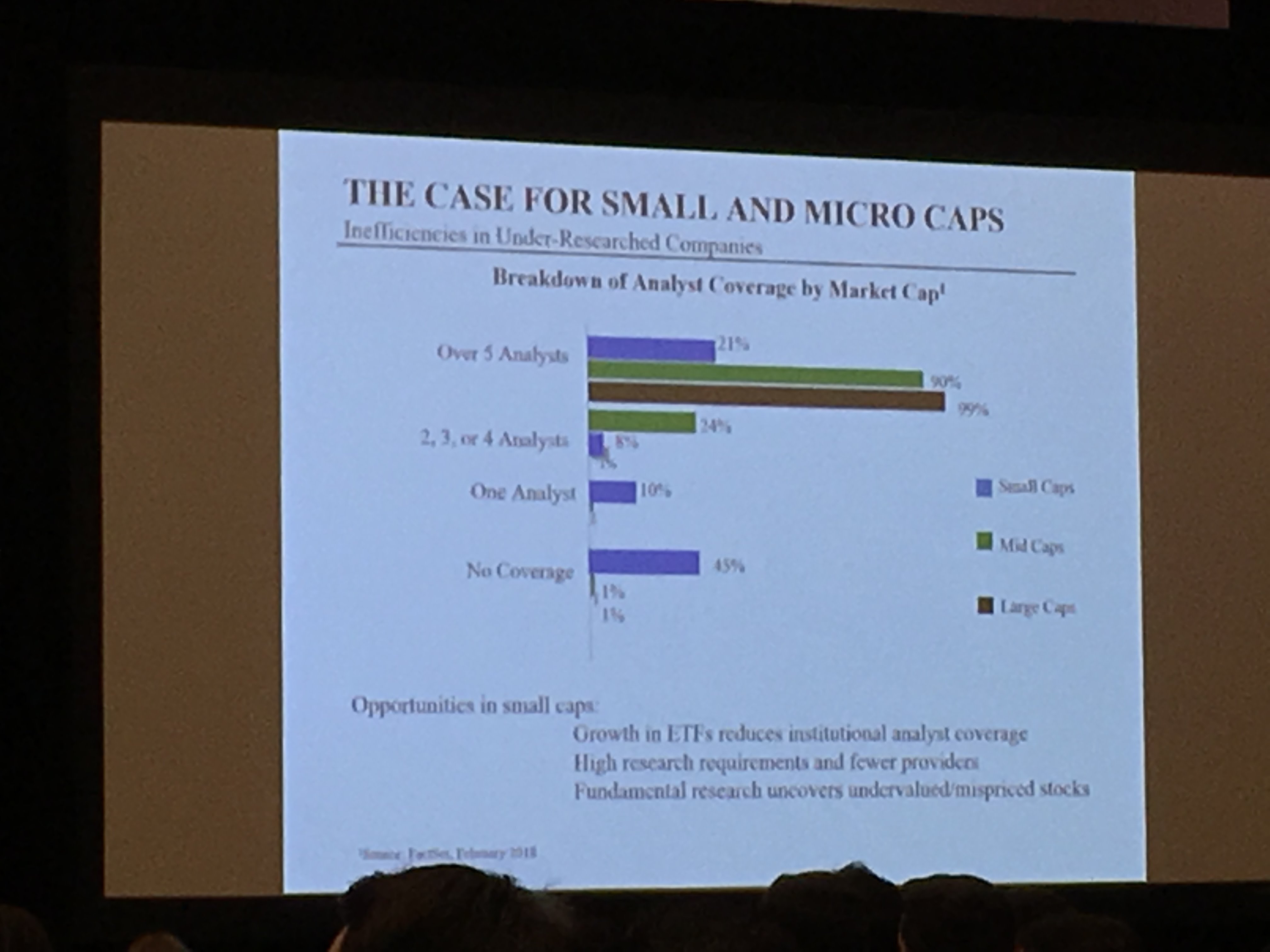

Elizabeth Lilly – Small Micro cap

- Activity, activists, attractive

- 1 year of M&A

- Hedge funds and high frequency higher volatility, short termism (environment they create)

- Average turnover for mutual fund, 44% today vs 30% 1986

- 45% small cap (3 bill market cap) have no coverage

- Information sources and identifying ideas show

- How are you going to grow the business? What are your margins going to be? Explain the disconnect for the valuation

- Look for change that wall street doesn’t appreciate

- Discipline capital allocation process

- Fundamental foundation

- What is it and what is it worth

- Now vs 5 year projection

- EBITDA to peers, transaction comp, DCF remove outliers, use margin safety

- Judge management firsthand, ask distinctive questions, do we want to be their partner

- Understand the business, philosophy of running the business

- What is your edge?

- Informational, emotional, time horizon

- Build mosaic, go where no one goes

- Valuation challenge

- Crocus hills partners

Allan MacDonald, Burgundy Asset Management

- Different business models without comps

- Confirmation bias in industry

- What if there is no comp? potential opportunity

- ONEX- 1990 à misunderstood

- Private equity and LBO misunderstood

- Online travel

- SNC Lavalin Group

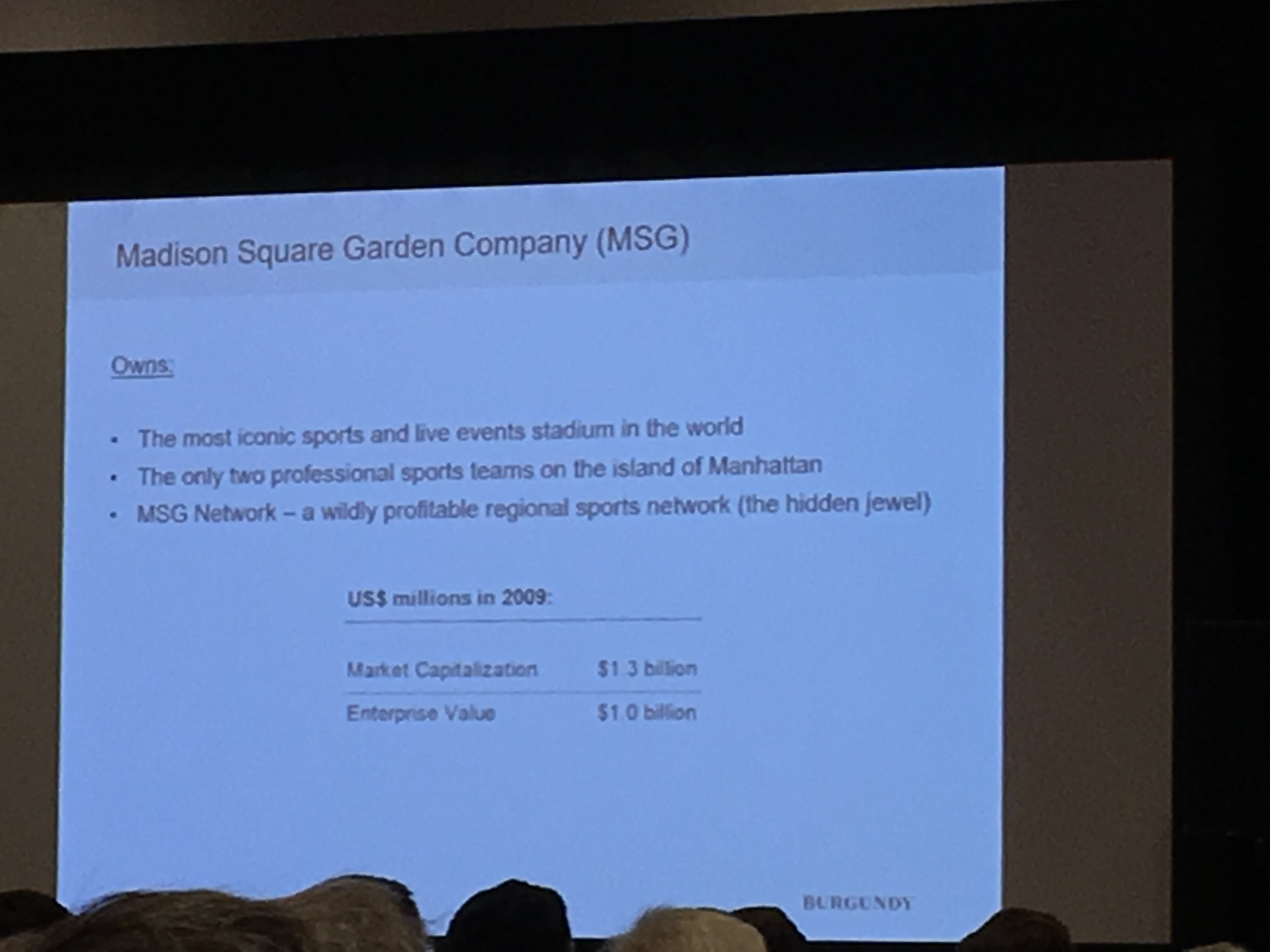

- Madison Square Garden Company

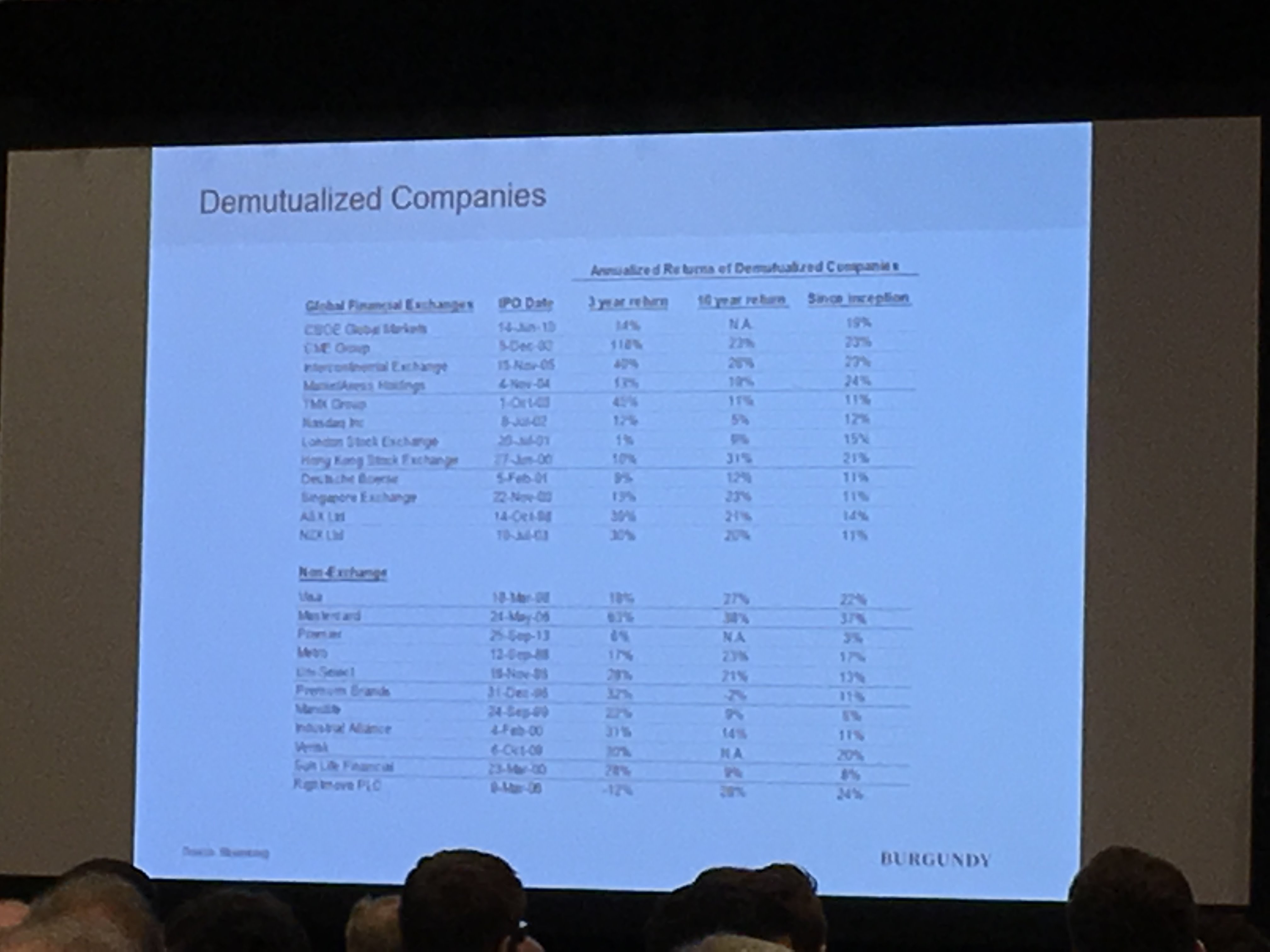

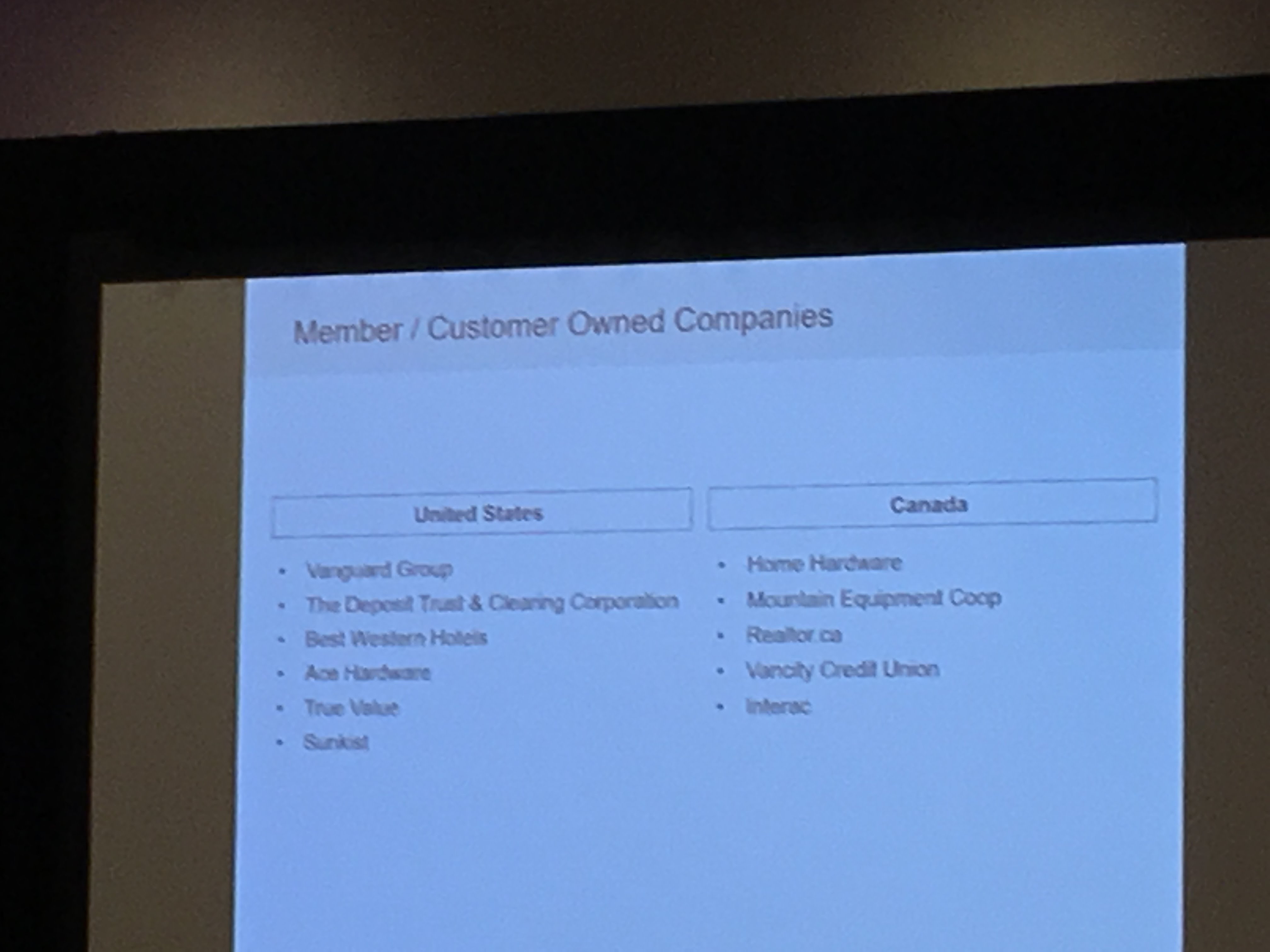

- Demutualization – exchanges

- Non exchange – visa, mastercard, premier, metro, uni-select, premium brands, industrial alliance, sun life financial, rightmove plc, Manulife

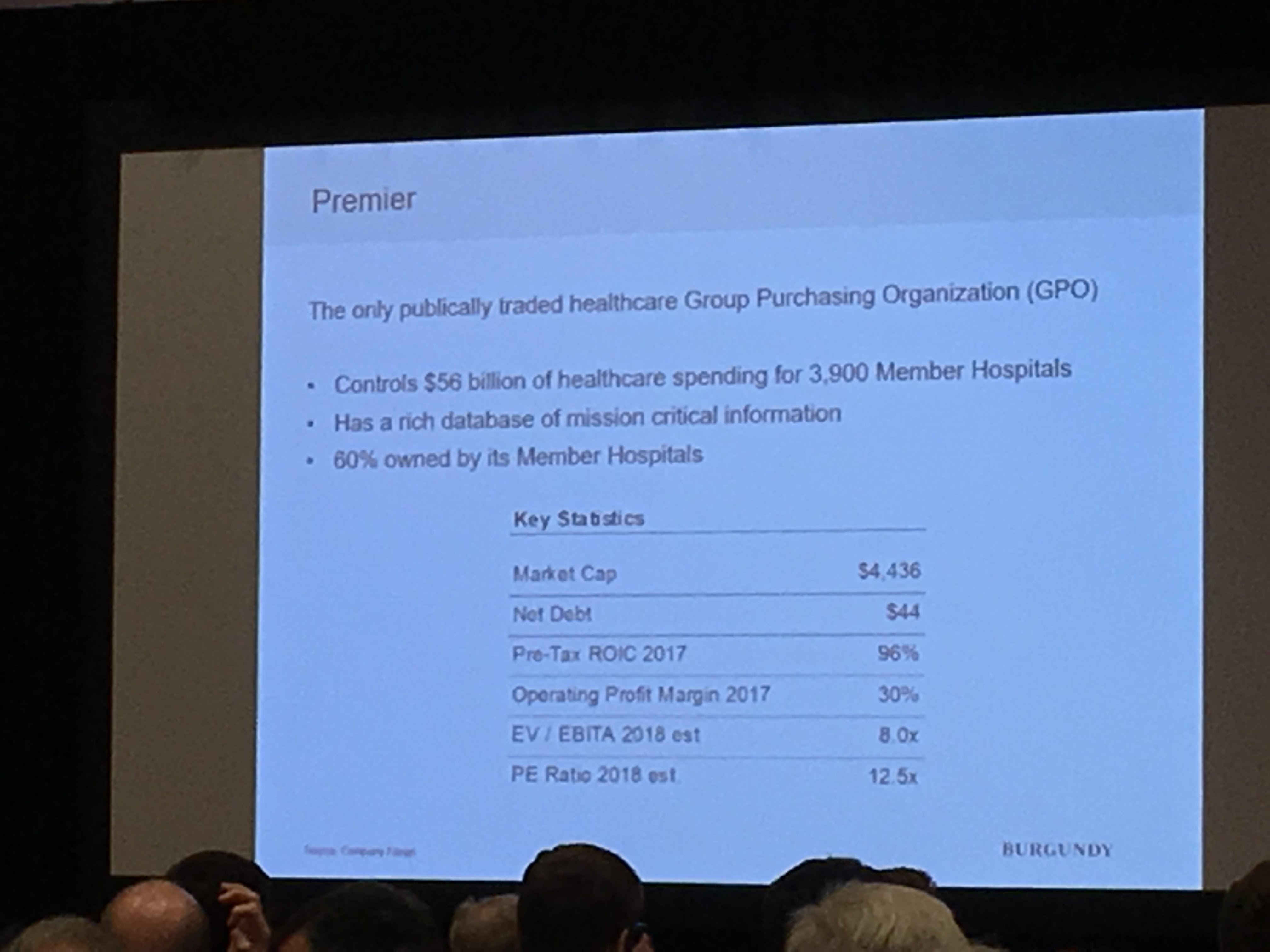

- Premier

- Only publicy tradedhealthcaregroup purchasing organization

- Controls 56$ bill spending 3900 memebers

- Has rich data base of mission cirtical info

- 60% own member hospital

- Net debt $44

- Pre-tax ROIC2017 96%

- Operating profit margin 30%

- Ev/ebitda 8x

- PE 12x

Mason Hawkins, Southeastern Asset Management

- Hold 5 years

- Concentrated 10-20 investments depending on mandates

- The outsiders à focus on building intrinsic value

- Qualitative becomes important over time

- Time is good for good businesses and exposes bad busineses

- Century link

- 1 bill cost synergies

- Start was with level 3

- 25 FCF(1 bill shares, about $3 FCF+ , dividend 2.16

- What do you think long term is today? How does that speak to the challenge of the last 10 years vs before?

- Adjust comps to interest rate environment at the time

- DCF – conservative with all of it, start with CF predictable and reliable

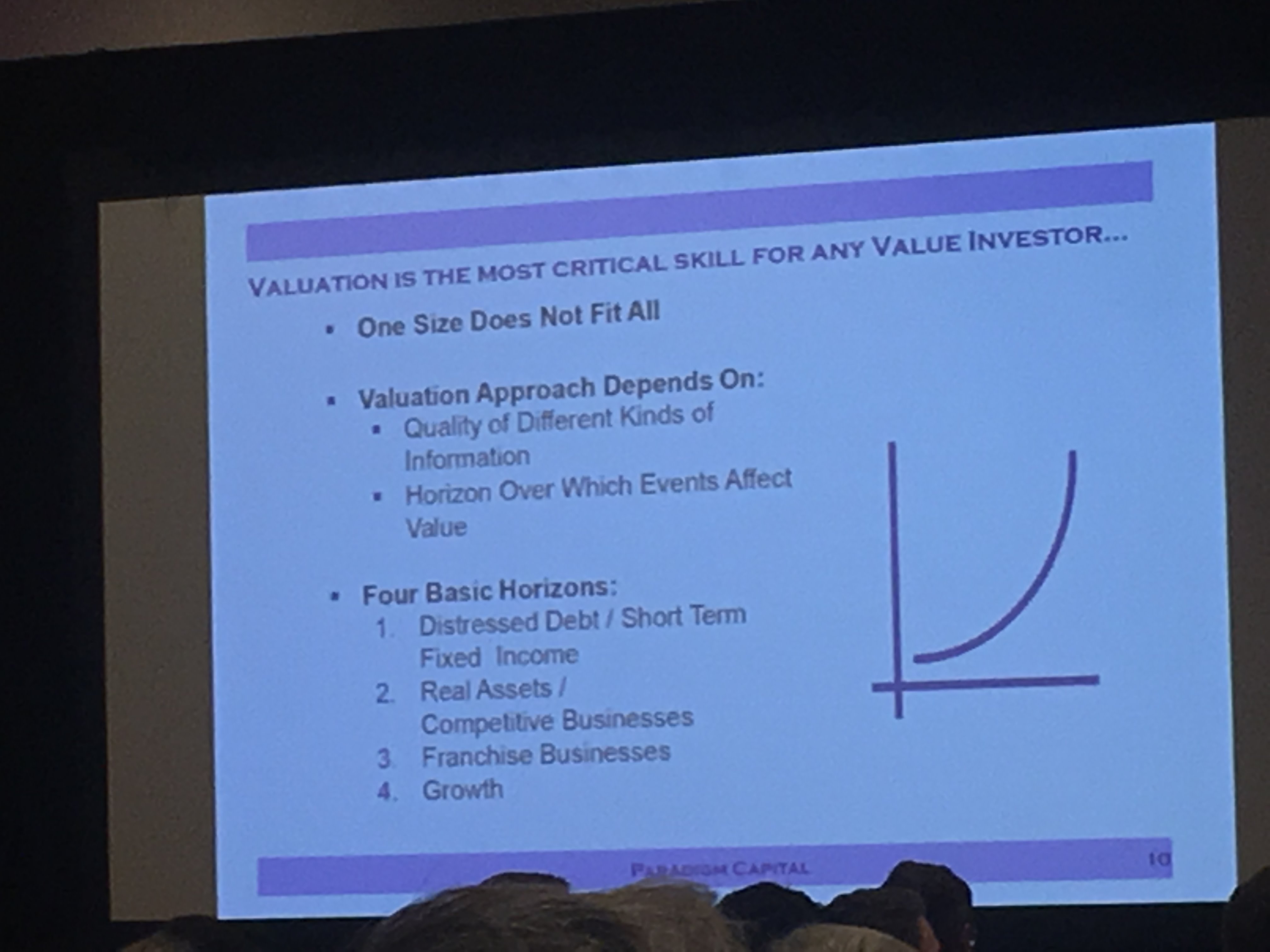

Paradigm Capital,the future of active value investing

- How do we create an edge

- Imperfect space

- Deep fundamental research

- Concentrated portfolio

- Hedging

- Specialization is key

- How do we start our journey towards specialization

- Investments -> asset classes -> equities -> Europe

- A focus on publicly listed companies in Europe offers close to 10 k to analyze but 7% generate

- 0% economic impact

- Size and geography

- Small cap, ciro cap

- Market cap 100 to 350 mill

- Narrow and screen out 90% of companies

- Value premium – lottery preference, ugliness aversion, overconfidence/uncertainty

- Imperfect space to deep fundamental research

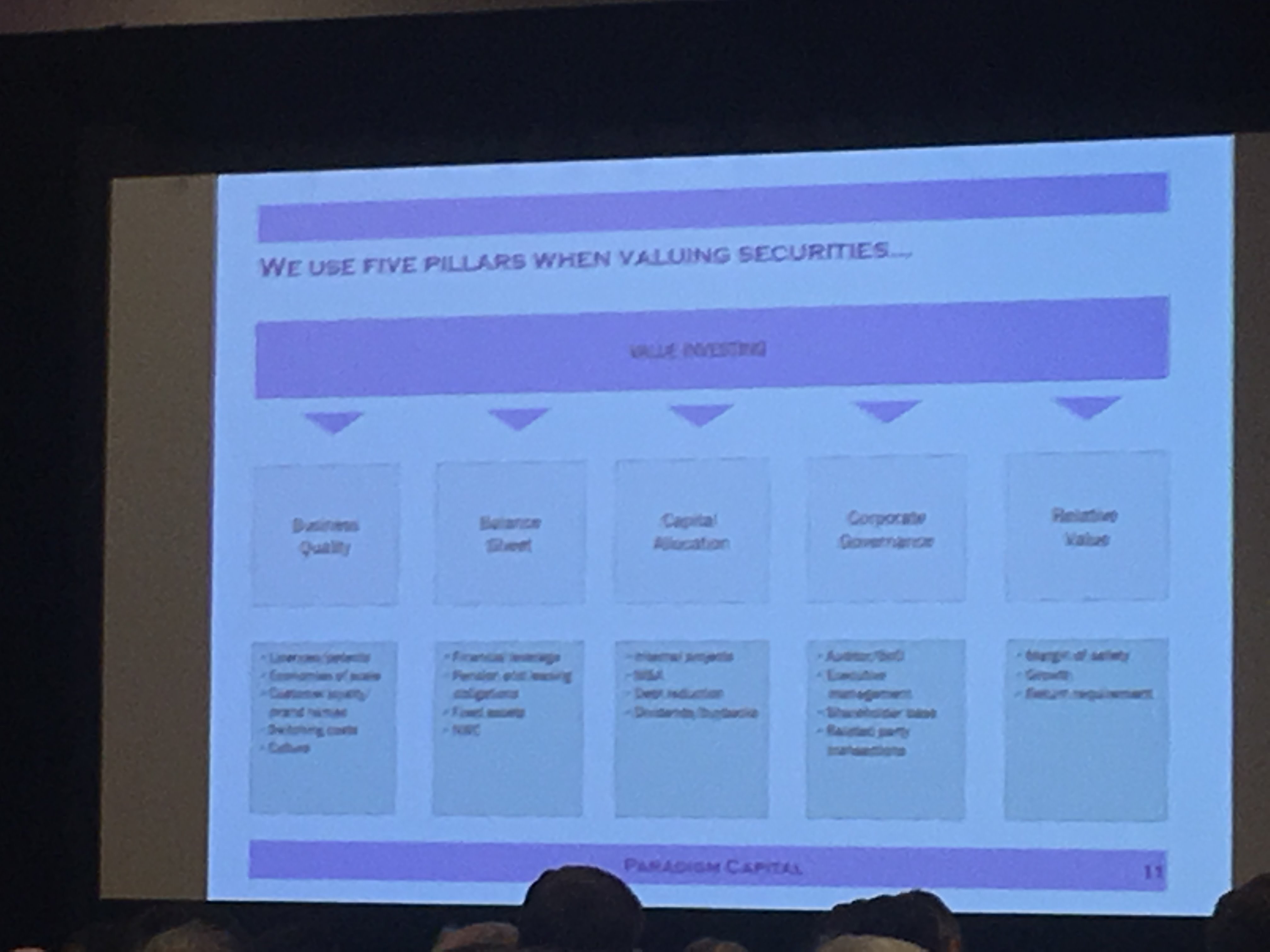

- 5 pillars business quality blance sheet capital allocation corporate governance relative value

- Value investing process

- NPV approach

- Ignore info

- Method of combining info

- Sensitivity analysis is based on difficult to forecast parameters

- Basic elemetns of value

- Strategic dimension

- Growth infranchise only ROCE > Cost of capital

- Franchise value current competitive advantage

- Free entry no competitive advantage

- Reliability deimension

- Asset value, tanglible,blance sheet based, no extrapolation

- Earneings power value, current

- Management -> cost efficiency, expansion of it only invested when expected return of capital employed is greater than cost of capital, when you invest in high cash flow and high return and how is distribution to capital to owners, management on human resource strategy (recruiting people when market and industry in difficult time, perfect time to pick the top people for your company)

- Understanding the concept of cost of capital and return on capital is an essential step in operating a business as well as being a good investor

- Value implications of barriers to entry

- Organic growth, cost reducing tech, new investments, growth option

- Efficiency

- 90% do not have or maintain a competitive advantage

- Risk management

- Not variance, but rather permanent impairment of capital

Q&A

- What are your thoughts on value investing is dead and impact of rising rates?

- Lily: strategies outperform over time

- Passive create dislocations in the market

- Shift towards active

- John Phelan: must evolve with times

- Utilize the new tools

- The survivors are the good ones

- Margin of error is much lower

- Adapt to the new efficiency

- When we think about growth, how would you invest in high multiple situation?

- Allan: growth and value are connected

David Sokol, Teton Capital

- Containership

- Major liner company

- Maersk, seaspan,

- Becoming like fedex

- What seaspan does

- Trucking on water, own the ships

- Liners are the customers

- Feeder, 1000 to 2700 boxes per ship

- Small markets

- Panama, post-panamax, new panama

- Charter rate what they charge Maersk, what is available to them

- Freight rates is what they charge their customers to move

- Freight forwarders use to help people move their stuff to port, now Maersk is doing this

- 62% value

- Alliances

- Don’t co-owon assets but rather co-utilize

- Top 8 now compose 80% of industry

- Few customers

- Engine efficiency, efficiency to ship itself

- Can the ship fit the panama canal

- Up to them to fill the ship up

- They run fuel and capacity risk

Stay tuned for more updates