Key Points

- Attractive investment opportunities can still be found in the real estate sector today, despite wide consensus that risks are rising as the U.S. economic expansion and commercial real estate cycle wear on.

- Opportunities include commercial real estate in high-growth markets in the U.S., special situations investing in select European and Asian markets, and distressed credits.

- In our view, investments in these areas can help a portfolio weather cyclical and localized risk in today’s late-cycle environment.

Q1 hedge fund letters, conference, scoops etc

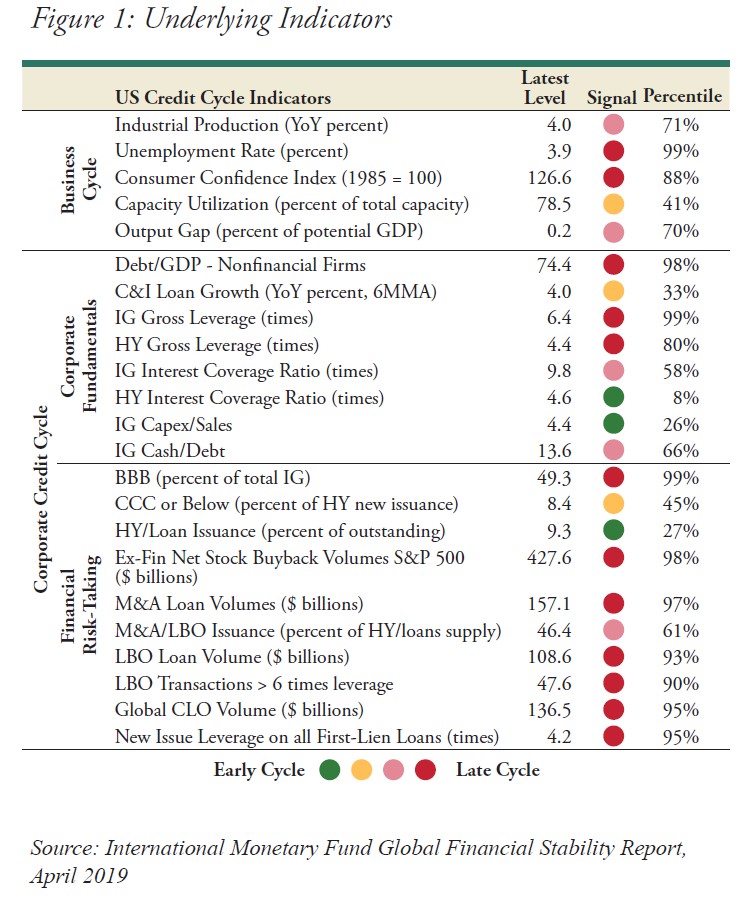

The United States is experiencing one of the longest economic recoveries on record. Steady GDP and jobs growth, coupled with moderate inflation and low interest rates, have characterized the U.S. economy for a full decade now. These positive economic developments have supported increases in real estate values that have far outpaced inflation and offered investors significant appreciation and income along the way. At the same time, no one knows how long this environment will continue. The economic cycle may be nearing the later stages of its up-leg, preparing for an inflection. The impact of a down-leg in the cycle could be especially significant in locations with excess real estate supply, difficult regulatory and tax environments, and limited access to affordable housing. Indicators that point to a maturing of the business and credit cycles include tight labor markets, increased risk taking and high levels of leverage across most credit-rating buckets (see Figure 1).

There is no particular catalyst in sight that appears likely to set off a downturn, and financial conditions remain relatively accommodative. But an air of uncertainty hangs over the markets; when a slowdown might start and what might prompt it are, of course, unknown.

Uncertainty warrants caution but does not rule out opportunity. Indeed, there are a few areas in real estate investing that we view as potential “winners” – that is, real estate investments that have room for upside and can weather cyclical and localized risks. We explore them in detail below.

Commercial Real Estate In High-Growth Markets

The United States has seen meaningful commercial real estate growth in areas once called “second-tier” cities, which are now fittingly known as “high-growth” cities. While the real estate industry defines markets in various ways and there are no strict rules regarding what constitutes a high-growth area, such markets are primarily characterized by high population and rent growth, diversified economic drivers, reasonable competition and differentiated capitalization rates.

This high-growth commercial real estate segment in the United States broadly covers the southeastern, southwestern and western regions. Key cities include Atlanta, Georgia; Denver, Colorado; Nashville, Tennessee; Phoenix, Arizona; and Tampa, Florida. We view these markets as experiencing a true transition into robust commercial real estate markets of their own, exhibiting strong fundamentals and greater growth potential relative to “gateway” markets such as Boston and New York, which tend to be “priced to perfection.”

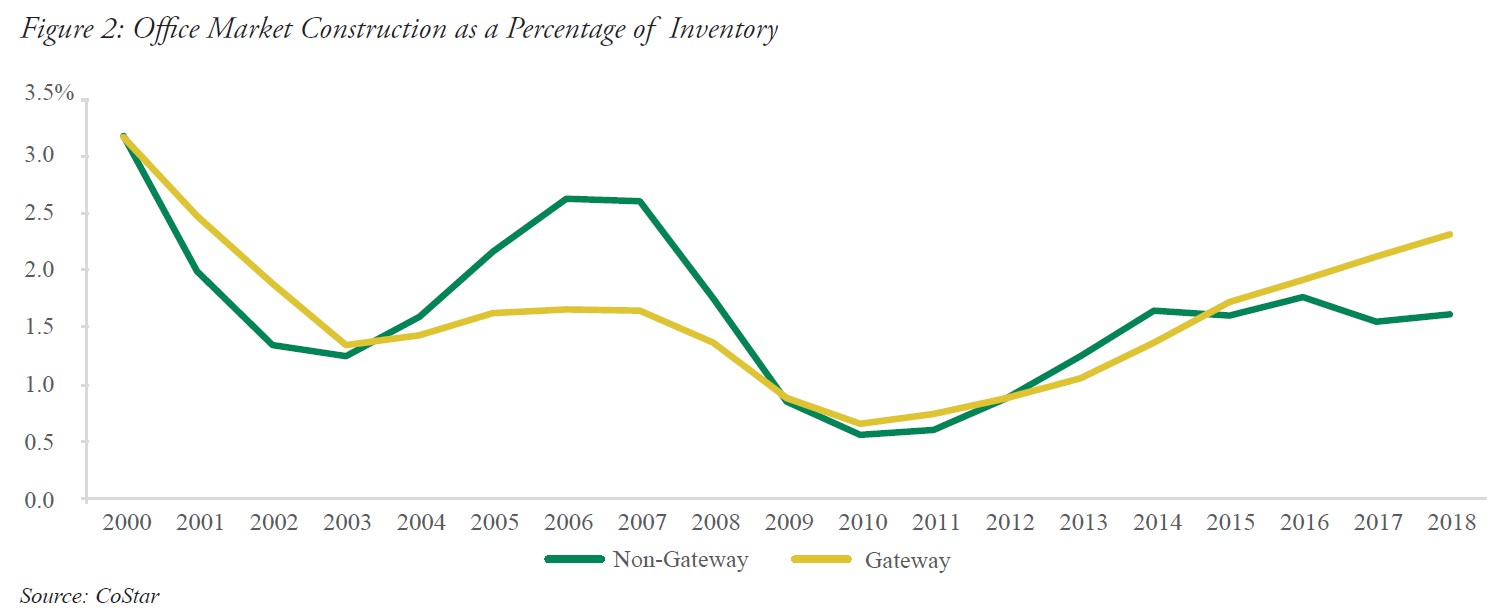

In particular, we find that high-growth markets offer favorable supply-demand characteristics relative to gateway markets, where supply risk is greater (see Figure 2). Further, the lack of aggressive overseas and “core” capital in high-growth markets has led to assets trading at cap rates above the national average, which allows investments to generate favorable annual cash yields. Fully leased assets in high-growth markets typically offer cap rates between 5-7%, versus the 2-4% range often found in gateway markets.

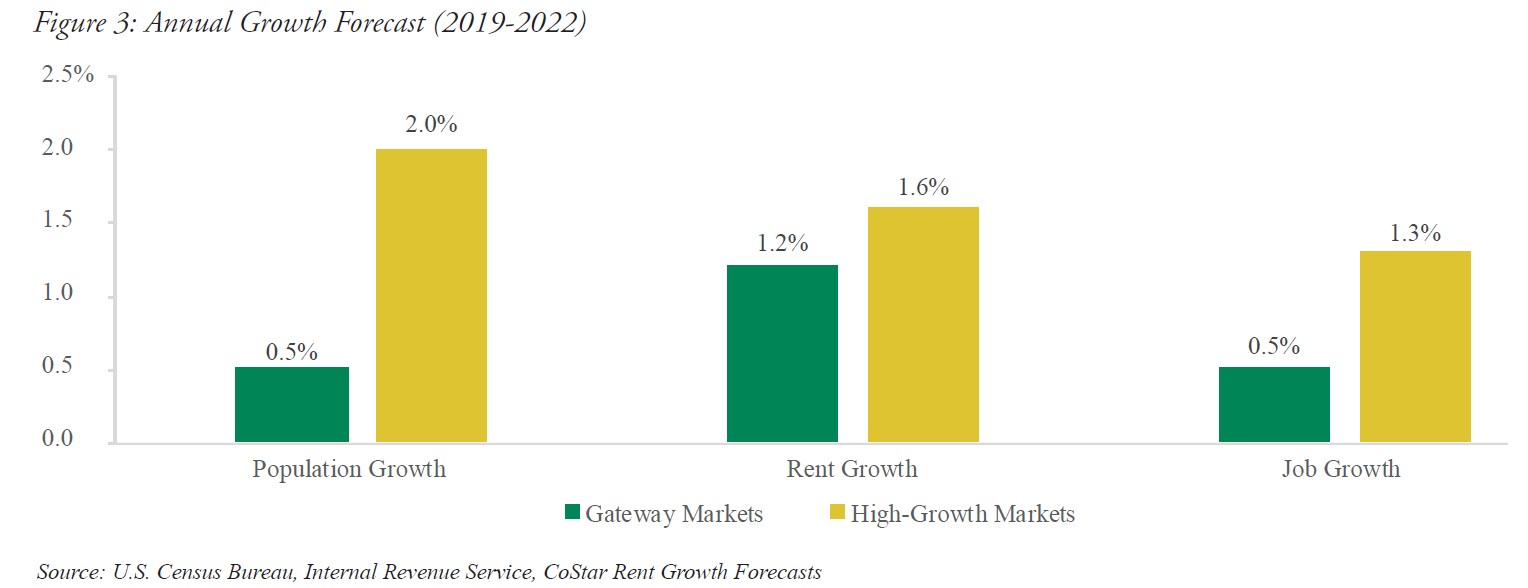

High-growth markets continue to experience population and rent growth and a job-base transformation (see Figure 3). Population gains are particularly strong within the millennial age group, the largest demographic generation in the United States. These markets offer a lower cost of living and higher quality of life owing largely to better tax and regulatory environments, technology and quality educational resources.

Notable migration of businesses into high-growth markets — many coming from gateway markets — and corresponding job gains have led to strong increases in rent, particularly for the office segment. Many of the reasons for company relocations are the same drivers of population growth. While the technology sector appears to be leading the pack in corporate moves, a diverse group of businesses in various industries such as finance, insurance, manufacturing, automobiles, logistics and healthcare have also either made moves to or expanded within high-growth markets.

Oaktree expects various regions in Europe and Asia to be sources of attractive buying opportunities, particularly in the form of “special situation” investments in select countries. Special situation investing involves elements of dislocation or instances of perceived undervaluation, and requires a highly bespoke approach to identifying, sourcing and executing on these opportunities.

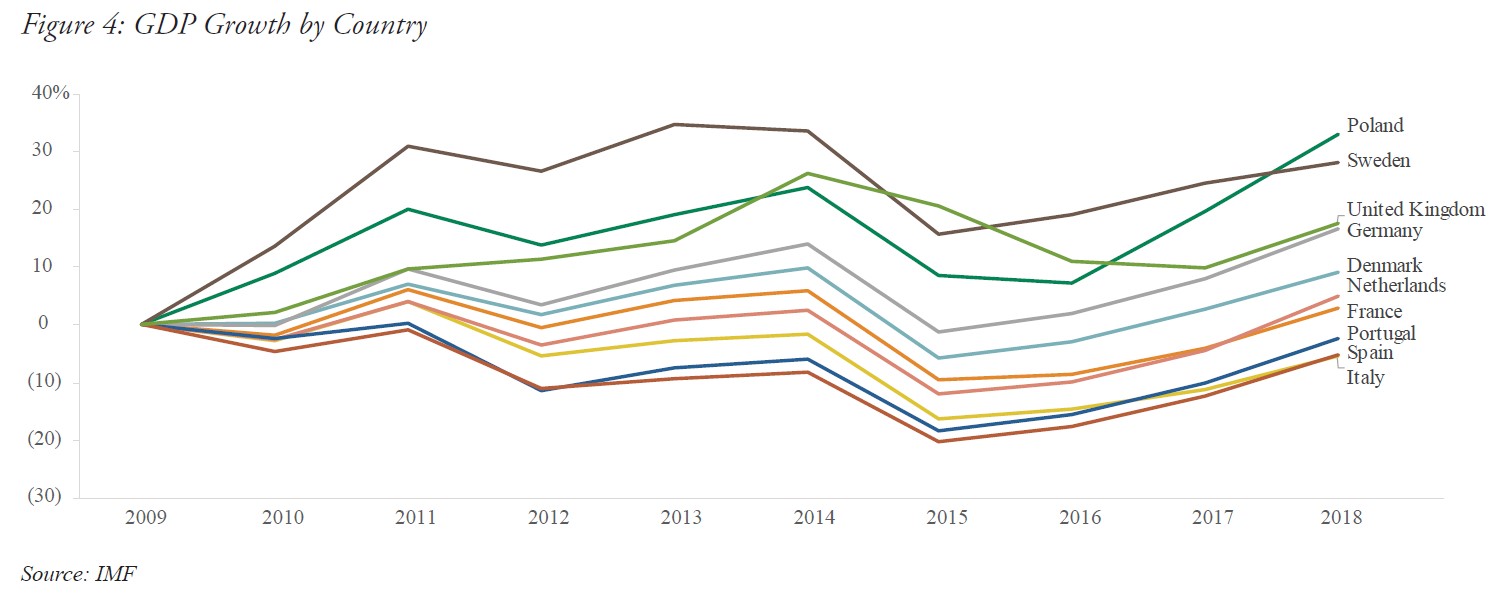

Economies in core European cities generally continue to exhibit growth, but broader political developments, such as Brexit, threaten stability, and the extent of growth is uneven among countries and metropolitan areas. There is also a geographical divide in the timing and pace of recovery since the Global Financial Crisis, with southern European nations (e.g., Spain) returning to growth later than their northern counterparts (see Figure 4). The southern markets are therefore earlier in the cycle and have experienced rapid growth in the last several years, with room for even more upside.

In addition, significant variation is present among the northern European nations. Certain submarkets have benefited disproportionately from infrastructure improvements and private-sector investment, particularly those that have an active presence of technology firms. Despite the many differences between these countries and markets, monetary policy in the EU remains centrally managed, which can magnify the economic strengths and challenges of each country. As the story of disparate growth continues, we expect attractive investment opportunities to arise in submarkets that stand to benefit the most from the European economic recovery and changing demographics across the continent.

In Asia, China, South Korea and Japan face challenges either specific to their regions or influenced by other,

international dynamics. The continuing trade-war threat may impose additional pressure on China’s economy, which has begun to show signs of cooling. South Korea’s administration continues to prioritize the resolution of tensions with North Korea and improvement in the economy; however, there are no “quick-fix” antidotes for either. The Japanese government’s re-inflationary policies have produced positive short-term benefits, including a strengthening real estate market in Tokyo, but the country still needs to deliver structural reforms to sustain long-term growth. Such environments create room for “situational” distress in local markets or assets.

Call Option On Volatility

In the fourth quarter of 2018 we were reminded — after a prolonged period of relative stability — of what an abrupt market correction can feel like. Anxiety over economic growth and continued uncertainty around trade negotiations, among other factors, resulted in the worst quarterly selloff for global stocks since 2011.

Various trends today indicate that the seeds are being sown for potential future distress. In a recent report the International Monetary Fund diagnosed “vulnerabilities in the sovereign, corporate, and nonbank financial sectors” as being “elevated by historical standards in several systemically important countries and regions that account for a significant share of the global economy.”

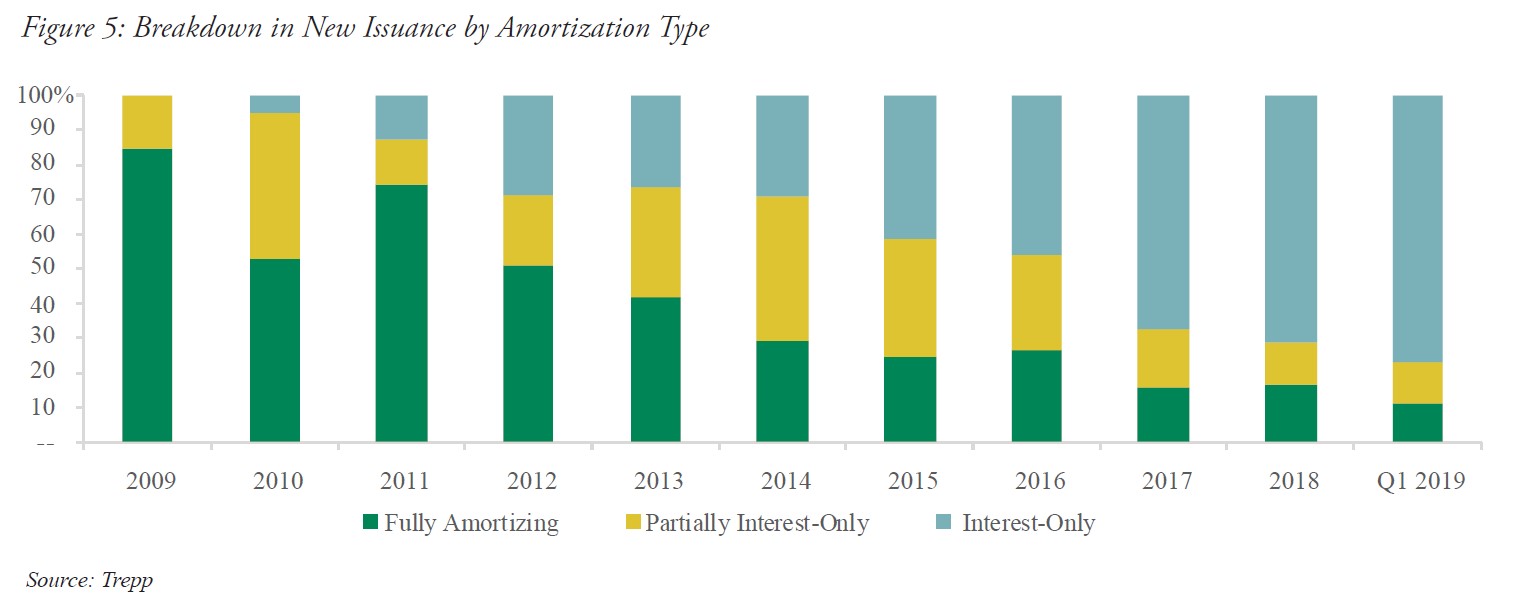

In U.S. real estate in particular, urban gateway markets have shown signs of weakening relative to high-growth markets when it comes to the office, residential and hospitality segments, particularly under the weight of potential oversupply. In addition, while overall issuance of commercial mortgage-backed securities (CMBS) is below pre-crisis levels, the makeup of those securities today is such that interest-only loans account for a much larger portion of the market, reaching levels last seen in 2007 (see Figure 5). Since interest-only loans do not amortize over time, this could further increase the risk that borrowers may have difficulty refinancing or selling their properties at loan maturity. Couple this with the reasonable assumption that cap rates could eventually increase if interest rates rise, and that could be a problem for owners that have utilized a significant amount of leverage.

Times of distress, however, can bring with them attractively priced opportunities for investment managers who can selectively source deals and deploy capital in stressed or distressed assets and credit. Such managers may be seen as having a call option on volatility that can be exercised at opportune times. Distressed investing opportunities may arise in such circumstances across the real estate industry, including commercial real estate, residential real estate, real estate-related debt, corporate securities and property-level debt. Structured products such as CMBS, as well as non-performing and defaulted bank loans, too, can be timely investments during a downturn. Even in the absence of a broad economic decline, particular real estate sectors may be adversely affected by oversupply, rising interest rates, heightened lending standards or general scarcity of credit.

A Long-term And Disciplined Approach

Real estate investors – much like any other investor – must strike a balance between the risk of losing money and the risk of missing opportunity. These “twin risks” – as Oaktree’s co-chairman Howard Marks calls them – are all the more pertinent today as we approach a possible inflection point in the maturing market cycle. The headwinds to investing in real estate today are plentiful; we see, among other things, increased competition, an unstable global trade environment and political concerns. Taken together, these warrant a defensive posture. However, Oaktree believes that skillful investors can continue to make attractive real estate investments throughout the economic cycle. Doing so requires a thoughtful approach, guided by risk control and selectivity to help navigate volatility and succeed no matter where the market winds may blow.

Article by John Brady and Bill Loskota – Oaktree Capital