Thanks to everyone who answered our survey from last week. Basically, everyone wants 3 things:

- Stock ideas & analysis

- Investing education and information

- Recommended readings

Q4 hedge fund letters, conference, scoops etc

So that’s what we’re going to give you. (Sure, we’ll sprinkle the odd tutorial or book review in, too.)

To kick things off, here’s an article about an attractive dividend play, Carnival Cruise Lines. Below that, you’ll find what we’ve been reading this week.

Thanks for helping make this newsletter a better place!

Mike

Cruise into 2019 with Carnival [Old School Value Blog – Dividend idea]

Guest article by Ranjit Thomas

Summary

Carnival Corporation (CCL) is a well-run cruise operator whose stock is trading at 11x forward earnings. The company is investing in expanding its business, while paying out a healthy dividend and buying back its shares. The stock has more than 20% upside to a $65 fair value, representing a reasonable 14x EPS. Enjoy a 4% dividend yield in the process.

Company background

Carnival is a global cruise operator that operates under the Carnival, Holland America, Princess, Seabourn, Costa, AIDA, P&O and Cunard brands. Each brand is differentiated to some extent by the size of its ships, staff to guest ratio, destinations, target audience and onboard amenities. The company is headquartered in Miami, Florida. It was founded in 1972 by Ted Arison, whose son Micky is currently the company’s Chairman.

The business is a straightforward one. The company buys ships, hires crew, and provides passengers an all-inclusive vacation to a destination, along with selling additional services to a captive audience. The financial reporting is uncomplicated. The company has a $36 billion market cap and $46 billion enterprise value. More than half of the company’s revenue comes from North American travelers.

The CEO for the last five years, Arnold Donald, has done a creditable job of operationally managing the company, investing in the business and returning cash to shareholders. Most crew members are from Asia and Eastern Europe and are non-unionized. As a result, wage increases for cruise lines are more muted, as compared to US airlines where labor is constantly angling for a bigger piece of the pie. The industry is also able to enjoy decreases in fuel prices when they occur, albeit to the extent they are not passed on to customers through competitive forces.

Financial results

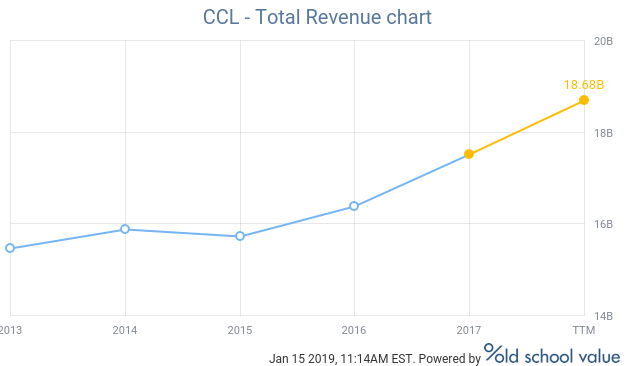

The company generated $19 billion of revenue for the year ended November 30, 2018. This represented healthy 8% growth over the prior year. Passenger ticket revenue amounted to 74% of the total, with most of the rest coming from onboard sales. Operating income was $3.3 billion, a 17.6% margin. Major costs include commissions, payroll, fuel, food and ship depreciation. Interest expense of $200 million is understated due to some interest being capitalized, while a 2% tax rate is low due to the way cruise companies structure their business by domiciling ships in low tax regions. Excluding a small amount of unrealized gains on fuel derivatives and a gain on a ship sale, the company had $3 billion of net income or $4.26 per share.

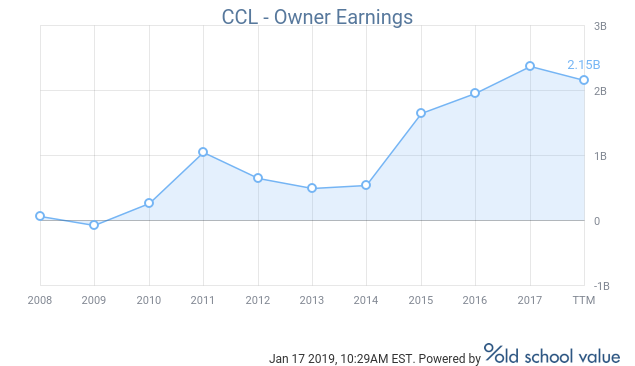

Along the way, CCL has improved its gross margins by about 10 points from the l0w-30s to the low-40s. It’s decreased its operating expenses, as well, resulting in improved EBIT and EBITDA margins. It has increased its CapEx to reinvest in the business and build capacity, but despite this, it has improved its Owner Earnings and Free Cash Flow along the way.

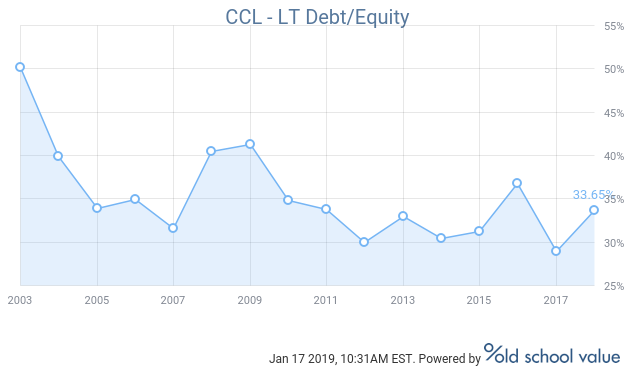

On the balance sheet side, the company has $10.3 billion of debt, well-supported by $35.3 billion of property and equipment. As cruise sales are made well in advance of actual sailings, the company held $4.3 billion of customer deposits that will be converted into revenue in the future.

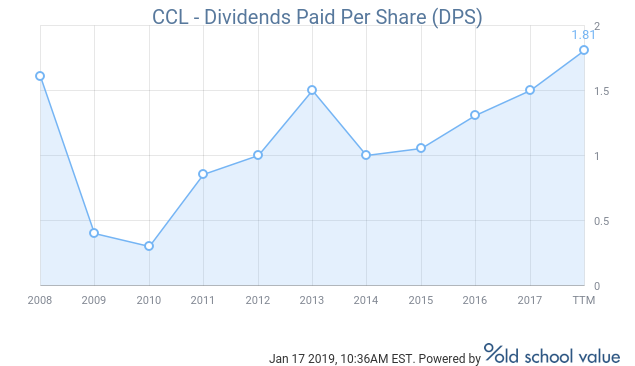

A look at the cash flow statement reveals the weak spot of the cruise industry. The company generated $5.5 billion of cash from operations, but spent a whopping $3.7 billion on capital expenditures (compared to $2 billion of depreciation). Thus, it generated only $1.8 billion of free cash flow, compared to $3 billion of net income. Effectively, it is re-investing 40% of its net income to grow the business. The company paid out $1.4 billion in dividends and bought back more than $1 billion of its shares, adding a modest amount of debt to its balance sheet.

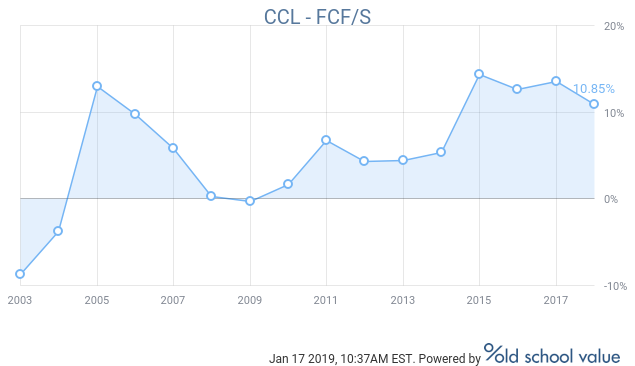

Despite the significant CapEx investments, CCL’s FCF to Sales is about as good as it’s been:

What we’re reading

A review of Seth Klarman’s warnings about the current state of the markets from his annual letter. [marketfolly]

Peter Lynch: 13 Filters for Finding the Perfect Stock. [Acquirer’s Multiple]

Netflix is so confident in its position it is effectively stating that if customers choose to watch TV, they will choose Netflix. [Stratechery]

The rationale, philosophy, and process of investing for the long-term. [Behavioral Value Investor]

Don’t think of your investment time horizon, but consider how sensitive you are to new information. [Morgan Housel]

We are not as good at selling stock as buying them. [Barry Ritzholtz]

The desire to just hold conflicts with a recognition that volatility creates opportunity. [Greenhaven investor letter, PDF]

The historical valuation premium [between US and Foreign stocks] has been ZERO. [Meb Faber]

Efficiency is great in an unchanging environment, but to expect an environment to remain static is unrealistic. [Farnam Street]

Algos & others aren’t causing market moves to happen faster than in the past. [Ben Carlson]

The art of decision-making. [The New Yorker]

Quick hit

Monthly Membership is Back!

As requested, it is back. If you are not an Old School Value members and have been hesitant about joining because of the upfront payment, it’s now easier than ever.

We brought back our monthly subscription plan about a month ago. Now you don’t have to commit to a full year or more when signing up.

We also added a 7-day trial for just $7, so your risk is even lower. You can cancel anytime during the trial and you won’t be charged again. Pretty sweet, eh?

Check it out and let us know what you think.

About Old School Value

Leverage your limited time to succeed in the stock market.

Stock grading, value screeners, and valuation tools for the busy investor.

Check out the live preview of AMZN, MSFT, BAC, AAPL and FB.

Article by Jae Jun, Old School Value