“If something cannot go on forever, it will stop.” – Herb Stein, Senior Fellow of the American Enterprise Institute

Q1 2021 hedge fund letters, conferences and more

Over the last several On My Radar posts, I’ve shared my notes from the 2021 Mauldin Strategic Investment Conference (SIC). We’ll continue this week with my high-level summary notes (and select comments) from Danielle DiMartino Booth’s interview with William White.

Why William White Matters

Bill White headed the Bank for International Settlements (BIS). Think of the BIS as the central banker’s central bank. He spent most of his career at the center of the table. He knows all of the players and has an exceptional grasp of global economic dynamics and their political impact. From monetary policy from the Fed to fiscal policy from legislators, Bill explains complex dynamics in a way that most people can understand. Most economists can’t do that.

We find ourselves at an important inflection point. Zero-bound interest rates and inflation are clearly in play now. Bill sees inflation in the near term, deflation in the medium term, and inflation in the long term. Inflation and higher interest rates represent an investment regime few have experienced. My hope is that by listening to what Bill has to say, you gain a better understanding of the dynamics at the Fed and the complexity they face given where we sit in the cycle (euphoria, ultra-high equity market valuations, and ultra-low interest rates).

Tickets in a Fish Bowl

The investor’s goal is to make money, period. The best explanation on investing I’ve ever heard came from famed investor Howard Marks. Presenting at the 2019 SIC, Marks said we should think about investing as “tickets in a fish bowl.” Here’s his quote:

There is no sure thing [in investing]; there’s a bowl full of tickets and the tickets are all the future possible outcomes and fate or something. Some people say that it’s very determinable because it’s logical and mechanical, and other people think it’s completely random, but fate or something is going to reach in the bowl and pull out one ticket.

Now that ticket may be the performance of GDP next year, the performance of the company’s earnings, or the performance of the stock market or a given stock. They are going to pull out one ticket, one outcome, which becomes the actual outcome from the many outcomes and nobody should think that there is only one ticket in the bowl, you know. The point is, there really are no sure things in life.

Now if all performance, if all the future, is one ticket drawn from a bowl full of tickets, does that mean we can’t know anything about the future as investors? The answer is no, it doesn’t mean that because sometimes there are more winning tickets in the bowl than losing tickets, sometimes they’re more losing tickets in the bowl than winners, and an exceptional investor is someone who has an above average awareness of the tickets in the bowl––even if he doesn’t know what the outcome is going to be.

But the great investors that I know, know when they have a bowl full of winning tickets and not losers. You have one stock and you know that if there’s a 90% chance it will go up but a 10% chance it will go down and if it goes up, it could go up five times, but if goes down, it could go down 30%. That’s a great investment opportunity.

You still don’t know what the future holds, but that is highly investable and you should invest more. You should invest more when the tickets in the bowl are in your favor. You should invest less when they are against your favor and what determines the mix of the tickets in the bowl is largely where we stand in the cycle.

It’s common sense: “You should invest more when the tickets in the bowl are in your favor. You should invest less when they are against your favor.”

Keep this concept in the back of your mind as you dive into today’s William White notes. Since the Fed sets the cost of money (the most important factor in investing), “don’t fight the Fed” accounts for more than a few of tickets in the fish bowl. Inflation will cause them to pivot.

Danielle DiMartino Booth’s interviews of both William White and Richard Fisher stole the show. Get ready for a crystal-clear window into what’s going on at the Fed. This week, William White; next week, Richard Fisher. Focus in on White’s discussion on interest rates. I could be wrong, but I think he is right on the money. Let’s go…

Grab that coffee and find your favorite chair.

This week’s On My Radar:

- William White

- Trade Signals – Model Favors Value Over Growth

- Personal Section – A Hat Tip to Mentors

William White

First, some background on why you should listen to what Bill has to say:

From Wikipedia:

William R. White (born 1943) is a Canadian economist who was the chairman of the Economic and Development Review Committee at the Organization for Economic Co-operation and Development (OECD) from 2009 to 2018.

In 1994, he joined the Bank for International Settlements (BIS), the Swiss-based “bank of central banks,” as manager in the Monetary and Economic Department. From May 1995 to June 2008, he served as its Economic Adviser and Head of the Monetary and Economic Department. He retired from the BIS on 30 June 2008.

He is famous for flagging the wild behavior in the debt markets before the global storm hit in 2008 (Great Recession).

Let me begin with the conclusion and then explain how he arrived there: As I mentioned, Bill believes in the near term (six to eighteen months), we will have inflation; in the medium term, we will have deflation (debt and demographic dynamics help deflation regain its foothold); and in the long term, we will have inflation. Like Stan Druckenmiller and Felix Zulauf (see last week’s OMR), the global central banks will, in the end, monetize the debts.

I think Bill does a better job than most everyone else in explaining how important it is to connect the dots between all the players in the system: governments, central banks, monetary/fiscal, interest rates, and currency movements (as in the end capital flows to where it is treated best). I also appreciated his comments around how we need to teach economics so that people understand the adaptive nature of complex systems.

Let’s dive in: Danielle DiMartino Booth interviewed Bill and began with a quote from Herb Stein, senior fellow of the American Enterprise Institute, which Bill included in one of his recent letters: “If something cannot go on forever, it will stop.” She asked Bill what that means.

Bill: Well, I think the phrase became famous because it’s so obvious, if something can’t go on forever, it will stop, it is not sustainable.

- But the reality is that the way we tend to think about things, sort of monetary policy, whatever, is that the future will be like the past. And I think what the difficulty is at the moment is that there’s many, many systems that we currently have in operation that are starting to show a real sign of stress and signs that potentially they will stop.

- Our economic system is in a mess.

- Our political systems and many of the democratic countries are under threat.

- The environmental and climate problems are clearly pressing. And now in addition, we’ve got the pandemic and do think that most of these system failures do need to be urgently addressed. And I don’t think the governments really understand the extent to which quick action is absolutely necessary.

And of course, the problem with all of these systems is that they’re all nested systems. Your economic system has influence on your political system; the environmental system has influence on every other system.

- When you start thinking in terms of solutions, you have to start thinking not just about a solution that’s good for the particular system that you’re addressing, but what will be the side effects on the other systems? We have some really difficult issues ahead of us, difficult in the sense of What is it that we should do? and difficult in the sense of, Do we have the powers to do it?

A good example would be, you’ve got global problems, but there’s not really a global government. And then lastly, you’ve got what I call the wooden problem, which is the will to act.

- Even if you know what you should do, and you could do it, will you do it—for example, without general support from the population who doesn’t really understand the character of the problem?

- There’s a lot of challenges out there and it’s all wrapped up in that, what is it?

Danielle asked Bill to walk us through why there has been so much denial of the close relationship between inequality and economics.

Bill quoted H.L. Mencken: “There is always an easy solution to every human problem—neat plausible and wrong.” Then added:

- I don’t want to be sort of conspiratorial, but if you go back to the simplest kinds of economic models, what they will tell you is that everybody gets paid their marginal product as it were, what you produce is what you get paid. And that’s very simple and it’s a very nice, (but simple is not so simple – Mencken’s quote).

- But the question of justice having to do with inequality, the question of power having to do with inequality, those questions just simply disappear. They go off the table. It suits a lot of people not to talk about the inequality problem. And the inequality problem, the more you think about it, again, it’s sort of part of the systemic system stuff.

- The tentacles go everywhere. If you’ve got inequality, one problem that Raghu Rajan pointed out, not the first, but he did it very eloquently in Fault Lines is that if you’ve got inequality, some people have got lots of money to spend and they spend it and the others don’t have the money, but they have the desire to spend it, to keep up with the Joneses and in trying to do so, they have to borrow the money, add interest, which frequently becomes cumulative. And so the inequality increases.

- And when you try to resolve these problems through macro-economic stimulus, let’s say, and easier monetary policy. One of the problems is it just facilitates people borrowing more money to keep up with the Joneses and they get still further in debt. There’s a kind of vicious circle involved here.

Bill: The second element of it, as I see it, is of the political element. I do think that growing inequality does wind up having a political manifestation. We see it in the UK, we see it in the US, we see it in other places in Europe.

- People who know they’re falling behind and maybe above all people who increasingly sense that their children don’t have equality of opportunity. It’s not just them, it’s their kids. This really makes people feel badly.

- And we all know that there’s a strong element in human nature. When things go wrong, somebody must be blamed.

- And that I think winds up with a kind of political polarization, which you’re seeing in spades, of course, in the US and to a lesser degree in the UK.

- And I think longer term, it’s just a real threat to the democratic process.

Bill: If you have an element of distrust because of the inequality and feeling that somehow you’re not part of the favored few, the absence of trust means that you’re not going to believe people when they tell you that you must do something for your own good. And I’m thinking particularly about the pandemic, about vaccine take-up, I’m thinking about environmental…

- These things are not easy solves and if you don’t have the trust between the various groups in society, and most importantly, the government and the people to say nothing of the journalists and everything else, then you don’t get the buy-in to do the difficult things that need to be done to deal with all the systemic problems that I started off talking about.

[SB here: read that last bullet point again… We have complex problems to solve. Will we get the buy in to make the difficult choices? We don’t yet know. What we get will add or subtract tickets from the fish bowl. Therefore, we must be prepared to adapt.]

Danielle: There’s a role that’s been played especially in a post pandemic world between the fiscal authorities and the federal reserve in the United States. One thing that confounds me more than anything else––possibly infuriates me more than anything else––it’s the fact that nobody at the Fed will own up to the fact that monetary policy pours fuel on the fires of inequality. You (Bill) have run inside the inner sanctum, why is there this level of blanket deniability among central bankers that they’re in no way responsible for what’s happened?

Bill:

- I think to be honest, Danielle, I think there is a growing recognition on the part of the central bankers. There is an increasing sort of number of conferences and papers that are being written on this.

- But of course, in a sense it’s far too late. Progress is being made. Progress is definitely being made on that front.

- But it seems to me there is a growing unwillingness to see the political implications of this inequality. You get a kind of a grudging admission that whereas income inequality might be lessened by easy money, there’s less of a recognition that wealth inequality is clearly increased by easy money

- Of course, the whole game plan, if you raise the price of financial assets which are mostly by definition owned by richer people and the increase in the wealth associated with those higher priced financial assets, then trickles down. That’s basically the story that people would tell.

- However, the unwillingness of authorities to see the unintended consequences, including the impact on distribution and equality and inclusiveness, that’s something that that’s troubled me personally. And I think has troubled the BIS (Bank of International Settlements) for a long period of time.

Danielle: Where do you feel we are in the pricing cycle? Do you see the same risk that so many do today that after a 40-plus year run of declining interest rates, declining inflation on a trend, do you feel that we are coming to an inflection point when it comes to inflation and deflation?

Bill:

I’ve been following this SIC conference pretty closely, and a lot of people that I respect a lot, and what is astonishing is on one hand, David Rosenberg, Lacy Hunt, Barry Habib all saying that inflation won’t become entrenched. And then you’ve got Jerry Dillon, Jim Bianco, Peter Boockvar are all saying, oh yes, it will. Who do you to believe?

- For a starter, I guess I would say that the inflation process, like all of the processes that occur in a modern economy are extremely hard to predict. One of the things that I’ve been on about for ages is that the necessity to see the economy is a complex adaptive system.

- What I would say is that the economists have made a fundamental ontological error. They have missed specified the character or the nature of the system that they’re dealing with. (Emphasis mine.)

Bill: All of the models, et cetera, are all very simple. And indeed, the models that are used most in the last 15, 20 years are about as simple as you can get with rational expectations and market clearing, and everything goes back to equilibrium.

- If, rather, you believe that the economy is a complex adaptive system––like virtually every other system in nature and society––then you can’t come to the conclusion that things are easily understood and easily controlled and inflation is one of them.

- As I look at it at the moment, I think with complex adaptive systems, you almost get thrown back to saying it’s impossible to predict the future. And I won’t go that far because I think you have to give it a bash, but it’s not easy.

- At the moment it’s pretty clear from looking at the numbers that inflation rates are taking off. I mean, not just in the US, but globally. We saw just the other day, Chinese producer prices are up 6.8% year over year. You saw the last thingy in the US on the CPI, commodity prices, house prices.

- No matter where you look, that’s where we are at, that’s what’s happening.

Bill: Short-term I think inflation is going to be rising, but then medium term, and I’ll get to the stinger and the tail in a moment. Medium term, I’m more in agreement with the people that say, this is not going to last. And I think the big reason for that is what I referred to before as the unintended consequences of ultra-easing monetary policy. Even before the pandemic hit, the patient had preconditions or morbidities. It was an accident waiting to happen. And the pandemic happened to be the trigger.

- Well, even if the influence of that goes away, those morbidities are still there. And indeed, given that one of the morbidities has been this constant accumulation of global debt over the course of the last 20 or 30 years, that debt problem, both public and private is now much greater now than it was at the beginning of the pandemic and far worse than it was when the crisis started.

- It’s not commonly realized when the great financial crisis started. I think the IIF numbers for debt to global GDP were 280% at the beginning of the crisis, when the pandemic hit, they were already at 320%.

- They were up 40 percentage points in large part in emerging markets. People who say, well, the downturn is the time for deleveraging. Think again, Bob, it’s gone in exactly the opposite direction and the pandemic of course has made it much, much worse.

Bill: I think some combination of the debt overhang the precautionary motive that will come out of both that and the pandemic. The likelihood that there will be other problems that will materialize that have their roots in easy money like:

- squeezed margins for financial institutions,

- more reaching for yield,

- more market excesses,

- more imbalances of various sorts…

Bill: Medium term, I think the story is one of very slow growth and deflation. In the longer term, I guess what I’d say is that governments can’t stand by idle.

- People won’t allow them to stand by idle.

- Something must be done! And that’s the kind of mentality we likely get.

Bill: Longer term, if the stagnation continues, I suspect what will happen is the governments will throw everything they can at it.

- Which is, they will double down on both fiscal and monetary. And this is where the problem arises.

- And we’ve seen this many times in history and we’ve got good theory to try to explain it, what happened is that in that kind of an environment where you’ve got big government deficit and a very large government debt and growing recourse to the central bank,

- As the only group of people still left that will lend money to this government. At a certain point, the fear of fiscal dominance creeps in, and the minute the fear of fiscal dominance comes in, the central bank(s) will do anything to keep their government(s) afloat.

Go back and read Reinhart and Rogoff. We’ve seen this so many times before. I’ve got a short-term story, a medium-term story and a long-term story. And my next question is how long is a piece of string?

- You get the point is we don’t have clear definitions of what these things mean, and it is not impossible. To be honest, it is not impossible in a complex adaptive world for people to go directly from the short term to the long term. That is not impossible.

- And in fact, these systems, I mean, I’m not saying I’m a huge student, but one thing about these complex adaptive systems is they have phase shifts so that everything can be just perfectly fine and then something changes that just pushes it over the edge. And the whole world is different.

Bill: Once the inflationary process gets started, you could see changes in behavior. The underlying problem with the overhang of debt and the slowdown of growth is because people slow spending and save more to pay down their debts. It’s the paradox of thrift.

- But you can go directly to a world where people are basically saying, there’s no way that I can do that. The best thing to do is to gamble for resurrection.

- They see the bad things coming down the road, and (say to themselves) I’m going to protect myself from that inflation and in trying to protect themselves from that, they actually create the problem that they’re trying to avoid.

- In these kinds of systems, it’s entirely possible.

And another aspect of it, I was just thinking about this, well yesterday in the context of one of the presentations, is everybody said, What happens if inflation goes up, for a reasonable period of time, six months, nine months, whatever? The Fed has nailed its flag to the mast that this is not going to happen. This is temporary. Whatever temporary means.

- What happens if there’s a growing sense that they got it wrong and that we’re seeing that they got it wrong?

- In that case, you have a reputational hit of no small magnitude, which basically says to everybody, all things are possible.

- And then the anchor is gone, the credibility is gone, and then anything can happen.

Bill concluded: I’m still sticking to my story. Short run, medium run, possibly long run. But you could move from the first to the third in the twinkling of an eye. I’m not saying it’s probable; I’m saying it is possible.

There was a great question from the audience. Bradley asked, “In the long term, where do you go?” Meaning, where to you put your money with so many countries doing the same thing, all printing money. This is kind of a de facto currency war that we’re in right now.

Bill answered:

“Bradley, that is exactly the question that I actually have been thinking about myself and for which I will say I have no clear answer. Certainly, there’s no historical precedent for this stuff. I am of the view that we have in fact been in a kind of currency war for quite a long period of time. When the US started easing money in 2009, and then into 2010, and the dollar went down, and everybody else’s currency went up and a lot of the other people said they didn’t want their currency to go up. And so they started using monetary policy too.

- When I look at Europe, for example, and I see the extraordinary things that the Europeans have done in terms of easing over the course of recent years, all on the basis of inflation coming in at 1.4 as opposed to 1.8, which is 2% or just a little below, I just find it hard to believe that that discrepancy was the only thing that could explain their behavior.

- To me, I think currency considerations always sort of figure in and that leads us to a situation where all of the big central banks as is implicit in your question now have vastly expanded balance sheets.

- And I do worry about that, that we don’t just have one country in trouble from what you can flee, but we have all sorts of countries potentially in trouble from which you can’t flee.

But that also brings me back. And I’m thinking on my feet here, that brings me back to the question we were just talking about inflation about going from the short run to the long run, sort of in one fell swoop. The classical way for people to get out of a currency where the government is spending and the central bank is printing it, and the credibility is gone, the classic way is a currency run.

- And you’re absolutely right to raise the question, Where do you run to, if everybody is doing it?

- Where do you go if everybody is doing it? Well, maybe what you do at that point is you go directly from, what I was talking about before, you go directly, not from one currency to another currency, which you might actually do in the face of rising inflation of one country and not another, you go directly from the money you’ve got to the real asset that will protect you.

- And so what you see is commodity prices go up, house prices go up, equity prices go up, et cetera. And that if you wanted to interpret it that way, you might say, the funny thing is, that’s what we’re actually already seeing.

- I’m not saying that what you’re seeing is a shift to the long run solution here, which is much higher inflation, but it is not inconsistent with it.

[SB here: There was more to the interview but I believe I addressed the high points—at least as I see them.]

This is one of the best discussions I’ve come across as it relates to how we should think of economics as a complex and adaptive system. Please share it with your children.

Back to Tickets in a Fish Bowl

Here’s how I see it:

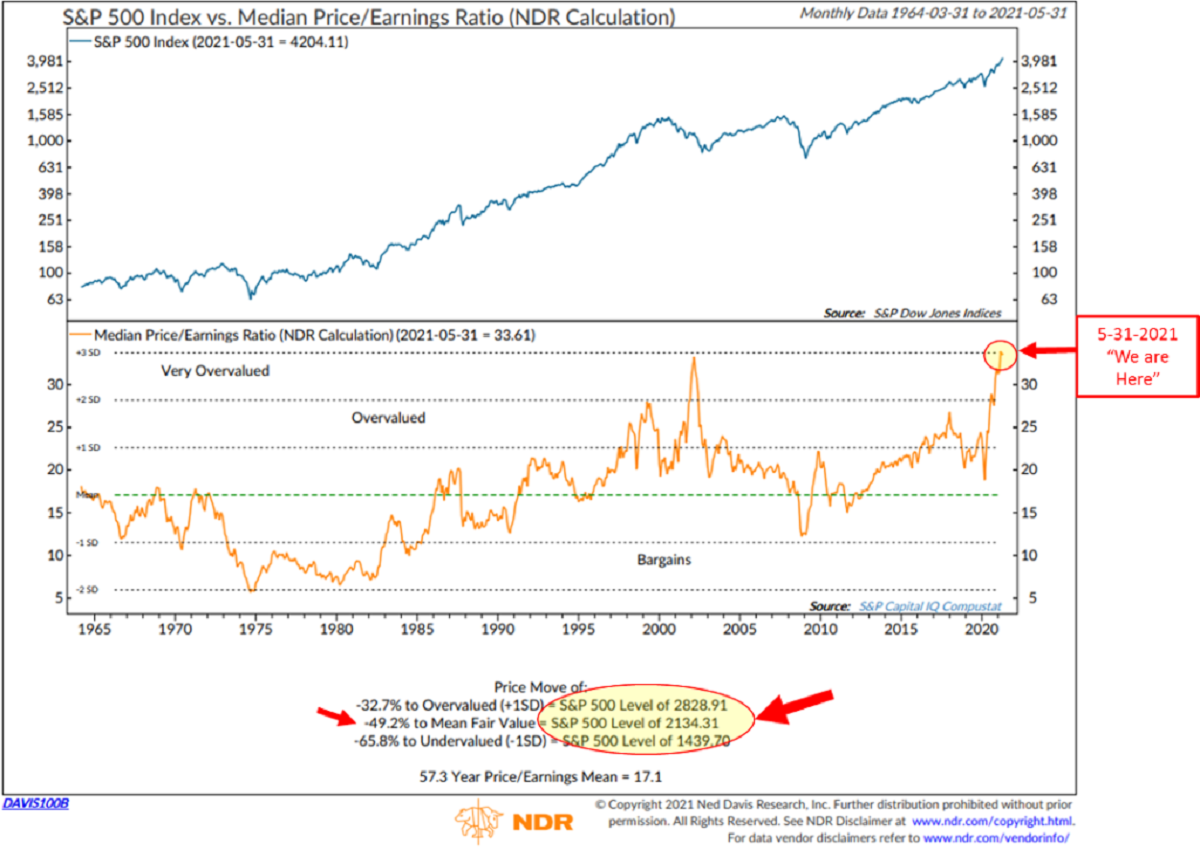

- Markets are richly priced and, by many important measures, at the most overvalued level in history. That tells us that the coming 10-year returns for basic cap-weighted index funds are approximately 0% to -3% per year.

- John Hussman says a market decline of -66% gets us back to fair value. This next chart from NDR—one of my favorite valuation measures—says -49.2% gets us to fair value.

- It’s important to note just how overvalued the market was at the end of May 2021. A decline of -32.7% gets us back to overvalued. I suspect that may be a very good entry point (note: it will come in a state of panic so be prepared).

Further:

- If the fish bowl is loaded with inflation tickets, positioning to a 1.60%-yielding 10-year Treasury may not be a good thing in a probable rising inflation and rising rate environment. A 2.10%-yielding corporate bond fund won’t help either. Too much risk vs. reward.

- Instead of using traditional bonds as part of your CORE (e.g., protect principal) portion of your portfolio, think about trading bonds instead and put that risk in your EXPLORE bucket.

- If you would like a copy of the interview I did at the end of the Mauldin Conference, simply reply to this email and I’ll send you a link. I talk ideas/solutions. (Available for current clients and prospective clients.)

Game Plan: It’s Time to Play a Different Game

- I had an article published in Forbes today. Bonds Are a Broken Asset Class – It’s Time to Play a Different Game – you can find it here.

- In it I share a few ideas. Not everything is overpriced and there remains opportunity. Just not in traditional 60/40 buy and hold. When the system resets, adapt. Then 60/40 will make sense again.

We’ll look at Richard Fisher and close my OMR conference note series next week. You’ll find links to past notes in the personal section below. And if you did not sign up for the conference and would like access to all of the presentations, including Mp3 downloads, transcripts, and slides, you can learn more here (please note, I am not compensated in any way—just a big fan of my partner and friend John Mauldin and his business partners at Mauldin Economics):

One of the SIC’s nicest features is the way people with vastly different viewpoints engage civilly and thoughtfully. Unlike “debates” that generate more heat than light, we sincerely look for the best answers—a refreshing rarity in this divisive era. Another reason you should get your pass and watch/read/listen to every session.

In the Personal Section below, you’ll find more links to the conference. Mauldin shared his thoughts and I provide a link to a select few past OMR letters.

Trade Signals – Model Favors Value Over Growth

June 2, 2021

Posted each Wednesday, Trade Signals looks at several of my favorite equity market, investor sentiment, fixed income, economic, recession, and gold market indicators.

For new readers – Trade Signals is organized into three sections:

- Market Commentary

- Trade Signals — Dashboard of Indicators

- Charts with Explanations

Market Commentary

Notable this week:

Mostly green on the signal board.

This week I thought I’d focus in on the Value vs. Growth story. I fundamentally believe we are in a period most similar to the tech bubble in 1999 (investors over-concentrated into the same names). If you remember, over the subsequent 10-years the S&P 500 Index lost 1.50% (approx.) per year. However, value did well. No one wanted to invest in value stocks in the late 1990’s. Like then, we may be nearing another inflection point. Take a look at the following chart.

- The middle section plots a relative strength ratio comparing the S&P 500-Citigroup Growth Index to the Citigroup Value Index.

- When the line is rising, growth is outperforming value. When falling, value is outperforming growth. Note the longer-term uptrends and downtrends.

- The bottom section shows two dotted light blue lines. When the model is between the two brackets, the model is considered neutral (i.e., no clear tendency for outperformance by either market). When the model is below the bottom dotted blue line “Favor Value” and when the model is above the upper dotted blue line “Favor Growth.”

- The data box in the top left corner shows the annualized performance based on the signal. Gray shading indicates the current signal. This is a long-term model and tends to produce approximately one trade per year to one trade every few years.

Trade Signals – Dashboard of Indicators follows next. Green continues to dominate the dashboard. Click HERE to go to the balance of Wednesday’s Trade Signals post.

Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note – A Hat Tip to Mentors

Years ago, Stephen Mittel gave me a shot. I was the first intern at his firm, Montgomery Securities, in San Francisco. I spent two weeks on the floor of the New York Stock Exchange, four weeks in San Francisco, and two days on the floor of the Chicago Mercantile Exchange. I was an accounting and finance major at Penn State and he opened my eyes to the markets and mentored me over the years until his passing eight years ago.

My assistant would shout to me, “It’s President Regan on the phone.” It wasn’t; it was Mittel. Another time, it was Coach Lou Holtz, and another it was Coach Paterno. It was always a head fake for my team, but for me it was time to drop whatever I was doing, pick up the phone, listen, and learn.

Years ago, I started an internship program at my firm. It’s named after Mittel and the goal is to do for others what he did for me: open someone’s eyes to what the real world looks like. Our first intern is now CMG’s president. How about that. To prepare this summer’s intern, young Zach, I sent him a short email with some links for him to review before he started.

The first one I shared was the video interview with William White. My thinking is he will have teachers that may present a different view, and he should begin with a base understanding of how the system works through the eyes of an experienced, balanced, and humble leader.

Here are some of the additional links I promised. They summarize what has been discussed at the SIC2021 (they’ll also be added to the internship must-read list):

- Put today’s On My Radar William White discussion at the top of the list. Best to first understand the adaptive nature of complex systems – A simple discussion that goes beyond Econ101.

- Deflation Talk, by John Mauldin – Thoughts from the Frontline May 28, 2021

- Expecting Inflation, by John Mauldin – Thoughts from the Frontline May 21, 2021

- Cold War or Not – China Panel, by John Mauldin May 14, 2021

- On My Radar: Stan Druckenmiller at His Best

- On My Radar: SIC2021 – Deflation? Inflation? Transitory? Define It?

More to come…

Seeing ideas stress-tested on stage by peers, to me at least, is invaluable in terms of better understanding current probabilities or “tickets in a fish bowl.” It’s what makes Mauldin’s conferences unique.

Lastly, on the final day of the conference I was interviewed by Mauldin Economics’ Ed D’Agostino. It was a “how does an investor take in all that was shared over two weeks and apply it to their portfolios” session. If you are a client and interested in a link to my video interview, please email me at blumenthal@cmgwealth.com.

I know I hit you with a lot today. I do hope you find this information helpful. I was asked to do a podcast summary of each letter and I think it is a good idea. It may be easier to take in some of these letters with sneakers on and ear buds plugged in. Stay tuned.

Wishing you a great week,

Stephen B. Blumenthal

Executive Chairman & CIO