Harvesting Fear and Greed

This research note was originally published by the CFA Institute’s Enterprising Investor blog. Here is the link.

Q1 hedge fund letters, conference, scoops etc

SUMMARY

- Option-based strategies generated better risk-adjusted returns than the S&P 500 over the last 30 years

- Investors should be wary of buying options and focus on harvesting the volatility risk premium by writing options

- Option-based strategies are an interesting alternative to long-short equity hedge funds for reducing risk

BUYING VERSUS SELLING OPTIONS

The investment banking divisions of Goldman Sachs, Morgan Stanley, and similar firms pride themselves on servicing sophisticated, blue-chip institutional clients. They mostly avoid the retail market because there is less to be gained – except for certain niches that are too profitable to ignore. Selling derivatives to German retail investors is one such niche.

Although German investors tend toward the conservative, with an unhealthy preference for low-interest–paying saving accounts, many have a dark side that manifests itself in the trading of such highly complex derivatives as digital or Asian options. Retail investors are not well-equipped to use or price options. This means they mostly lose money, but it makes an attractive business for the investment banks issuing the options.

But there is a big difference between buying options – often for speculation – and selling them, which exploits the fear, greed, and ignorance of investors. Some US mutual funds pursue strategies that include writing options, whether to generate additional income or to offer protection against market crashes.

Given low interest rates and concerns about a market downturn, option-based approaches have become popular in the United States in recent years. Currently, there are more than 70 such strategies – an all-time high. So do option-based approaches offer any value to investors?

THE LONG-TERM EVIDENCE

The Chicago Board Options Exchange (CBOE) publishes indices for several option-based strategies with data going back 30 years. Two of these indices are among the most well-known:

- CBOE S&P 500 BuyWrite Index (BXM) employs a covered call approach that buys the S&P 500 and sells at-the-money calls on the index.

- CBOE S&P 500 PutWrite Index (PUT) sells at-the-money S&P 500 puts and invests the cash in short-term Treasuries.

BXM and PUT have the most appeal when we expect the market to move sideways or trend moderately. The downside is partially hedged through the income generated by writing options. However, there is limited upside and the strategies underperform during sustained market upswings like those in recent years.

Allocating to these strategies might have less appeal if we’re buy-and-holders who believe the equity markets will continue on their upward trajectory and want to aggressively compound our returns. Given that these approaches have optimal implementation windows, they require specific views on the market, which can be challenged as market timing.

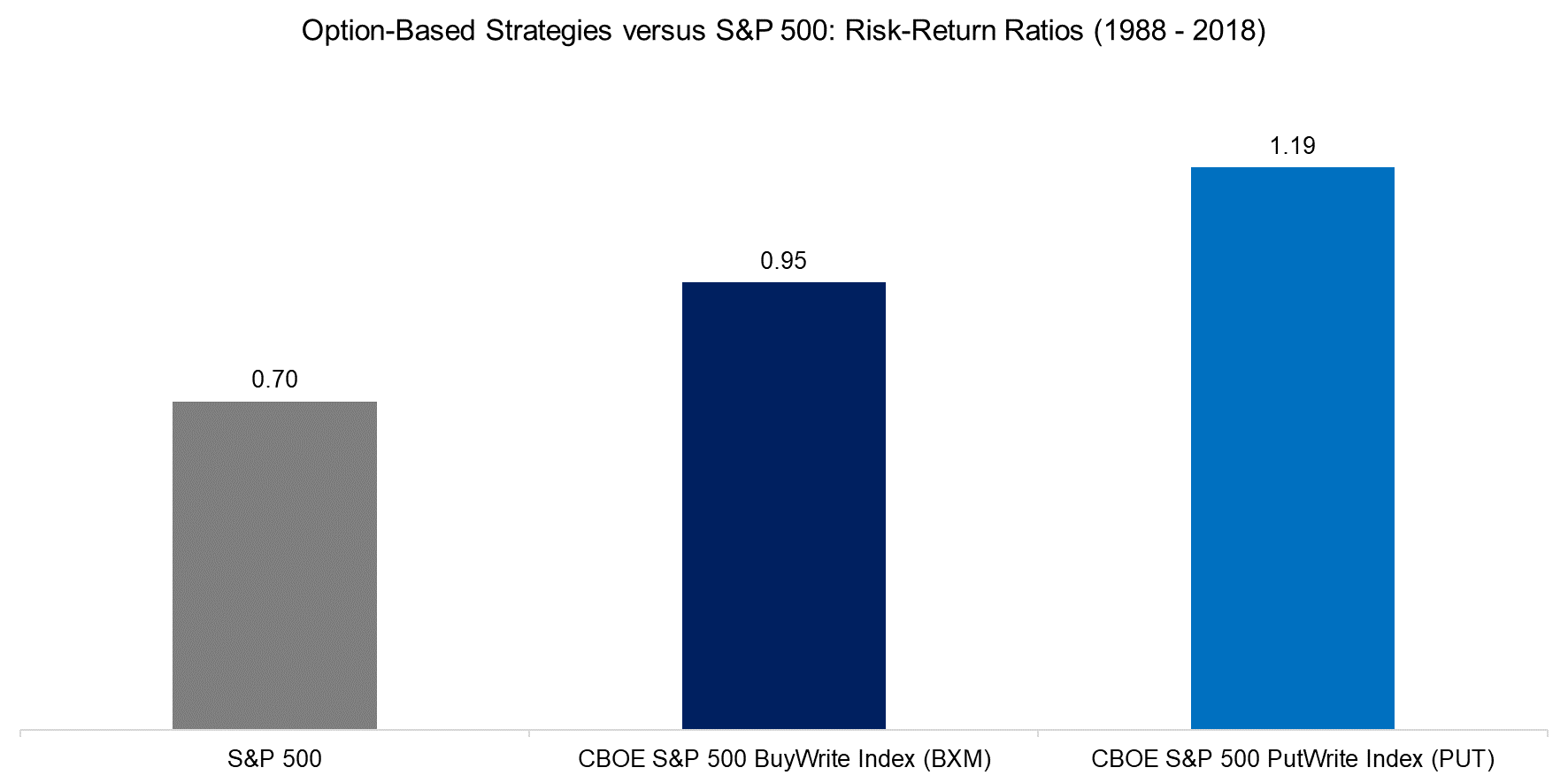

Theoretically, both strategies should have the same returns given the put-call parity, no-arbitrage condition. But PUT generated higher risk-adjusted returns than BXM over the last three decades because of differences in portfolio construction. Both option-based strategies significantly outperformed the S&P 500.

Source: CBOE, FactorResearch

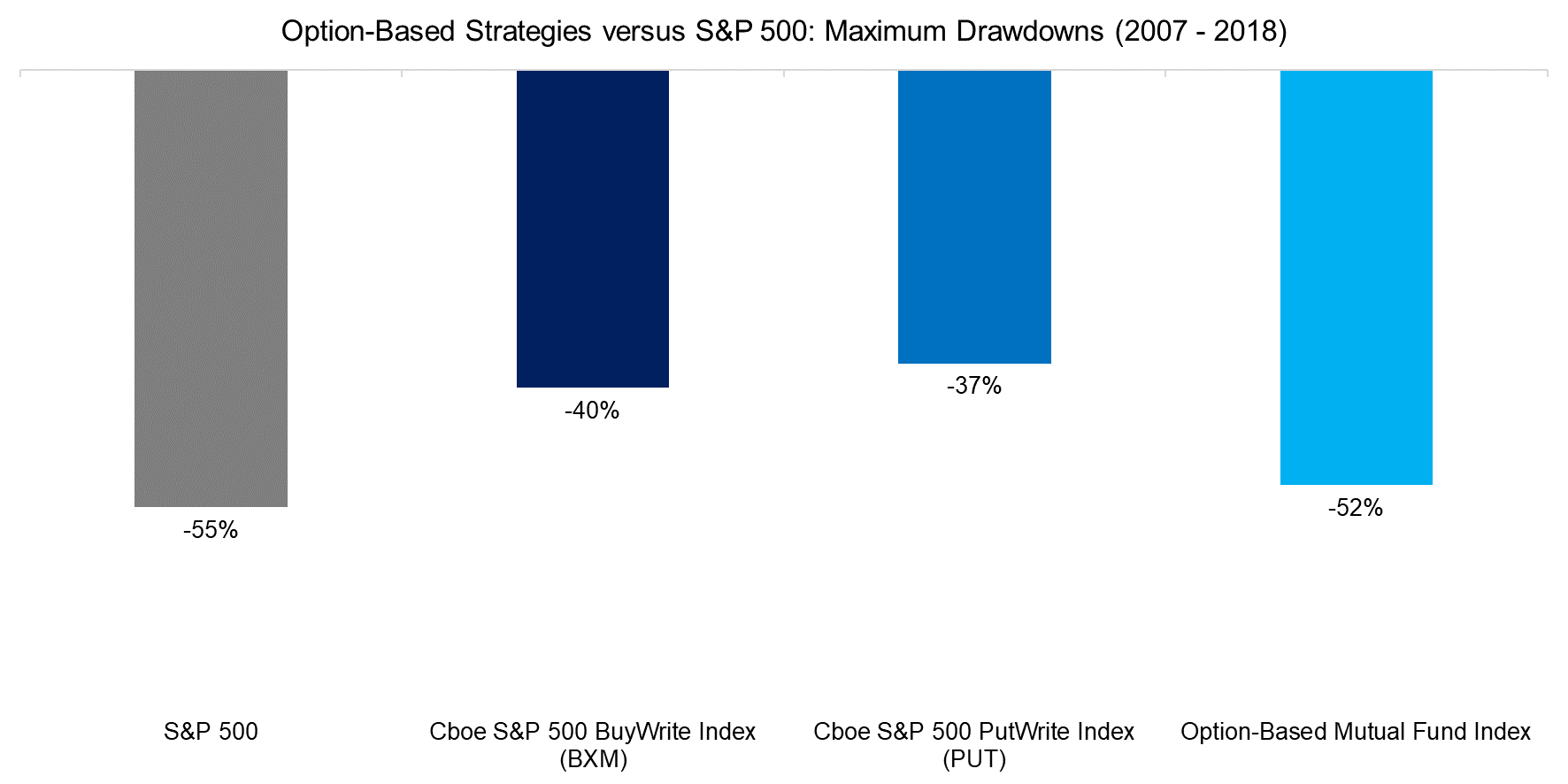

The high risk-return ratios relative to the S&P 500 are due to higher returns as well as lower volatility. Both BXM and PUT significantly reduced the maximum drawdown of the S&P 500 during the global financial crisis in 2008 and 2009. Based on these favorable results, option-based strategies could even be considered potential replacements for core equity positions.

However, BXM only became directly investable through an exchange-traded fund (ETF) in 2007 and PUT in 2016. Option-based mutual funds have been available for decades, but an equally-weighted index created out of these would not have substantially reduced the maximum drawdown of the S&P 500. So, how to reconcile the attractive performance of the indices with the less favorable results from actual investment products?

Source: CBOE, FactorResearch

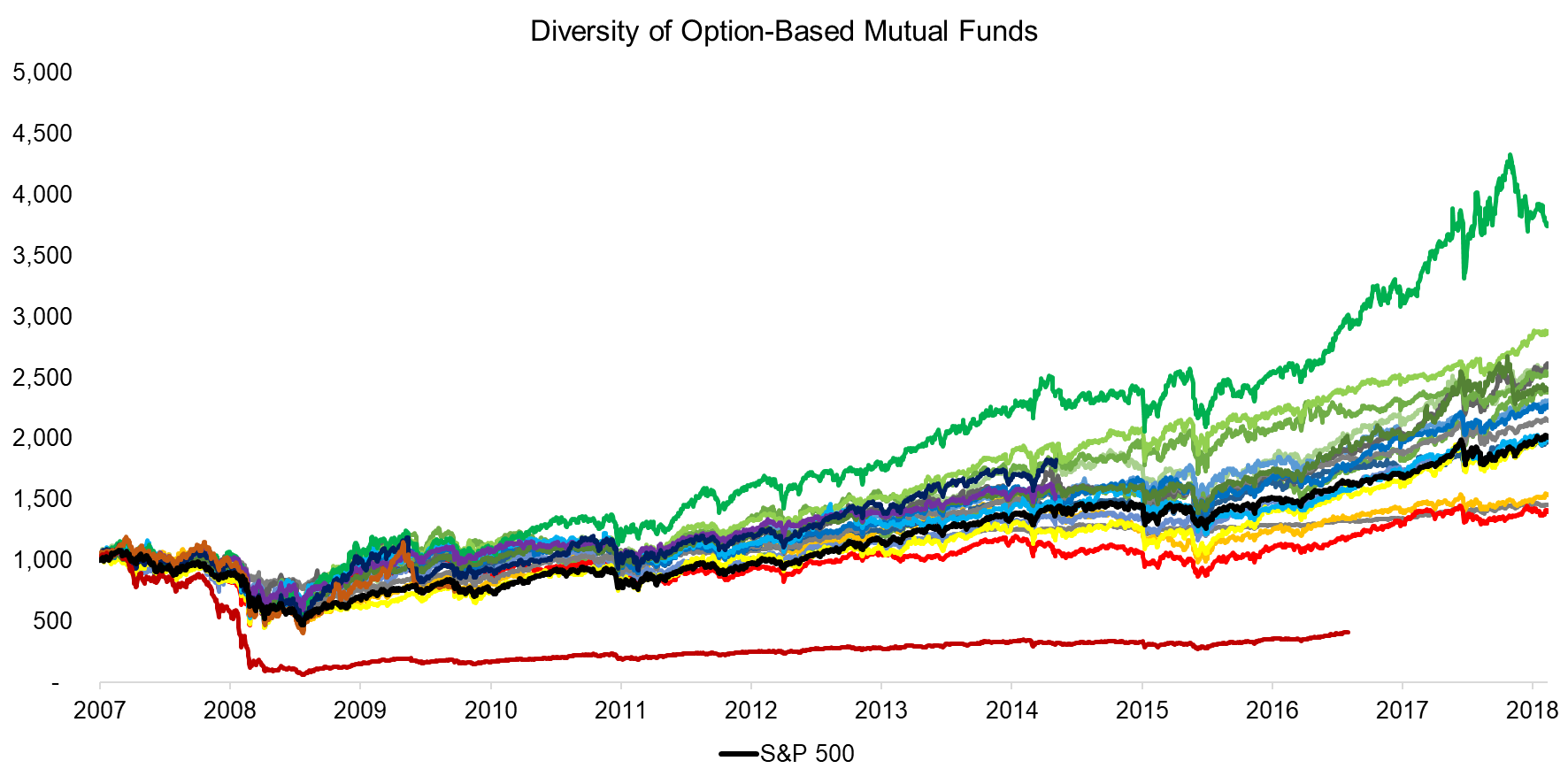

DIVERSITY OF OPTION-BASED STRATEGIES

That there is a volatility risk premium is supported by academic research and explained by realized volatility being systematically lower than implied volatility. In the case of put options, investors fear a market downturn and pay option sellers for protection. Writing put options is like selling insurance policies, which tend to come with a premium.

The vast universe of option-based strategies can broadly be divided into three categories: income-generating, hedging, and tactical trading. Income-generating approaches harvest the volatility risk premium, although this is less clear for the other strategies. Speculating with options is much more challenging, which may explain why some option-based mutual funds performed as poorly or worse than the market during the global financial crisis.

Source: FactorResearch. The analysis includes liquidated funds.

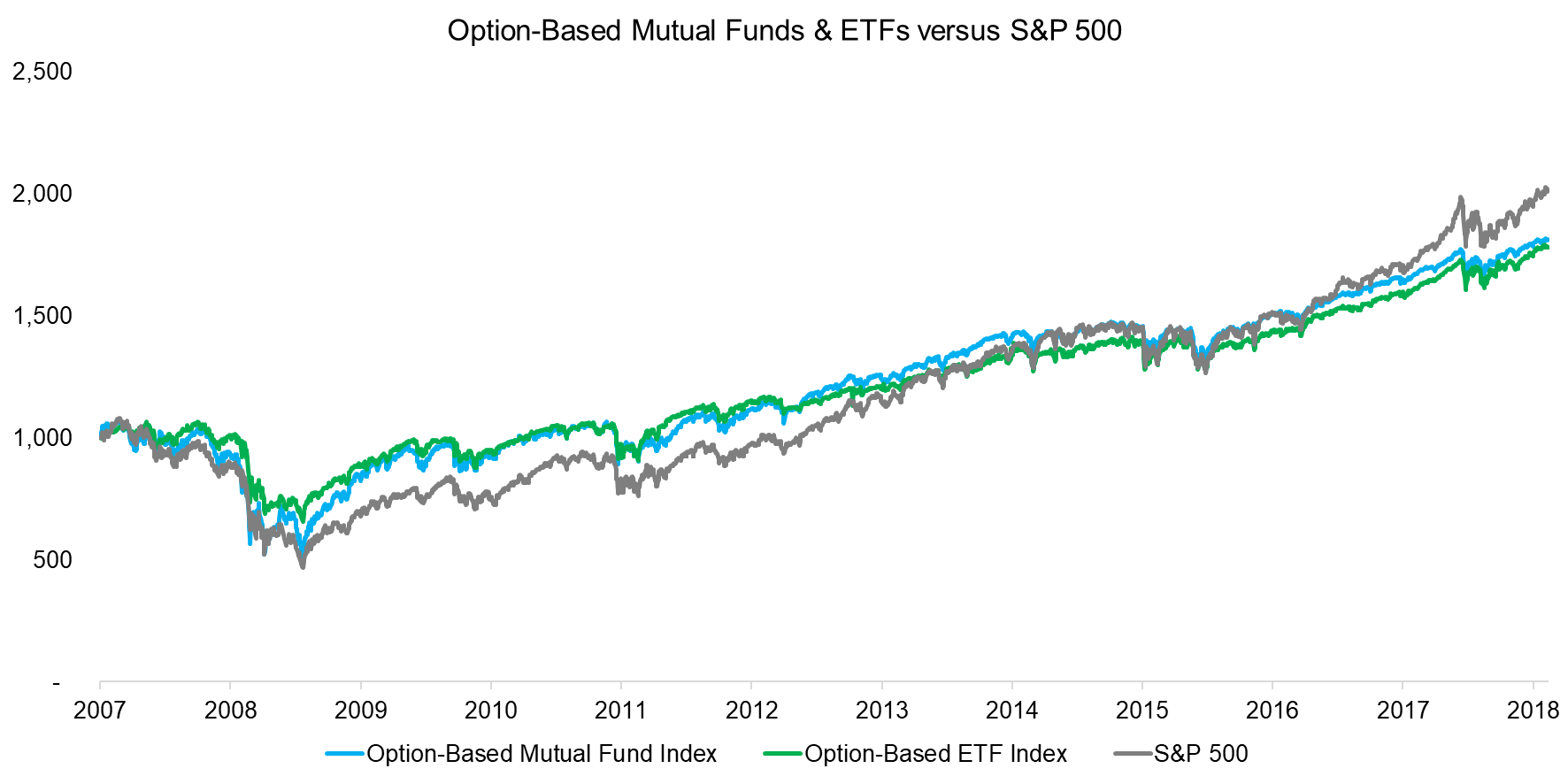

ETFS TO THE RESCUE?

The diversity of option-based mutual funds highlights the challenge of manager selection. Most mutual fund managers see their investment process as their competitive edge so are not inclined to reveal it. A lack of transparency combined with the complexity of options is not a good recipe for mutual fund selection.

Fortunately, such strategies as BXM and PUT are now available as ETFs. While this doesn’t reduce their complexity, we can at least analyze the long-term historical data of the underlying indices, and, naturally, ETFs are more affordable than mutual funds.

Option-based mutual funds and ETFs behave roughly as expected when compared to the S&P 500 since 2007. Both underperformed in the bull market of recent years, but outperformed during the global financial crisis in 2008 and 2009 and ETFs had a significantly lower drawdown during that period.

Source: FactorResearch

OPTION-BASED STRATEGIES VERSUS HEDGE FUNDS

The popularity of low-volatility strategies in equity portfolios reflects investors’ desire for securities that offer equity returns with lower volatility. This analysis, as well as related research, demonstrates that such option-based approaches as BXM or PUT effectively deliver what these investors are seeking.

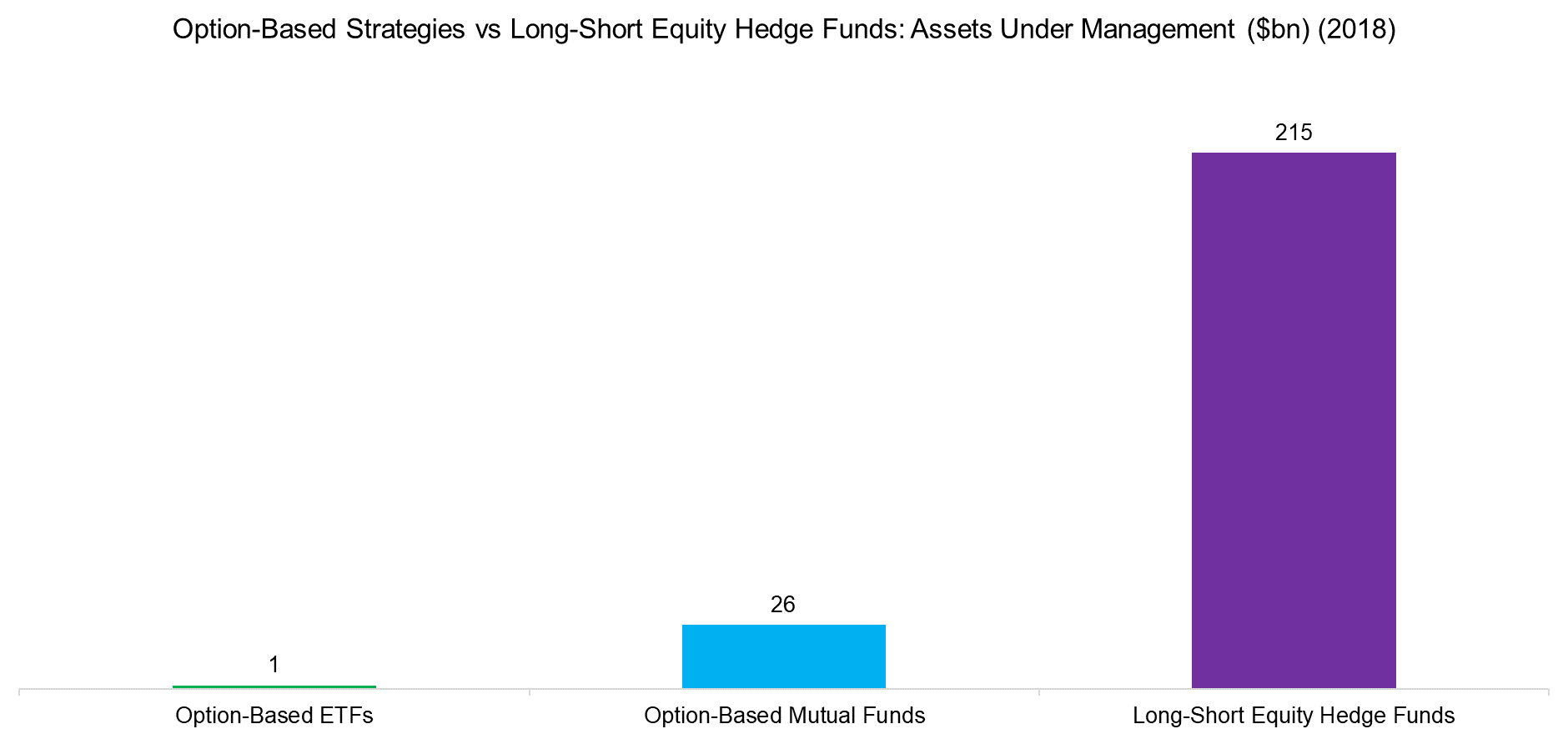

But what’s difficult to explain is that option-based ETFs barely exceed $1 billion in assets under management (AUM) and option-based mutual funds account for only about $26 billion in AUM. Both figures are fairly negligible in the context of the investment industry.

In contrast, long-short equity funds, which also aim to provide equity exposure with lower risk and reduced drawdowns, manage more than $200 billion in assets. But because of their exorbitant fees, they mostly fail to achieve equity returns with lower volatility. So we might consider option-based strategies potential alternatives to long-short equity hedge funds when it comes to reducing equity risk.

Source: BarclayHedge, FactorResearch

FURTHER THOUGHTS

The Financial Conduct Authority (FCA) in the United Kingdom recently banned the sale of binary options to retail investors and restricted the sale of contracts-for-differences (CFDs), which cost UK retail investors between $350 and $600 million in estimated annual losses per year.

Investors should be wary of derivatives for speculative purposes, but might well use them to exploit the fear and greed of others by harvesting the volatility risk premium. One person’s loss is simply another’s gain.

RELATED RESEARCH

Liquid Alternatives: Alternative Enough?

ABOUT THE AUTHOR

Nicolas Rabener is the Managing Director of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Article by Factor Research