Owens & Minor (OMI) is a small (~$1 billion market cap) medical supplies distributor.

The company has seen its earnings-per-share decline in 2017 and 2018, though it is still profitable – and its dividend was well covered by adjusted earnings.

Q3 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Which is why we did not expect the company to reduce its dividend… But this morning, Owens & Minor slashed its quarterly dividend from $0.26/share to just $0.075/share. Shares have tumbled ~30% following the announcement.

So what should investors do?

Key Metrics

Overview & Current Events

Owens & Minor is a healthcare logistics company that provides packaged healthcare products for hospitals and other medical centers. The company has a market capitalization of $935 million and distributes ~220,000 different medical and surgical supplies to ~4,400 hospital systems worldwide.

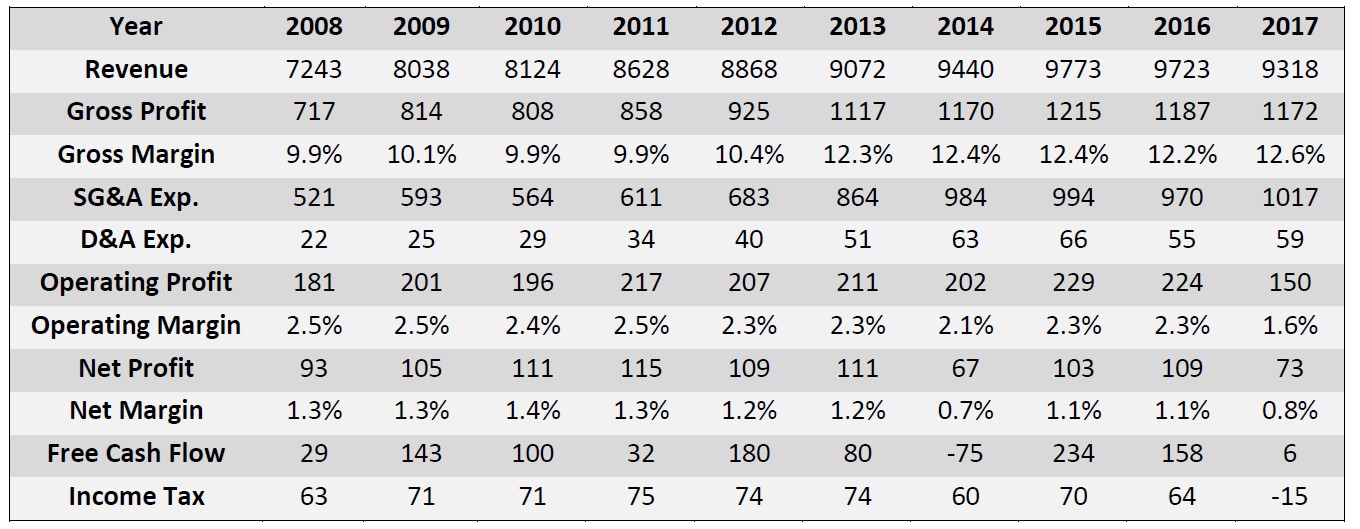

Owens & Minor reported 3rd quarter 2018 earnings on October 31st. Revenue grew 5.6% due to the acquisitions of Byram Healthcare and Halyard. Adjusted operating income for the quarter grew slightly, from $48.5 million in the same quarter last year to $48.8 million. Adjusted earnings-per-share fell from $0.40 in the third quarter of 2017 to $0.32 in the third quarter of 2018. Owens & Minor’s Chief Executive Officer Cody Phipps had this to say about quarterly results: “The strategic moves we have made into attractive alternate sites of care with Byram, and in meaningfully building our own brand product portfolio with Halyard, have strengthened and diversified our business. These new businesses are helping to offset the continued pressures we face in our domestic distribution business.”

Owens & Minor again slashed its guidance for 2018. Fiscal 2018 guidance was reduced from $1.45 at the midpoint to $1.225 at the midpoint. Worse yet, the company announced a significant dividend reduction on October 31st. Owens & Minor is reducing its dividend payable January 2nd, 2019 from $0.26 to just $0.075 per share. This ends a streak of 19 consecutive years of dividend increases. We are highly displeased with this announcement and view it as unnecessary, as the dividend was covered by adjusted earnings.

Growth on a Per-Share Basis

Owens & Minor has recently completed a number of promising acquisitions that should fuel its growth for the foreseeable future. Last year, the company closed (8/1/17) on the acquisition of Byram Healthcare, a $380 million purchase that generate $450 million in sales for the company. More recently, Owens & Minor announced (11/1/17) the acquisition of Halyard Health’s surgical & infection prevention (S&IP) business for $710 million – the largest acquisition in Owens & Minor’s history. While these two transactions should help earnings to grow in the future, Owens & Minor has struggled as of late with poor execution and rising costs. We are forecasting a return to earnings-per-share of $1.60 by 2023 which corresponds with a growth rate of 5.6% over the next 5 years. This is significantly lower than our 8% expected earnings-per-share growth we had from last quarter, as the recent dividend cut and continued poor performance casts additional doubt on Owens & Minor’s management teams’ ability to grow the business.

Valuation Analysis

Using the midpoint of Owens & Minor’s new 2018 financial guidance, the company is trading at a price-to-earnings ratio of just 7.9. While Owens & Minor has performed poorly in 2017 and 2018, the company is trading at a steep discount to fair value. Due to recent struggles and the dividend cut, we are reducing our fair value price-to-earnings ratio from 18.0 to 15.0. Even with the new lower fair value price-to-earnings ratio, Owens & Minor shares have the potential to generate annualized returns of 13.7% from valuation multiple expansion if it returns to fair value in 5 years.

Safety, Quality, Competitive Advantage, & Recession Resiliency

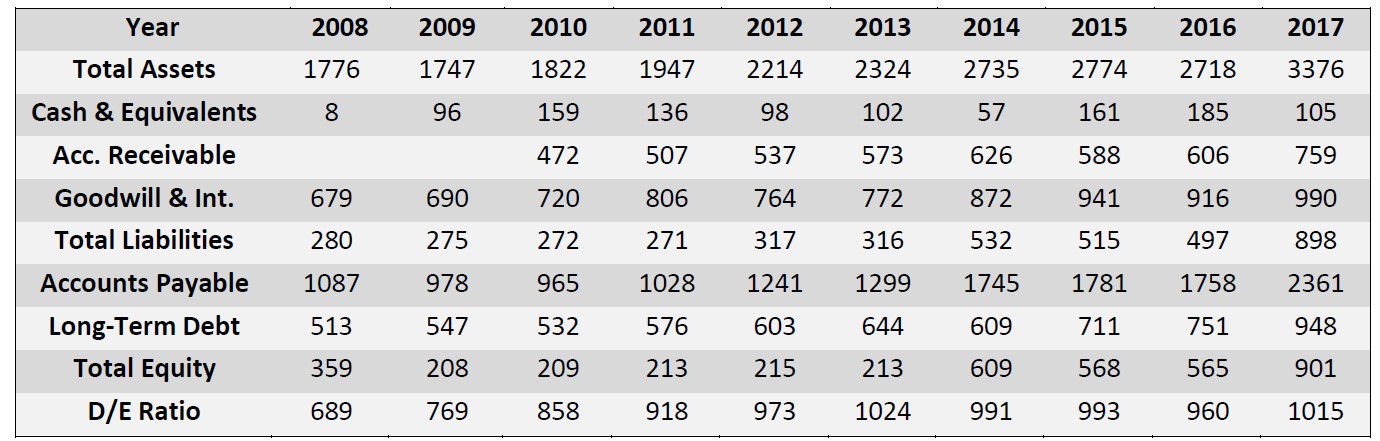

Owens & Minor has experienced a deterioration in several of its quality metrics in the last several years. Most notably, its dividend payout ratio has increased and its interest coverage ratio has fallen (because of the $450 million of new debt it acquired to fund the Halyard Health acquisition). These metrics should improve over the next several years. The recent dividend cut makes another dividend cut unlikely and gives the company room to pay down debt.

Owens & Minor’s weakening competitive advantage comes from its entrenched position within the healthcare distribution industry and its strong relationships with customers. The company has a customer base of approximately 4,400 hospital systems and boasts an on-time delivery rate of 99%. Owens & Minor is also very recession-resistant. The company increased its adjusted earnings-per-share each year during the 2007-2009 financial crisis.

Final Thoughts & Recommendation

Owens & Minor’s dividend cut comes as a great disappointment. The company’s stock price has collapsed ~30% the morning of the dividend cut and 3rd quarter earnings release. As a result of this price decline, Owens & Minor stock still looks poised to generate excellent total returns over the next 5 years. With that said, the company clearly cannot be relied on for reliable dividend growth. Owens & Minor is still a buy for value and total return-oriented investors at current prices. The company is a pending sell for dividend and income investors; it should be sold when trading around fair value, not at current prices where it is extremely undervalued.

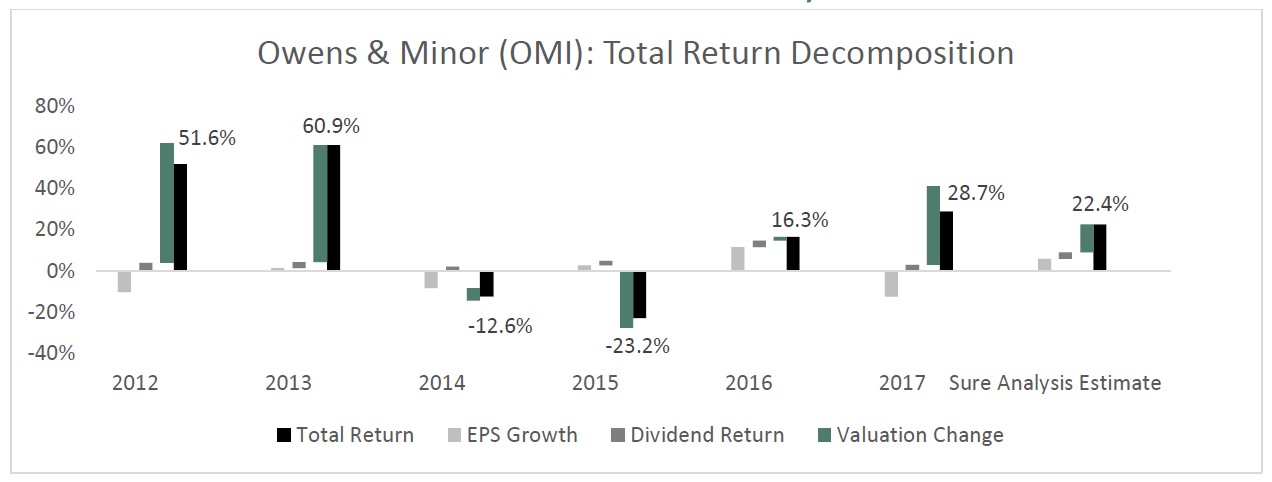

Total Return Breakdown by Year

Income Statement Metrics

Balance Sheet Metrics

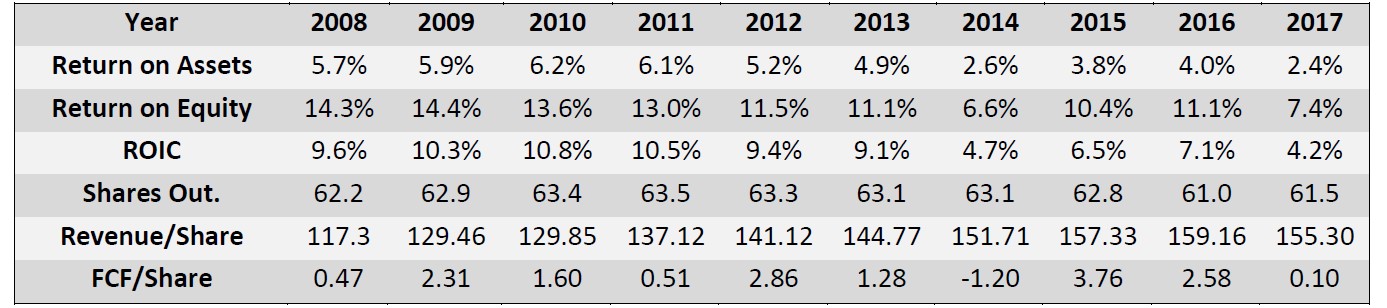

Profitability & Per Share Metrics

Article by Ben Reynolds, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.