We’ve just been reading through the latest Fairfax Financial Annual Report 2018 in which Prem Watsa discusses his failed attempt to short indices (mainly the S&P500 and Russell 2000) and a few common stocks, saying:

Q1 hedge fund letters, conference, scoops etc

In the past, to protect our equity exposures in uncertain times, we shorted indices (mainly the S&P500 and Russell 2000) and a few common stocks. After much thought and discussion, it became clear to me that shorting is dangerous, very short term in nature and anathema to long term value investing. As I mentioned to you in last year’s annual report, shorting has cost us, cumulatively, net of our gains on common stock, approximately $2 billion! This will not be repeated! In the future, we may use options with a potential finite loss to hedge our equity exposure, but we will never again indulge anew in shorting with uncapped exposure. Your Chairman continues to learn – slowly!!

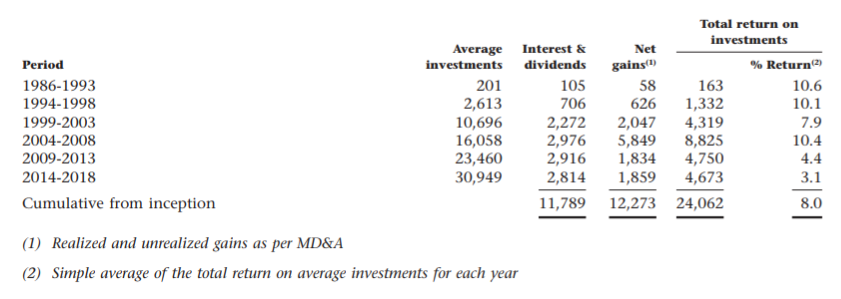

Further down in his letter Watsa demonstrates just how difficult it’s been to be a value investor over the past decade with annual returns of just 3-4%:

(Source: Faifax Financial Annual Report 2018)

You can read the entire 2018 Annual Report here: Faifax Financial Annual Report 2018.

For more articles like this, check out our recent articles here.

Article by The Acquirer’s Multiple