Managers in the region are providing investors with outsized returns to compensate for risk.

Q2 hedge fund letters, conference, scoops etc

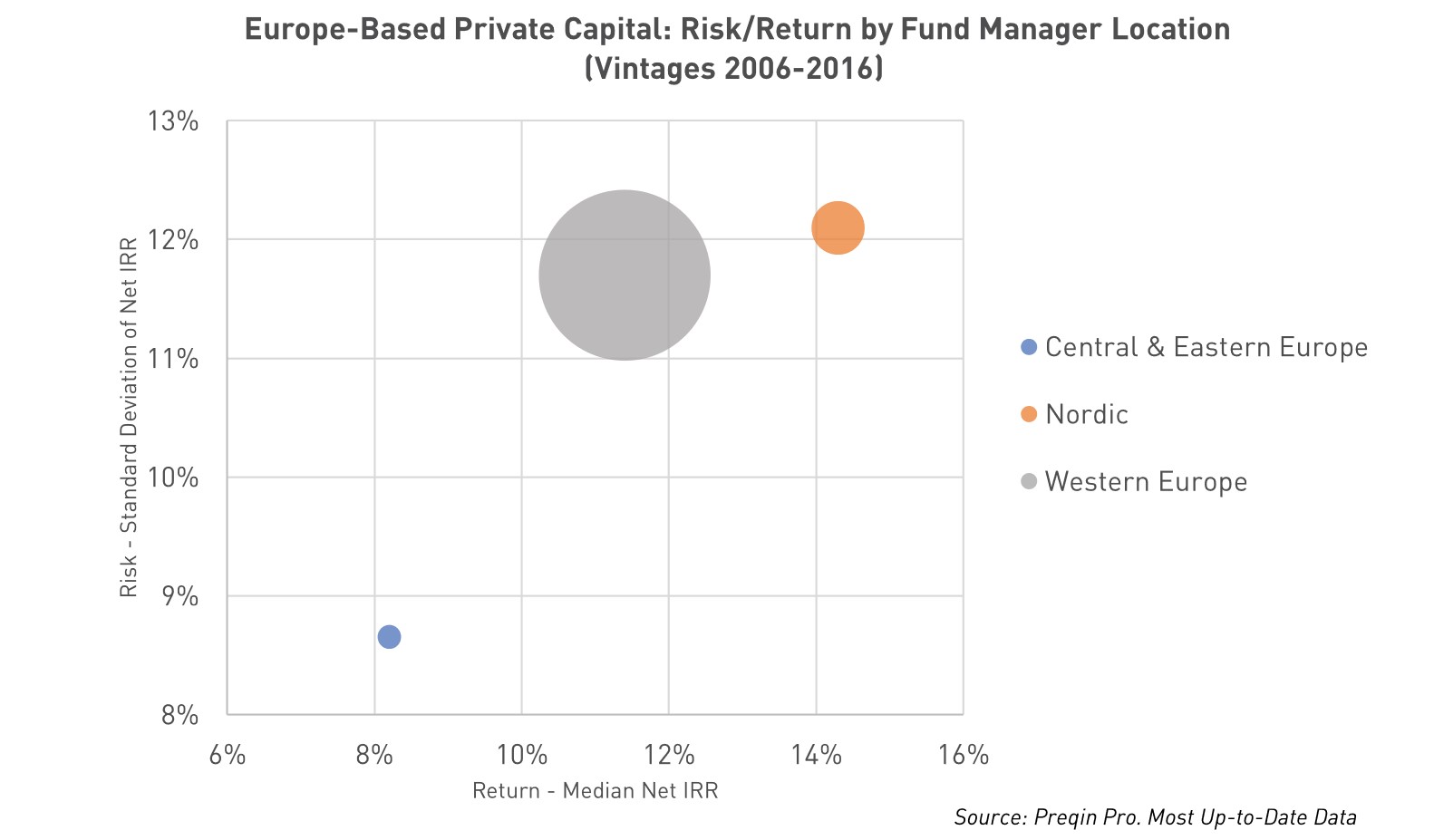

Although the majority of European capital is concentrated among Western Europe-based managers, Nordic-based fund managers have offered investors the largest return compared with firms in Western Europe and Central & Eastern Europe. The associated risk is marginally larger in comparison, though these impressive return figures are the rewards investors would expect as compensation.

Preqin Pro tracks the performance of over 1,500 Europe-based unlisted private capital vehicles of vintages 2006-2016. Using this data, it is possible to analyze the risk/return profiles associated with committing capital to managers in based in different regions of Europe.

As shown in the chart below, Nordic-based managers exhibit a median net IRR of 14.3% and median standard deviation of 12.1%. At the other end of spectrum, funds in the less developed Central & Eastern Europe region have produced the lowest median return (+8.2%), but with the lowest associated risk (8.7%).

The quartile rankings of Nordic-based funds also reflect the success they are enjoying: 36% are ranked as top quartile in their respective benchmark groups, with only 18% in the bottom quartile.

Winning the Competition

With Europe-based private capital assets under management (AUM) having grown each year over the past decade, competition between fund managers for investment opportunities is at an all-time high. Institutional investors need to be fully aware of the risk and reward profiles when committing capital to managers.

Nordic-based managers have attracted over 4x more private capital than managers in the much larger Central & Eastern Europe, and Nordic-based AUM has increased at a greater rate than both other European regions. Recent fundraising statistics also reflect the rising investor appetite for Nordic-based funds, and the largest Europe-based fund closed since 2018 was managed by Swedish-based EQT – this is the eighth fund in a series of buyout funds raised by the firm over the past 25 years.

As Nordic managers continue to provide investors with outsized returns, we expect fundraising and AUM in the region to continue increasing. The current risk/return profile seems skewed in comparison to the performance of managers in other European regions – for the additional returns, it would be expected that the gulf in risk would be larger than it is currently. With dry powder accumulating in the region, increased competition between managers for opportunities is likely to lead to higher valuations. This could provide more sporadic returns, increasing the risk profile to a figure more in line with the large returns on offer.

Looking for more performance data and analytics? Preqin Pro provides transparent fund-level data, including individual fund performance; benchmarks by strategy, vintage year and geographic focus; PME benchmarks; PrEQIn Private Capital Index; horizon IRRs and cash flow. Take a demo today to find out how Preqin Pro can help you.

Article by Jaysul Mistry, Preqin