The economic calendar is full, including all of the big reports except employment. There will be some attention to the data, but I expect competition from Congress. Many will be asking:

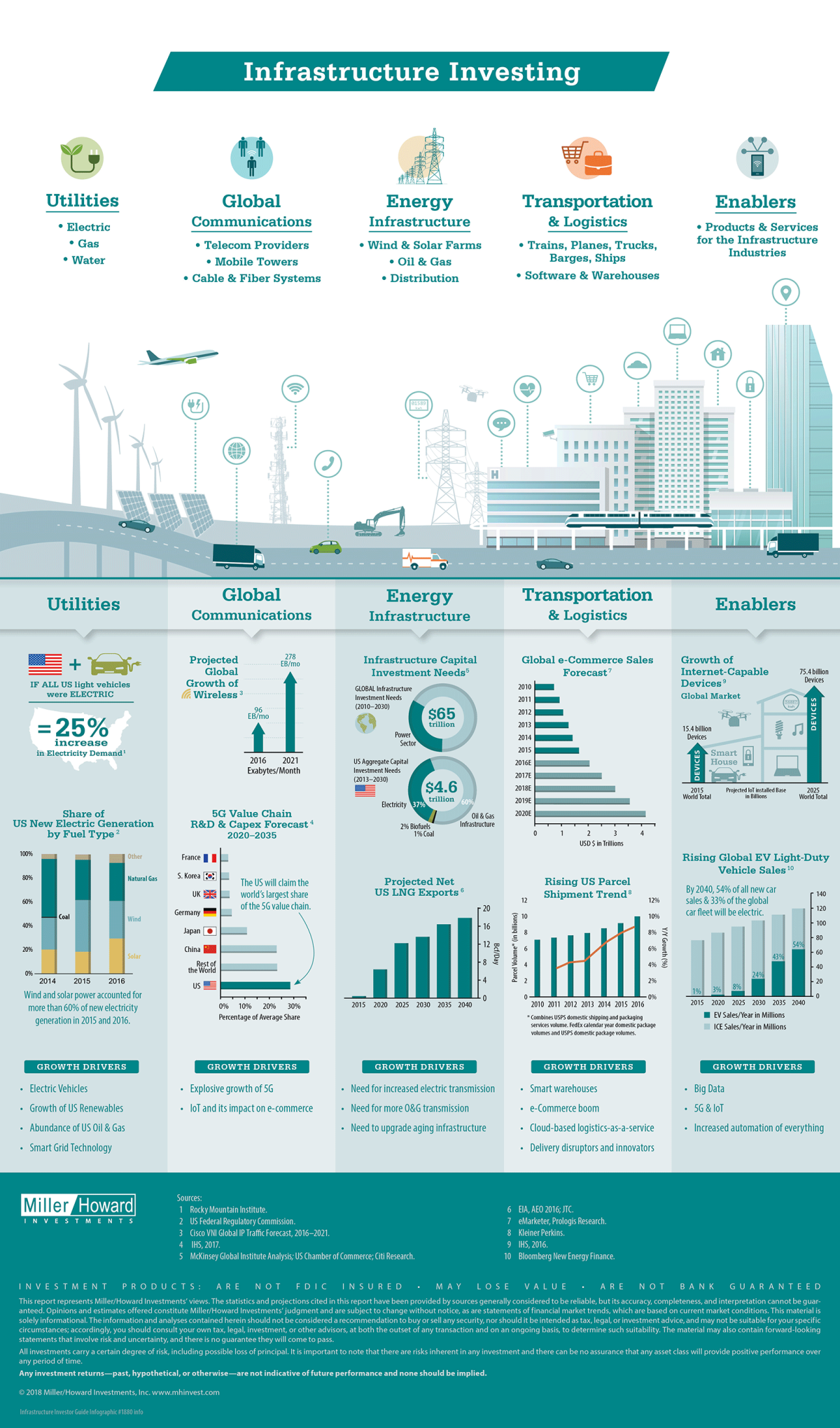

What are the chances for an infrastructure bill?

Last Week Recap

My last edition of WTWA I predicted a continuing discussion of whether stocks had put in a bottom. That was the topic at the start of the week, including conflicting opinions from two big firms. The Fed minutes provided a brief interlude at mid-week, but then it was back to “V” versus “W” for the shape of the rebound.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the Doug Short design with Jill Mislinski updates and commentary. You can see many important features in a single look. She includes not only the price changes, but also volume and helpful callouts. The entire post includes a great collection of charts and analytical observations.

The gain for the week included a 2% trading range. This was much less than the last two weeks but still high in comparison to the last year.

Personal Note

As noted last week, I am off this weekend – doing well in my competition and having a good time. I know that many appreciate an indicator update. I hope that an abbreviated WTWA is better than nothing.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news was mixed. Leading indicators were very strong, up 1%. Initial claims fell to 222K. Existing home sales declined from December and missed expectations. The market reacted much more to the Fed minutes (a bit more hawkish than expected) than to any of the economic data.

The Ugly

A troubling twist on an old scam. The IRS calls with a threat to arrest you. It all starts with data stolen from tax providers. (Washington Post).

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

We have a pretty heavy calendar. All the big reports except employment are on the calendar. Any or all could command attention. I am most interested in PCE prices (reaffirmed as the favorite Fed indicator), personal spending, and the ISM index.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

Despite the big economic calendar, I expect a forward look at new policy. Many will be asking:

What are the prospects for an infrastructure bill?

I have expressed disappointment that the proposed Federal contribution to this proposal is so small. Some disagree sharply, encouraged by the attractions for private investors.

I am shopping for ideas in this space, especially companies expected to benefit from favorable tax treatment. I liked this presentation from Jeff Desjardins, especially as a guide to one’s own research.

I am not going to add anything to this now, but it is a sector worth investigation.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

Short-term market health continues to lean bearish and could still turn negative. We are watching this closely. If there is further market deterioration, we will exit some or all trading positions. Long-term indicators remain bullish, in line with the conclusions from our fundamental analysis. Vince’s excellent measures of market health predict danger, but not always a decline. Trading results can be improved by exiting dangerous markets.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession. His business cycle index, which we use in the Indicator Snapshot, is no longer “on the peg” at 100, but does not indicate a recession.

Insight for Traders

Our discussion of trading ideas has moved to the weekly Stock Exchange post. The coverage is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. Each week we explore a topic of current interest, drawing upon trading experts. This week we asked traders, “Are you out of your comfort zone?” We illustrated the exit techniques of our trading models. Performance updates are published, and of course, there are updated ratings lists for Felix and Oscar, this week featuring the NASDAQ 100. Blue Harbinger has taken the lead role on this post, using information both from me and from the models. He is doing a great job, presenting a wealth of new ideas and information each week.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility! I remind investors of this each week, but now is the time to pay attention.

Most important of the Week

The most important takeaway from last week was the interaction between bonds and stocks. The knee-jerk reaction to the Fed minutes and the long end of the yield curve moving higher and stocks moving lower. As the week progressed, it seemed like stock investors were more comfortable with high rates and a steeper yield curve.

This is very healthy. It is needed for the current expansion to continue through economic and earnings growth.