“This U-Turn on nothing fundamentally changing is unprecedented. Three months ago, we were on ‘autopilot’ with the balance sheet and now the bond market is priced for a rate cut this year. The reversal in their stance is stunning.” – Jeffrey Gundlach – CEO, DoubleLine Capital LP

Q4 hedge fund letters, conference, scoops etc

Stunning indeed! What is Team Powell seeing that you and I are not seeing? Yields dropping; the bond market is on fire. If you’ve been away from the news, here is what’s going on. Well summed up by Camp Kotok fishing friend, Sam Rines, in his Thursday (March 21) blog post:

A solid majority of FOMC members favors no more rate hikes but the balance sheet contortions were the bigger surprise. The Fed will now taper the liquidation of its Treasury holdings in May and stop in September. More important, they will also let their mortgage securities portfolio mature and use the proceeds to buy more Treasury securities. That means purchasing a minimum of $300 billion in predominately shorter-term US Treasuries in 2020. Concluding, Basically, QE-lite is coming.

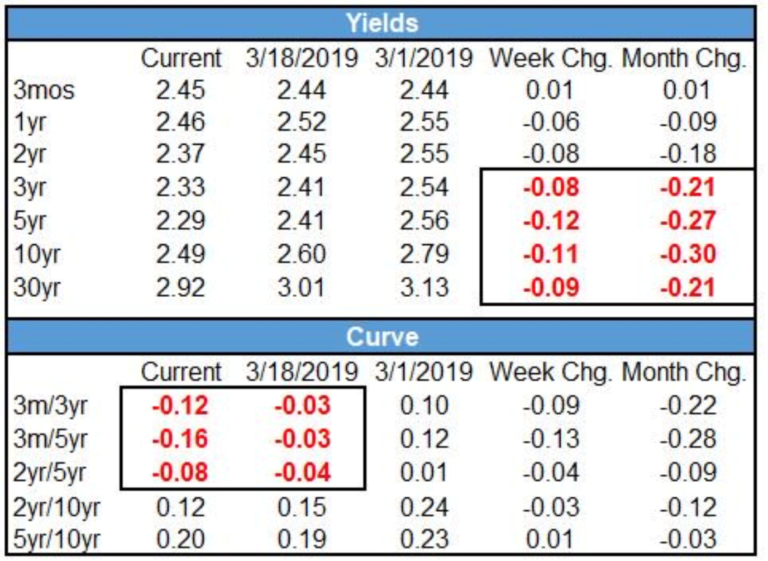

We now sit at the most inverted yield curve since August 2007. That’s when short-term yields are higher than longer-duration yields. @GS_CapSF tweeted this morning, “Remember when the SF Fed published a paper saying the 3-month vs. 10-year yield spread [the difference between the two yields] was the best predictor of recessions and there’s no need to worry since the spread is at 95 bps [for non-geeks, 100 bps equals 1%]. Fast forward 8 months and the spread is now just 7 bps.” The bond market is signaling something is up. (Comments in the brackets are mine.)

What gives? I believe it’s global recession. Not here in the U.S. just yet but in Europe and in China. Risk #1 in my view: nearing sovereign debt crisis and what that means to European banks. What is the Fed seeing that we are not seeing? My witty friend Ben Hunt had a particularly fun post this week. He took us back to the Nixon years and specifically Nixon’s relationship with then-Fed Chairman Arthur Burns. Burns was Nixon’s guy… and an election was on the horizon. Timely. You’ll find Ben’s short post below. Scroll to the “They’re Not Even Pretending Anymore” section.

Inverted Yield Curve

Each month I update the “Recession Watch” charts in Trade Signals as most of the data is produced monthly. One of the best recession predictors is the spread difference between the 2-year Treasury yield and the 10-year yield. The current difference is +0.12 bps. Recession has almost always followed when the number turns negative (inverts). But do keep an eye on the SF Fed’s 3-month vs. 10-year inversion predictor. Pundits will again be giving all sorts of reasons why this next time will be different. Odds say don’t listen to the pundits.

There is some good news here. Once the 2’s vs. 10’s invert, there is generally some time to prepare as the average lag from inversion to recession start is 14 months. But make no mistake, recession matters, as the stock market dropped -50% in each of the last two. If you are my kids’ ages, party on and dollar cost average. If you are a pre-retiree or retiree, you just can’t afford another 50% hit to your retirement funds… and the needed time it will take just to get back to even. Initial starting conditions matter. I’m not saying -50% is certain. Could be more or could be less. I’m saying the bad stuff happens in recession and the most severe declines occur when your starting condition is extremely overvalued markets. You can find more recession charts here (Trade Signals – page down to the Recession Watch section).

To give you a sense for what is going on in the bond market, the following chart shows the various yields as of early this morning (March 22, 2019). Note the curve is now inverted on the front-end (red numbers bottom section of the chart).

What the Fed is saying is “QE is coming back.” I am writing you from Salt Lake City where I presented at the Barron’s Independent Summit. I laid out my base case on coming returns, recession timing and risk regimes. I suggested there is much we can do. Just like in 1999 when a shift to value-oriented stocks made great sense. However, no one wanted to miss out on those daily spikes in tech stocks. It kind of feels like that today.

I was asked a question about debt. The advisor said, “We were told in the 1980s, 90s and 2000s that debt is too high but we continue on and debt hasn’t tanked us.” I answered that the size of the debt was never this high. It is north of 350% relative to what we produce as a country (GDP) and that story is even worse in much of the world. History shows the inflection point from sustainable to problem is at 300% debt-to-GDP. The last time we were in this position was in the mid- to late 1930’s. We are at the end of a long-term debt supercycle. Few of us have seen one and we have to figure out how we are going to get out of this mess (monetize the debt in the U.S. and globally). As Ray Dalio says, the outcome may be “beautiful” or “ugly” (the outcome late 1930’s was ugly – debt, populism, war). I believe in us, I said… I’m seeing “beautiful” but it’s going to get bumpy. There are better and there are worse solutions. We just don’t yet know what legislators and central bankers in the U.S., Europe, Japan and China will do. It will need to be with hands held together. Do you see that happening right now? This next quote pretty much sums up the conundrum.

The central banks, all their models are broken. All their models would suggest they would have done so much more in terms of interest rate hikes by now, but in fact they’re seeing that we’re not getting the inflation.

We’re operating in an environment that is spectacularly indebted and the main feature that has come out of that, along with the aging demographic, is a very, very, very, very low neutral interest rate.

That’s why Japan’s at zero, Sweden’s negative, the euro zone is at zero, Australia, New Zealand are at 1–2% with their high population rate and all these countries are decelerating [in growth]. There’s a massive amount of debt and that may be contributing to an incredibly low neutral level of interest rates.

– Robert Tipp, chief investment strategist and head of global bonds for PGIM Fixed Income

And this from Mark Yusko:

We know exactly what they (Fed) will do… seen movie before. 2007, Bank of Japan (“BOJ”) was at 26% of GDP on their balance sheet and said no more QQE, markets fell, QQE resumed and now BOJ has 100% GDP on its balance sheet and they own 46% of Japanese Government Bonds and 75% of ETFs… The ECB and the Fed are just BOJ with 9 to 11-year lag.

Earlier in his career Mark ran the University of North Carolina endowment fund. I’ll be with Mark Yusko in May at the Mauldin Economics Strategic Investment Conference.

We’ve got some figuring out to do. Grab a coffee and find your favorite chair. You’ll find Ben Hunt’s “They’re Not Even Pretending Anymore” piece and a thoughtful piece from my colleague and co-portfolio manager, John Mauldin, on retirement. The title is catchy, “Retirement Isn’t Happening.” He shares some good math and some insights on retirement planning. Finally, I so enjoyed listening to Michael Lombardi present at the Barron’s conference. Michael’s been in the NFL (on the talent side) and has been back together working for Bill Belichick and the New England Patriots since 2014. He is a major part of their success. It’s about culture and that is what he presented on. You’ll find my notes in the personal section. He was great… I’m hitting send and rushing to the airport. Can’t wait to get home to be with Susan. Some red wine awaits. Thanks for reading and do have a great weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- “They’re Not Even Pretending Anymore,” by Ben Hunt

- “Retirement Isn’t Happening,” by John Mauldin

- Mauldin, Blumenthal, Cucchiaro Podcast

- Trade Signals – The Trend Limps Higher

- Personal Note – It’s About Culture

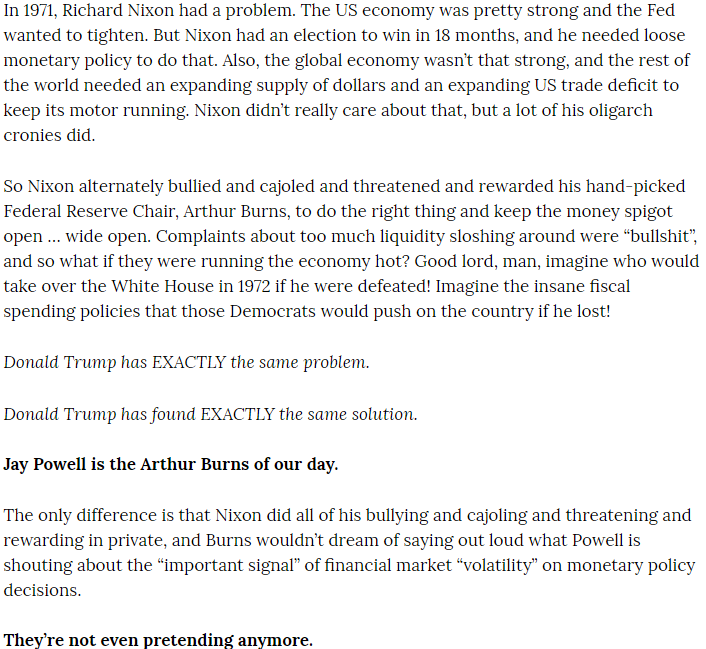

“They’re Not Even Pretending Anymore,” by Ben Hunt

Ben is a good friend with a brilliant mind yet do brace yourself as you read on… Ben hits hard in this particular piece. I don’t agree with his conclusion but I do appreciate taking in a different view. Ultimately we get to the same place as I share my two cents at the end of this section.

With permission from Ben:

Source: Ben Hunt, Epsilon Theory

SBB here (my two cents): As I indicated, Ben hit hard. I’m not in the “Donald Trump has found EXACTLY the same solution” camp. Perhaps indirectly… I don’t believe they make ideal bedfellows. I’m more in the “OMG, what must be happening that we are not yet seeing” camp. Is a major systemic player in crisis? My father used to say, “Watch what they are doing not what they are saying.” I see doing! Do consider following Ben on Twitter @EpsilonTheory, he’ll get you thinking.

“Retirement Isn’t Happening,” by John Mauldin

I have long said I don’t want to retire. I enjoy my work. It’s not too physical, other than the travel (which is finally beginning to wear on me). Also, my savings are not yet sufficient to sustain the retirement lifestyle Shane and I want. I could retire now but would rather wait.

Fortunately, I have the choice of continuing to work and adding to those savings. I realize many Americans don’t have that luxury. Some have to retire because of illness, or because their work requires more physical ability than their age allows. Many others don’t retire because they just can’t afford to.

TV commercials suggest a financial advisor is key to a leisurely retirement. A good one certainly can help, but only to the extent you’ve saved enough cash to give them something to invest. And as we’ll see, many Americans haven’t.

My readers tend to be conscious of these things. You probably have above-average income and savings. Maybe your retirement plan is on track, but that doesn’t mean you can rest easy. We all exist within a society and an economy. Its problems are ours, too, as we may find out when taxes rise to help pay for others to retire.

Today, we’ll look at the state of retirement in America, updating some data I shared a couple of years ago. Then we will look at some strategies to keep your plan realistic and on track.

Social Security Is Not Enough

How much money will you need to retire, and how much will you have? Answering those questions is one reason a good financial advisor is worth every penny you pay them. But let’s talk about some generalities.

Say you want to stop working at 65. You’re in good health and your family tends toward long lives. You expect to reach 90, having been retired for 25 years. Will Social Security alone be enough?

If you spent most of your life paying as much as legally possible into the system, and you retire in 2019 at age 65, your monthly benefit will be $2,757, which is then indexed for inflation (at least under current law). It jumps to $3,770 if you delay retirement until age 70.

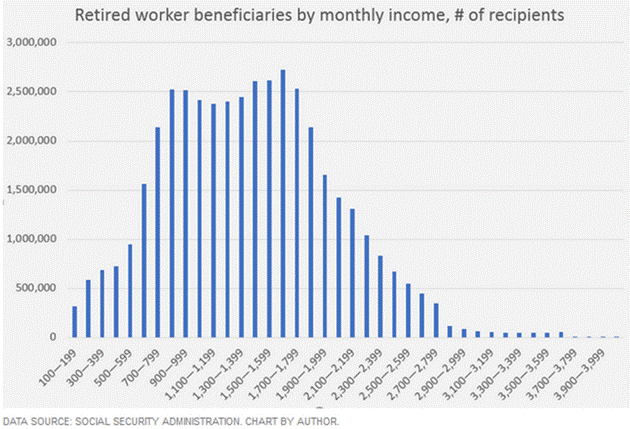

Since I am not yet 70 for another eight months, I really haven’t paid much attention to what I will get when I start my Social Security. I assumed like the charts that I’ve seen below that it would be a couple of thousand a month. I was surprised to learn I may get significantly more. Considering how much I’ve contributed over 50+ working years, it’s probably not that great a return. Yet most people get less. Here’s the distribution.

A solid majority of Social Security recipients receive $2,000 a month or less, and many less than $1,000. The average benefit is $1,413, according to Social Security’s latest fact sheet. If that’s all you have, your retirement lifestyle is not going to include many cruises and golf tournaments.

Of course, it shouldn’t be all you have. Social Security was never supposed to be a complete multi-decade retirement plan. It was designed to keep retired workers out of poverty at a time when lower life expectancies kept retirement much shorter for most—if they lived to 65 at all. Now we live longer, and we have higher expectations, which political leaders have done little to dampen. Often they’ve done the opposite.

Bottom line: Social Security probably won’t give you much security. You need more.

Is That All There Is?

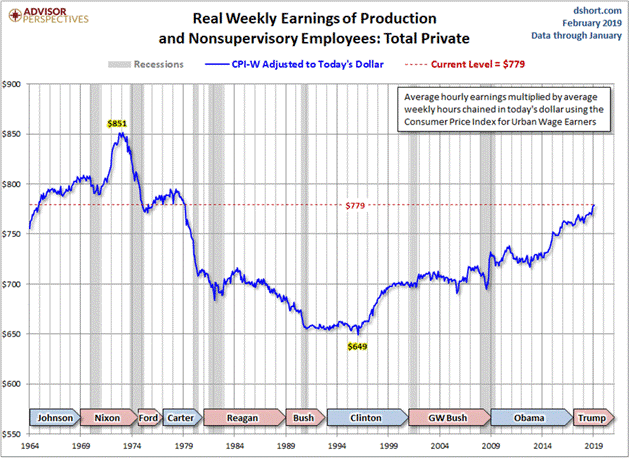

Ideally, people should avoid relying on Social Security and accumulate other savings as well. Many, perhaps most, do not. The reasons vary. I suppose some just spend their money unwisely and neglect to save anything. But income data says many Americans can’t afford to both live a typical middle-class lifestyle and save enough to finance a 20+ year retirement. Here’s a Doug Short chart to illustrate.

Source: Advisor Perspectives

In constant dollars and adjusting for hours worked, average weekly earnings for non-managers are now $779, and that’s an almost 40-year high. Millions of those now approaching retirement age spent their entire lives earning the equivalent of $40,000 a year, at most. Little surprise they don’t have six-figure retirement savings. The simple fact of the matter is, it takes enormous discipline to save even 6% for your 401(k) at that income level.

In a country of 330+ million people, shockingly few have enough retirement savings to support the stereotypical leisurely golden years. Dennis Gartman shared some disturbing numbers last week.

Firstly, we note that there were 133,800 “millionaires” late last year with sums of more than $1 million in their retirement accounts, which on its face, sounds like a large number. But that is down from 187,400 at the end of third quarter of last year, according to Fidelity Investments. According to the Federal Retirement Thrift Investment Board, which oversees TSPs, as of the end of last year, there were 21,432 “millionaires” compared to 34,128 at the end of September in those TSP accounts. The 4th quarter of last year was a disaster to those solely involved with equity investments; it was merely “horrible” for those with a more balanced investment portfolio.

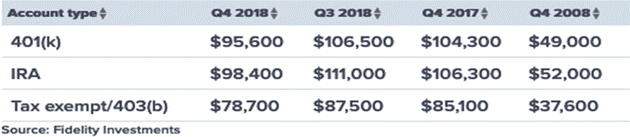

But these are not really our focus this morning; our focus is that the average balance in 401(k)s, 403(b)s, or IRAs fell to $95,600 at the end of last year from $104,300 at the end of the 3rd quarter for 401(k)s, to $78,700 from $85,100 for 403(b)s and to $98,400 from $106,300 for IRA balances. It was not the drops in value that caught our attention; it is the fact that the averages are only at or near $100,000, forcing us to wonder what sort of retirement can the average retiree look forward to with this minimal sum of money set aside? Is that all there is? Really? Is that really all there is? If so, we are in very real trouble.

The average IRA balance is not necessarily indicative of retirement savings generally, as many other vehicles exist, but it’s probably a good proxy. And an average of around $100,000 won’t yield much of a supplement to the monthly Social Security benefits described above.

I found this chart on CNBC, which also refers to the study Dennis quoted:

Many of our parents and grandparents had defined benefit plans and other guaranteed retirement benefits from the corporations they worked for. Those are increasingly an endangered species in the private sector while 401(k)s, IRAs, and Social Security aren’t giving the average person enough to retire on anything close to a comfortable lifestyle.

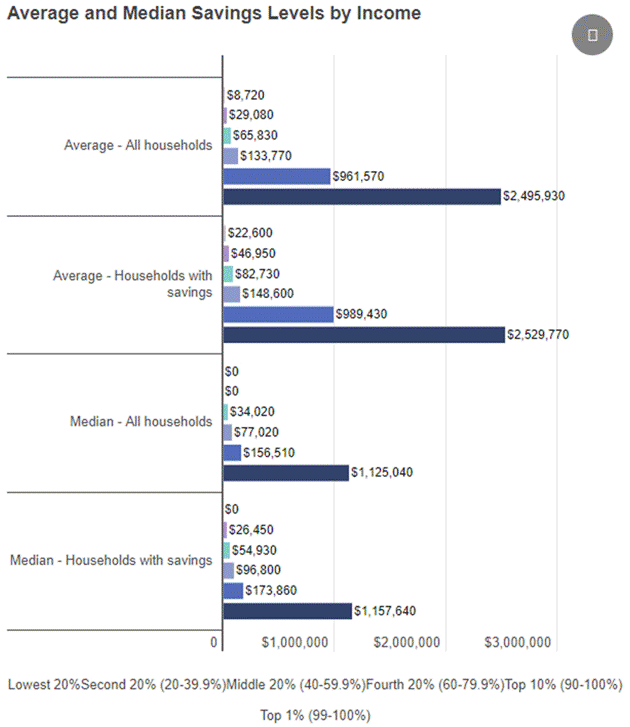

Average household savings for the bottom 40% are under $30,000. Median household savings for the bottom 40% are zero dollars. Clearly the top percentiles and especially the top 1%, skew the average. Note the bottom lines in the chart below is not the top 20%, but the top 1%. And the top 1/10 of 1%? Don’t make me giggle.

Source: cnbc.com

The point is that the 80% of households have less than $100,000 in savings. That is not enough for even a minimal retirement. Let’s make the very aggressive assumption that you can take 5% a year from your savings plan. If you have $100,000, that’s $5,000 yearly or about $417 a month—on top of your Social Security. And if you don’t have your house paid off? Or car?

The Indexing Problem in Retirement Accounts

Nearly every article I read on this topic talks about the fourth quarter’s losses, but something else leapt out at me.

Back-of-the-napkin math (and a rough napkin at that) says these retirement accounts are at least 50% invested in equity index funds. Some of you are now asking, “What’s the problem? All those index funds have come back. Everybody is back to where they started.”

Not so fast, Jack. As I have said until readers are probably tired of it, bear markets (which the last little bump in December barely qualifies for) that are not accompanied by a recession have V shaped recoveries. Which is exactly what we got.

Bear markets that are accompanied by recession take a very long time to recover and will likely be in the 40 to 50% loss range. A 50% loss requires a 100% gain to breakeven. That took about five years from the bottom of the last bear market.

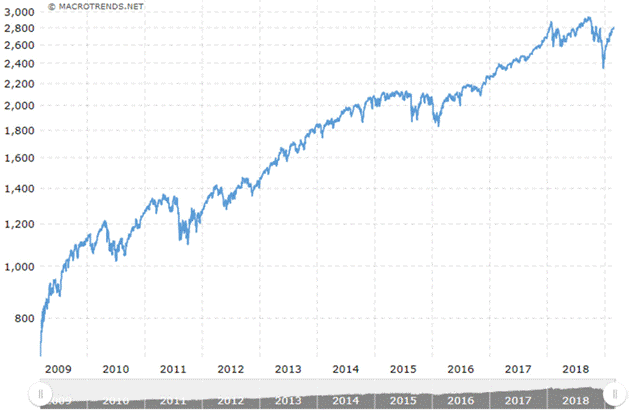

Now, let’s look at the chart from the S&P 500 for the last 10 years courtesy of Macrotrends. Note that the S&P is up well over 3.5x (give or take) in the last 10 years. But the 401(k)s and IRAs did not even double. Some of that is due to investors getting out at the bottom and back in later. Some is maybe due to high bond allocations in 2009 (bond funds had done very well, and we know people chase returns). But nonetheless, retirement funds have not performed as well as you might expect.

Source: Macrotrends

Further, when that next recession and bear market hit, it will take even longer to bounce back. The recovery will be even slower than this last one. As the research I’ve shared in previous letters shows, large amounts of debt slows recoveries. Very large amounts create flat economies. We are approaching large amounts in the US.

(Think what that large debt and recession did to Japan. What’s that song? Turning Japanese by The Vapors. The official 1980 video is not politically correct by 2019 standards but has some interesting historical tidbits along with the WWII propaganda silliness.)

In any event, the next recession will shortly cause a $30 trillion debt for the US government, soon to be followed by $40 trillion. Will that much debt turn us Japanese? That’s not entirely clear, since we have the world’s reserve currency and a unique role in global commerce and finance, but I think the recovery will be much slower, at a minimum. A double dip recession is clearly possible, making those stock market index fund losses even worse.

You must have some kind of strategy for dealing with market volatility. I don’t know how many times I can say that. But that’s the case only if you have savings to lose. Millions don’t, which means they have an even harder challenge.

Double Problem

I speak at a variety of investment events every year. Some are for high net worth investors, but others draw a broader crowd. Lack of retirement savings, both their own accounts and those of their neighbors and the rest of the country, is by far the most common worry I hear at those events. Sometimes it verges on panic, even among people who spent decades earning good incomes and saving all they could.

The Baby Boom generation that is now reaching retirement age has a double problem. First, many of its members didn’t save enough cash to support a comfortable retirement. Second, those many who did save enough could see it evaporate when we get into another bear market, which we certainly will at some point.

What can you do? Some suggestions.

First, whatever your age, save as much as you can. Stash it in your IRA, 401k, defined benefit plan, or whatever other tax-advantaged vehicles are available to you. Then save more outside them. If you look at your income and expenses and think “I just can’t do this,” think again. Start saving something, even if it’s $20 or $50 a month. Get in the habit and it will become easier.

(A personal note: If you have a small business, you should at a minimum have 401(k)s and business employment retirement plans. If you’re making a relatively good income, you should think about getting your own defined benefit plan. DB plans are not just for monster corporations. They can work extremely well for small, very closely held businesses. You can put away over $2 million of total contribution over your lifetime. If you start your plan and your age is 60, those can be some hefty annual contributions. Just another reason a good financial advisor can be useful.)

Second, invest in programs that give you at least a chance to dodge bear markets. Buy and hold works in theory, but not for most people because we are humans with emotions. We should recognize that and take steps to control it. As I continually say, we should invest in trading strategies and not buy-and-hold index funds in this environment. And of course, fixed income strategies like actual bonds, real estate, private credit, and so on.

Third, forget about retiring at 65 unless you are in truly dismal health (in which case, financing a long retirement is probably not your top worry). Keep working a few more years, even if you have to find a new career that better fits your circumstances. This will let your capital accumulate longer and you’ll get a higher Social Security benefit by waiting until 70 to start collecting.

Fourth, take care of your health. It will both reduce your medical expenses and keep you in shape so you can work and produce income longer. Further, staying physically active will keep you healthier. If that physical activity is involved in a job, that counts. There are studies that actually associate retirement with lower life and health spans. But gym time and a healthy diet are still important.

I’m personally doing all of the above, and I’m still concerned it won’t be enough. Laugh if you want to, but that concern for me is real. Relaxing is not in my personal makeup. I know a lot of people like me. I can only imagine the panic of those less fortunate and prepared. Their problems are yours and mine, too, because an economy with so many low-income elderly people has less opportunity for everyone.

While I think socialist and progressive policies are terrifying, they are spot-on when talking about wage and income disparity. Corporate profits are at their highest level ever percentage wise, yet labor is back to Great Depression levels. That is not healthy for our society. I am not going to start singing 1930s union songs, but this is a problem we must address. It is only going to get worse and the longer we wait, the more expensive the solution is going to be. Those of us with a libertarian bent may just have to suck it up and become part of the solution.

Mauldin, Blumenthal, Cucchiaro Podcast

In case you missed it: John Mauldin, Steve Cucchiaro and I recently recorded a podcast where we discussed the global economy and investment markets.

Steve Cucchiaro founded 3EDGE Asset Management and is one of the most successful ETF strategist in the business. In 1994, Steve founded Windward Investment Management and grew it from $75 million to nearly $20 billion in 2014. His firm was acquired by Charles Schwab in 2006. After helping Schwab integrate the business, Steve retired in 2014. But, a former Olympian and highly competitive person by nature, he couldn’t stay away. He put most of his former team back together to manage their money and now other institutions. We are thrilled 3EDGE is one of the strategists in the CMG Mauldin Smart Core Strategy.

Following is the link to the podcast. We hope you find it insightful and I believe you’ll enjoy the lightness and depth of the conversation. Make sure you listen until the very end. John was cute. He thought the recording was stopped and exclaimed, “Well, I think that went really well.” I think it did and hope you gain a few insights into what we see in the period immediately ahead.

Mauldin/Blumenthal/Cucchiaro Podcast

Trade Signals – The Trend Limps Higher

March 20, 2019

S&P 500 Index — 2,831

Notable this week:

No major changes or updates.

Modest improvement continues in the market indicators. The NASDAQ 200-day trend model has turned positive. However, the S&P 500 50-day over 200-day Moving Average is nearing a positive signal and the S&P 500 200-day MA rule is nearing a bullish signal. Both the Nasdaq and the S&P 500 have cleared their November highs and increases the odds of a test of all-time highs. For the S&P 500 Index, that level is at 2,941.

The Ned Davis Research CMG Large Cap Long/Flat model is back in an uptrend though it is important to note that the overall trend score is still below 60. The current reading is 59.42. What this is telling us is that there is not broad market breadth across the 24 sectors we measure. Fewer sectors are carrying the market higher. The strongest market environments have broad participation across sectors (or a score of greater than 70 in our process). This bears watching (no pun intended). You’ll see below that the Fixed Income Trade Signals remain bullish, suggesting risk on for bonds. Risk of global recession remains high. I believe we’ll look back in six months and see we were in fact in a global recession in Q1 2019. There is little risk of a U.S. recession in the next six months. Inflation risk remains low.

You’ll find the updated equity and fixed income charts below as well as the most recent recession watch charts. Thanks for reading. Have a great week.

Click here for this week’s Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note – It’s About Culture

“If we are all thinking alike, we are not thinking.” – Bill Walsh

Michael Lombardi took the stage at the Barron’s Independent Summit in Salt Lake City. On his right index finger was one of the largest rings I’ve ever seen. Loaded with diamonds, it’s the ring that was given to each player and staff of the New England Patriots for winning Super Bowl LI. I was expecting a sports story; however, Mike’s book, Gridiron Genius, is really about organizational culture.

Tom Peters, co-author of In Search of Excellence wrote, “…make no mistake; this is a very serious book… a full-fledged blueprint for organizational excellence… and it applies way beyond the gridiron.” I walked about with a number of ideas.

- To give you an example, Michael said there are three types of people in an organization. The first will do anything you want them to do. They are the individuals that show up early, never complain, work hard, think positively and do whatever it takes to improve themselves and the team. Competitive and driven to win.

- The second group is undecided… waiting and watching to see what you will do.

- The third group are individuals you can’t make them happy. The disrupters. Often full overconfident and self-centered. Their talent may be great but it’s all about them and you can’t make them happy.

Michael said, “Don’t pay attention to group three. Focus only on group one. Eliminate the threes, put all your attention on the ones and the twos will become ones.”

There were a number of other great points. He talked about four areas of leadership that creates culture. Winners are strong in three of them, great coaches are strong in four:

- Do your job

- Be attentive

- Speak for yourself

- Put the team first

Michael shared this slide – it took me back to that awesome moment in 1982:

I’ve been too late to fire in the past. The team is always watching. Fire the threes, focus on the ones. Like that advice.

Michael told a story about a time he was working for the Atlanta Falcons. The coach had organized a team bonding bowling event, and all were to meet at the team facilities and bus together to the bowling alley. A hot shot wide receiver who had just signed a big contract pulled up to the parking lot in his new Bentley. He told the coach there is no way he was getting on the bus. He’d be driving over in his Bentley. Instead of riding on the bus with the team, the coach jumped in Bentley and drove over with his star receiver. He picked the three. The team was watching. He should have focused on the ones. Name on the front is a lot more important than the name on the back.

There were a number of other great anecdotes from Michael. “If you want culture, define it.” “Who do we intend to be?” “If you find a rat in the mix, immediately confront it head on.” Bill Walsh’s quote, “If we are all thinking alike, we are not thinking.” Love that one. “Teach culture every single day.” “Your best player must set the tone for intolerance.” He cited Tom Brady as a selfless leader. Boy, do we all know that.

Michael said he believes there are just eight teams in the NFL that New England is competing against. They have great organizational leadership and culture. The others are in various degrees of disfunction and that usually begins with the owners.

There was much more… I’m really glad I sat in on that session. I always sit near the front so my ADD doesn’t go all over the place. I’m glad I did as Michael autographed a few books and it was easy be front in line. I’ve got book in hand and am looking forward to reading it on the flight home.

Selfies, I’m nearly 58 years old and taking selfies. Next is a shot with VanEck’s head of ETF strategies, Ed Lopez, just after our Barron’s presentation. If you are an advisor and would like a copy of the slide deck, please send me a email. Happy to share.

I’m mostly in Philadelphia the next few weeks then Mauldin and I are keynote speakers at a large advisor-partner event in Austin, Texas on April 3 and again in Dallas for a dinner presentation on April 4. It is an event for individual investors. There are a few seats available. If you would like to attend either event, you can sign up here. The Mauldin Strategic Investment Conference follows May 13-16 in Dallas. I hope to see you there.

Wishing you a fun-filled weekend!

Best regards,

Stephen B. Blumenthal

Executive Chairman & CIO