(NB: To improve readability, we are now linking references to media reports and articles directly in the text via hyperlinks. Footnoting will be reserved for documents to which we can’t link or to provide additional clarity on a topic.)

Q1 hedge fund letters, conference, scoops etc

Since early May, the trade tensions with China have morphed into a broader conflict. Not only is the U.S. trying to change the trade relationship with China, but it is also attempting to change Beijing’s industrial policy. The U.S. has been using two tracks to accomplish this goal. The first uses tariffs to narrow the U.S. trade deficit with China. The second involves various tools, including legal actions and regulations on foreign investment and technology transfers and sales, to affect Chinese industrial policy. The 2018 arrest of Meng Wanzhou, the chief financial officer of Huawei (002502, CNY 3.67), was the opening salvo in the second element of the administration’s policy toward China. Recent actions to limit the sale of technology to Chinese firms is another example to that effect.

China has started to retaliate. It has applied its own tariffs on U.S. exports, which has hurt the U.S. agricultural sector. In response to the technology policy, China is making an implied threat to prevent the export of rare earth porducts. In a highly publicized tour, Chairman Xi visited a magnet factory that uses rare earth elements in production, highlighting the potential threat. Using rare earths as a form of intimidation is nothing new; China embargoed rare earth metal exports to Japan in 2010 over a maritime dispute.

In this report, we will offer a brief outline of China’s structural economic problems and the U.S. response to provide context for the threatened rare earths embargo. Following this section, we will detail what rare earths are, their importance and discuss the rise of China’s dominance in this area. From there, we will offer our analysis of the likelihood that China follows through with this threat and the probability of its success if implemented. As always, we will conclude with market ramifications.

China’s Economic Problem

Since the industrial revolution, the world has seen a parade of high-growth/low-cost producers (HG/LC). In fact, this has become a commonly used development strategy for growing nations. The primary characteristic of the HG/LC nation is that growth is dominated by investment which builds the industrial infrastructure of the country. There are two different ways to fund this investment. The first is through direct foreign investment; the HG/LC nation attracts foreign investment and often runs a trade deficit when doing so. The second is through export promotion. In this model, the developing nation purposely constrains consumption through an undervalued exchange rate, capital controls and consumption taxes. These policies tend to generate high levels of household saving that provide the liquidity for investment.

The U.S. mostly followed the first model, while most other nations, especially after WWII, have leaned toward the second model. The HG/LC nation tends to have robust economic growth during its development, but, over time, a critical mass of investment is reached and usually exceeded.1 Once this happens, the HG/LC nation has excess capacity and must take steps to resolve it. In the late stages of this excess capacity, the HG/LC nation becomes a major exporter, running large trade surpluses that upset relations with major trading partners. Eventually, these trading partners retaliate against the HG/LC with trade impediments. Deteriorating trade relations are usually a signal that the HG/LC needs to resolve its excess capacity problem (which, in the export-promotion model, is usually accompanied with an excessive debt problem).

Historically, there have been four avenues of resolution:

- Revaluation: The excess investment capital needs to be written down to a level where a new investor can purchase the devalued asset and make it profitable. This can either be done quickly, which is what the U.S. did during the Great Depression, or slowly, as Japan has been doing for the past three

- Imperialism: The HG/LC acquires colonies that it can use to dump its excess production. The colonies, under control of the “mother country,” are forced to accept the imports thus undermining their domestic

- Value chain adjustment: The HG/LC can move from low-value production to high-value production. As a result, the excess capacity is transformed into viable new capacity.

- Mass mobilization war: The HG/LC gets involved in a large-scale war that (a) utilizes the excess capacity for the production of war materials, (b) uses that excess capacity to dominate the postwar world, or (c) sees the capacity destroyed by its enemies.

Needless to say, these resolutions aren’t easy. Every nation that has found itself transitioning from HG/LC status to that of a developed economy has been forced to make these adjustments. Of the four options, #3 is the most attractive but usually requires the world to either absorb at least some of that production as new high-valued exports or the other developed nations lose the HG/LC as an export market for these goods. The other three solutions cause even greater turmoil.

China now finds itself in this predicament and is trying resolutions #2 and #3. The “one belt, one road” project of foreign infrastructure development is a modern form of 18th century imperialism. The nations that participate have found themselves with projects that have incurred high debt and were often constructed with Chinese labor. Once built, the facilities then become conduits for Chinese exports. China is also attempting to climb the value chain through its “China 2025” industrial policy. This program is designed to make China the dominant player in several critical markets, including 5G and artificial intelligence.

The U.S. views China as a strategic competitor and is therefore working to prevent China from using methods #2 and #3. It is starting to take steps to undermine the belt and road project and the recent restrictions on technology exports will harm China’s attempt at #3. American actions, if successful, will force either outcome #4, a war with the U.S., or #1, either a Great Depression-style economic calamity or a repeat of Japan since 1990. Needless to say, China wants to avoid both war and revaluation. At the same time, Chinese leaders will tend to resent the actions of foreign nations to constrain the HG/LC economic model. Often, the leaders of the HG/LC economy view their country’s growth as the result of unique cultural or societal characteristics, not just a happenstance of development. Consequently, there is a tendency for them to view anger from foreign nations over the trade surplus as an intrusion on the “special” HG/LC nation’s sovereignty. This anger is often what is behind imperialism and war as resolution strategies.

China now finds itself as a target of U.S. policy. The U.S. does not necessarily want to prevent the rise of China but does want it to fall in line with American hegemony. In other words, China must not threaten the American military’s free movement around China and should acquiesce to the U.S. dollar’s reserve currency status and the U.S.- structured multinational trade system. China doesn’t want to completely accept U.S. hegemony. Instead, it has shown a pattern where it accepts the parts it likes (e.g., global security, U.S. open trade) and rejects what it doesn’t (U.S. power projection into the South China Sea, in particular, and the area, in general, the use of financial sanctions and interference on trade and technology transfer). The U.S. has addressed China’s behavior through tariffs and technology restrictions, thus China wants to retaliate. It has cut agricultural imports from the U.S. and is looking to expand tariffs. Its threat to cut rare earth exports is part of this retaliation.

Rare Earths: A Primer

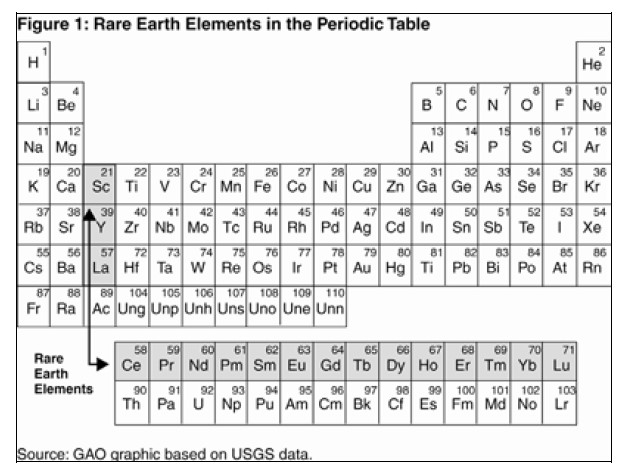

Rare earth elements (REE) are a group of 17 chemically similar metallic elements: lanthanum, cerium, praseodymium, neodymium, promethium, samarium, europium, gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium, lutetium, scandium and yttrium. They are shown on the following periodic table.

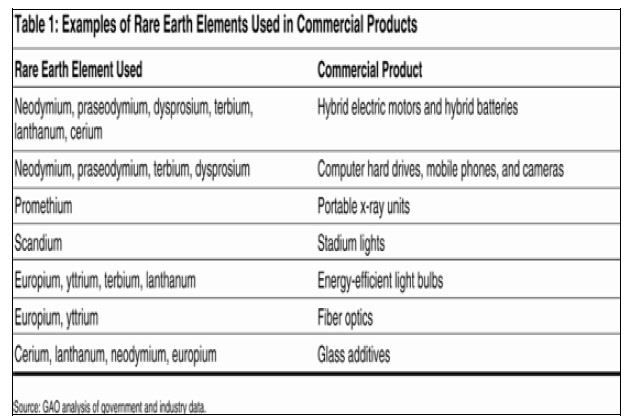

The table below shows examples of various uses of rare earths.

REE and rare earth metals (REM) are used heavily in the production of specialized magnets that are used in hybrid and electric cars and in wind turbines to generate electricity. Cordless power tools use these elements, as do earphones, smartphones, and energy efficient light bulbs. These materials have a number of military applications as well. They are used in jet aircraft engines, missile guidance systems, electronic countermeasure systems, including underwater mine detection and anti-missile systems, and in satellite power and communication systems. High technology warfare would be nearly impossible without these materials.

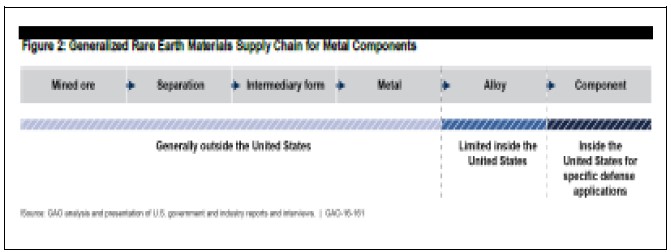

Producing REM and REE requires five basic steps. The ores must be mined, separated, refined, formed and manufactured. In general, the processes of mining and separating these materials are fraught with environmental dangers. In nature, REE coexist with thorium, a radioactive metal. The waste from mining and separating is often radioactive and the water used in processing becomes dangerously polluted.

Chinese officials estimate that every ton of REE produced creates 2,000 tons of mine tailings, which are often toxic and radioactive.

Industry Structure

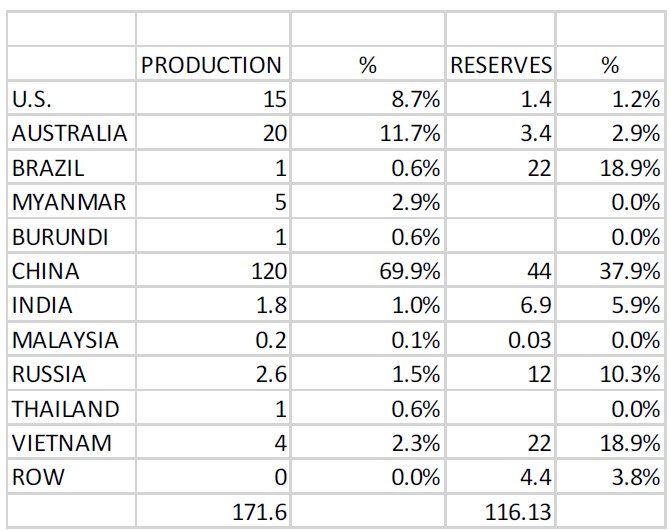

China dominates all phases of REE and REM.

However, there is a significant difference between reserves and production. Nearly all processing and refining of rare earths are done outside the U.S. and most are in China.

In the wake of the REE crisis in 2010, the U.S. reopened its long dormant mine at Mountain Pass, CA. The ore it currently mines is shipped to China for processing and under a 10% retaliatory tariff. The U.S. lacks the capacity to refine and form these metals.

The United States was essentially self- sufficient in REE and REM from 1949 until 1985. In 1949, U.S. miners discovered massive deposits of REE in Mountain Pass, CA. The U.S. performed all the stages of REM processing during the period of 1965-85. However, environmental regulations and falling prices of REE ores (due to massive Chinese production) eventually ended U.S. production. China has forced technology manufacturers that need the various products produced from rare earths to move entire production lines to China, effectively creating a vertically integrated supply chain within China.

Is the Threat Viable?

Vertical integration gives China power in this area. As noted above, the mining, processing and production of REE and REM are mostly in China now. However, there are three problems with using this power as a threat.

- The expansion of capacity means that China must export REE and REM to make the capacity profitable. Restricting exports as a weapon in trade and technology negotiations runs the risk of creating unprofitable excess capacity within China.

- The very threat from Chinese dominance in this area will prompt a reaction from other nations. Although Western nations will struggle to deal with the environmental hazards from REE and REM production, clearly the U.S. previously made these materials and can rebuild its capacity. Obviously, this will take some time and U.S. capacity won’t be as cost effective as in China, but given how critical some of these metals are in defense applications, a ready market with a price-insensitive buyer does exist.

- China can’t complete the threat because its currency isn’t widely used and its financial system is closed. It is likely that if the U.S. is excluded from buying REM it would be able to secure the item from another country. For example, if Luxembourg bought the item and re- exported it to the U.S., China would be hard-pressed to prevent that from occurring. China could deploy a “whack-a-mole” strategy by cutting off other nations that engage in re-exporting practices, but that is time-consuming and there may be some nations China might not want to anger and would therefore allow the activity to occur. Unlike China, when the U.S. finds itself in such a situation it can deny access to the dollar and the U.S. financial system as a secondary impediment to cheating. That factor has proven to be very effective. China doesn’t have that capability, so its ability to completely secure the export chain is compromised.

Overall, restricting exports of REE and REM carries risks to China. Being seen as an unreliable supplier will prompt other nations to rebuild capacity, and China lacks the capability to completely secure the export chain. As a result, we suspect China will be reluctant to fully deploy this threat.

Ramifications

The most obvious beneficiaries of China’s threat to restrict the exports of REE and REM will be firms that participate in the rebuilding of the supply chain. The miners themselves will probably also benefit, but to a lesser degree than companies that promise to build refining and smelting capacity. We would also expect aggressive stockpiling to occur which may benefit those involved in the acquisition and warehousing of these materials.

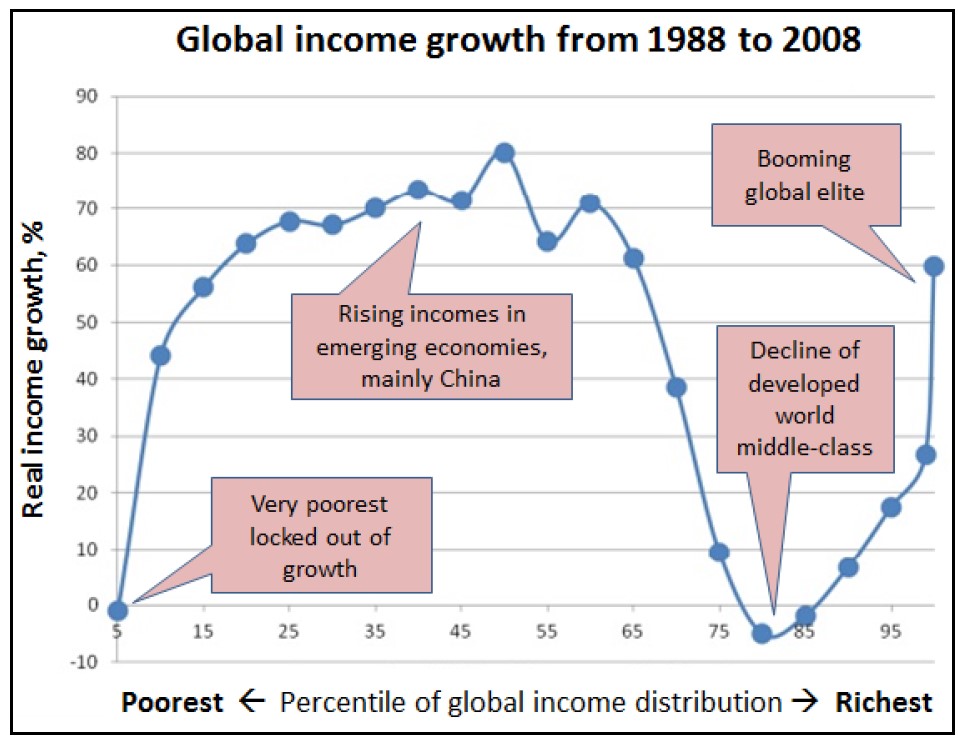

The bigger issue is that the potential restrictions of REE and REM are part of the trend against globalization. The famous “elephant chart” shown below illustrates a factor that has led to populism in the West and reflects this deglobalization trend.

(Source: Bruno Milanovic)

Essentially, the rise of the emerging world from 1988 to 2008 was at the expense of the Western working class; only those at the very top of the income scale have benefited from globalization.

Geopolitics and national security are other elements of deglobalization. Long global supply chains rely on a hegemon providing a stable reserve currency and world security. If that arrangement begins to break down, there is an incentive to shorten supply chains and create redundancies in production. In other words, optimization is a virtue under conditions of stability but a vice during periods of instability. It is optimal to have China dominate the REE and REM supply chain if the Chinese are willing to operate within the American-dominated trade, financial and security systems. However, it would be suboptimal to have China dominate this industry if it is unwilling to submit to U.S. hegemony. Rare earths are not the only industry that is, or will be, facing this problem. Just-in-time inventory logistics require stability and certainty. We are probably moving into a world where optimization = unnecessary risk. That is a world where profit margins will decline. Overall, this doesn’t mean that some companies and sectors won’t do well, but falling profit margins will make broad equity gains challenging.

Bill O’Grady June 3, 2019