Saber Investment Fund commentary for the third quarter ended September 30, 2019.

[dalio]

Q3 2019 hedge fund letters, conferences and more

Dear Investment Partner,

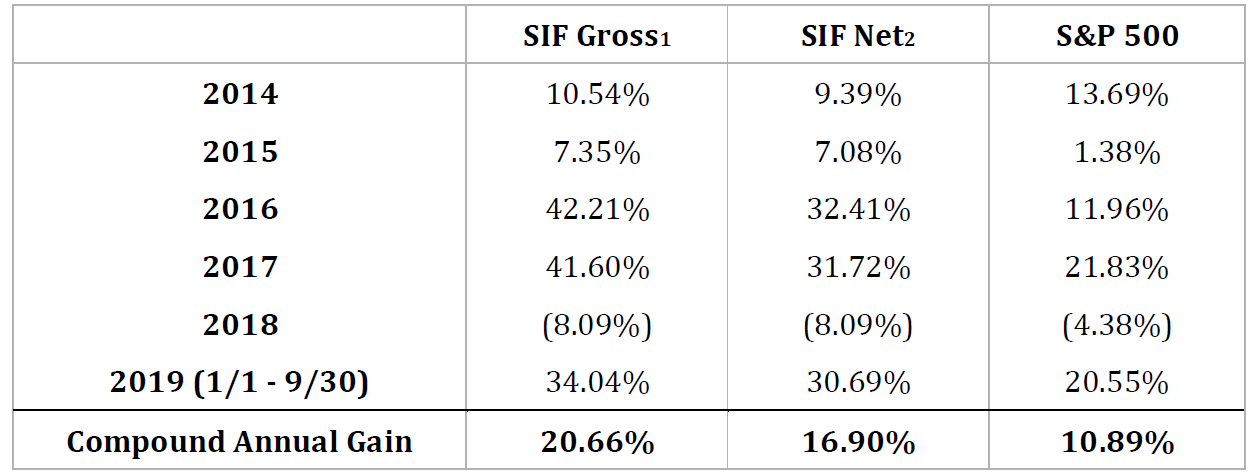

For the first three quarters of 2019, Saber Investment Fund gained 34.04% before the General Partner’s performance allocation, which resulted in a net gain of 30.69% for limited partners.

[1]Gross return before performance allocation

[2]Net return assumes investment in the fund at inception with no additional contributions/withdrawals, and assumes 0% management fee and a 25% performance fee over a 6% compounding hurdle

I place little to no emphasis on short-term results, but as I said in last year’s end of year letter when we finished the year down, no manager is immune to disappointment when short-term performance is poor. Conversely, it’s always more fun to report good results when they come in. After all, my parents and the in-laws (not to mention my wife) have a sizable amount of their money parked at Saber headquarters. Thus, the Thanksgiving dinner table is always better when results are good, but in between my first and second helping of pumpkin pie next month, I’ll remind my family that the focus should always be on our long-term results.

You should have received your 9/30/19 account statement from Liccar & Co., which has your capital account’s value as well as your individual net return. Note that your individual return may vary depending on when you entered the fund and the timing of any new contributions.

Worth noting: Most investors who entered the fund last year had a loss at year end, and thus will have a net return so far in 2019 that is higher than partners who entered the fund this year. This is because you don’t pay any fees until a) all your previous losses are recouped, and b) your capital grows above the 6% hurdle.

As a reminder, the 6% hurdle is not just a fixed 6% hurdle rate: it compounds annually, meaning after a losing year, the 6% hurdle is now a 12.36% hurdle in year 2 (6% compounded).

Bottom line: If your money is not growing by more than 6% annually, then you’re not paying a dime in fees.

Portfolio

There were just minor changes to the portfolio since my mid-year update. We did take advantage of the August downturn in stocks to buy more Wells Fargo, and we also bought some Bank of America, although it is a smaller position than WFC. Both companies continue to gush cash that is used almost exclusively for buybacks and dividends, both offer a double digit earnings yield, and both offered around a 15% total “buyback + dividend yield” at the prices we paid. I summarized my thesis on the banks in my last letter and also in this writeup on WFC.

It’s worth noting that when the fund has inflows, it effectively reduces the size of each position as a percentage of the fund’s NAV, unless we use those funds to buy more of everything we own. I am always looking to allocate each dollar to where I think the best risk reward is at that moment, and so I chose not to invest incoming cash into some of our stocks that have appreciated closer to fair value, which effectively trimmed those positions (without paying tax!). We did use incoming funds to buy what I thought was better value, and the portfolio will continue evolve as stock prices change and opportunities shift.

More Comments on Edge

I often get asked the question, “what is your edge“? The question comes up so often, and I feel like there is such a misunderstanding around what edge is and where it exists today that I continually feel compelled to write about it in these letters. Institutional investors seem especially interested in this question, and the edge that they are almost always looking for is some form of informational edge or insight that the rest of the market isn’t aware of. The problem is that this edge doesn’t exist anymore. Everyone understands that there is no info edge in Facebook or Apple. But there isn’t any info edge in smaller stocks either, at least not in a meaningful way that can be reliably utilized.

I’ve observed over the years that whatever information an investor believes to be unique is almost always understood by many other market participants, and thus is not valuable. The mispricing is not in the stock itself, but in the investor’s own perception of the value of information: it’s worth far less than they believe it is. Information is now a commodity, and like the unit price of computing power that provides it, the value has steadily fallen as the supply and access to it has skyrocketed.

Black Edge

I read a great book called Black Edge, which describes the trading strategy of Steve Cohen and SAC Capital. The traders at SAC categorized edge in three ways:

- White Edge:this was public information that wasn’t worth much to them because anyone could find it

- Gray Edge:this was valuable non-public information where it was uncertain if it was okay or illegal to use

- Black Edge:Clearly illegal inside information

The traders would hunt for gray edge all the time, and some engaged in black edge.The firm spent hundreds of millions of dollars they collectively spent on research was all designed to figure out if a stock was going to go up or down a few dollars in a short period of time, usually after an earnings announcement or some other significant event.These traders were moving billions of dollars around with no concern for what the company’s long-term prospects were, other than how those prospects might be viewed by other traders in the upcoming days.

Everything was purely focused on how the stock price would act in the very short term. It’s how the firm operated, and it’s how portfolio managers and analysts earned their bonuses. Everything depended on the short-term, and as a result, investment decisions were made that had nothing to do with long-term value and everything to do with short-term stock price.

This worked for SAC. Even before they committed a crime, they were very successful at betting on short-term moves. But reading about their strategy is refreshing because it solidifies two things that I already am very convinced of:

First, I have no informational edge, I don’t think anyone else has one either. But I don’t think you need one. This is fortunate, because it’s a game that is very hard to win. Reading about SAC’s resources reinforces that belief. It’s similar to how Ray Dalio advises people to diversify and invest in various asset classes and hold for the long-term, because “we are spending hundreds of millions of dollars each year to try and figure this game out, we’ve been doing this for 40 years, and we still don’t know if we’re going to win.” I’m not interested in trying to compete in a game that is that difficult to win.

Second, the investor who is willing to look out three or four years will have a lasting edge because the more money that gets allocated for reasons other than a security’s long-term value, the more likely it is that the security’s price becomes disconnected from that long-term value. In short, thedeterioration of the info edge has actuallyincreased the size of the “time horizon” edge.

This is a different kind of edge. The traders at SAC weren’t even discussing this type of edge. It wasn’t even on their radar, because they had no interest in the long game. But this is the reason that the time horizon edge exists, and I think has only gotten stronger as markets have become faster and the information has become more easily available. In fact, the liquidity that is provided by short-term traders adds to the volatility of stock prices, which creates more opportunities for long-term investors.

Price of Time Horizon Edge

Note that the time horizon edge isn’t a magic bullet. There is a reason why investors don’t want to own certain stocks at certain times. No one wanted to own Bank of America in 2016 because they were worried about recessionary risks and low oil prices and what might happen to the stock if those risks materialized. It was priced at around 7 times normal earning power, but investors thought (probably accurately) that it would fall more if the economy slipped. No one wants to own a stock that they think will go down in the next 6 months, even if they think in three years it will be worth much more.

The time horizon edge could be summed up this way: the price of gaining this edge is the volatility that could occur in the near term. You have to be willing to accept the possibility that your stock will go down before it goes up. Very few investors are willing to pay that price, which is why even large cap stocks can become disconnected from their long term fair values:

Stock prices move much more than true values do even in the largest stocks, which by definition causes mispricing at times. This isn’t due to a lack of information, it’s simply good old-fashioned human nature, and unlike the price of semiconductors or the value of information, human behavior is not going to change. The biggest edge is in understanding this simple concept, and then being prepared to capitalize on it when it’s appropriate.

This is Saber’s game plan, and I will do my best to implement it.

Summary

As a reminder, our fund can accept new contributions once a month. If at any point you would like to add to your investment, please contact me or Maureen Murphy at mmurphy@liccar.com(the fund’s administrator). Maureen and the rest of the team at Liccar & Company have done a great job handling numerous back office tasks for us, and they are always available should you have questions regarding your account statements, or anything related.

As always, I want to thank you for your partnership. Your trust and confidence in Saber Capital as your investment manager is what makes it possible for me to do what I love for a living, and I’m very grateful for that. It’s a privilege to be your partner.

Best Wishes,

John Huber

Managing Partner

Saber Capital Management, LLC