In this edition I take you through 5 charts which outline how a possible reassessment of the global macro/fundamental outlook is changing among investors. From a peak in the “bull market in pessimism” to a reflation reassessment, there’s signs of change afoot here, and I have a feeling more and more people are going to start talking about this soon.

Q4 hedge fund letters, conference, scoops etc

Firstly, for context, in the Sentiment Snapshot series I look at some of the charts and data from the weekly survey on Twitter, which asks respondents to indicate whether they are bullish or bearish for primarily technical or fundamental rationale. I also add a few other charts from time to time when it helps explore a certain theme.

The key takeaways from the weekly sentiment snapshot are:

- Equity fundamentals sentiment rebounded on the week, technicals sentiment continues to trend up.

- Yet, bond fundamentals sentiment seems to point to even greater pessimism on the outlook.

- A possible peak in pessimism is underway, and it mirrors the rebound in reflation trade positioning.

- The China PMI/copper chart presents some real time evidence that there may be something to this potential transition in fundamentals sentiment.

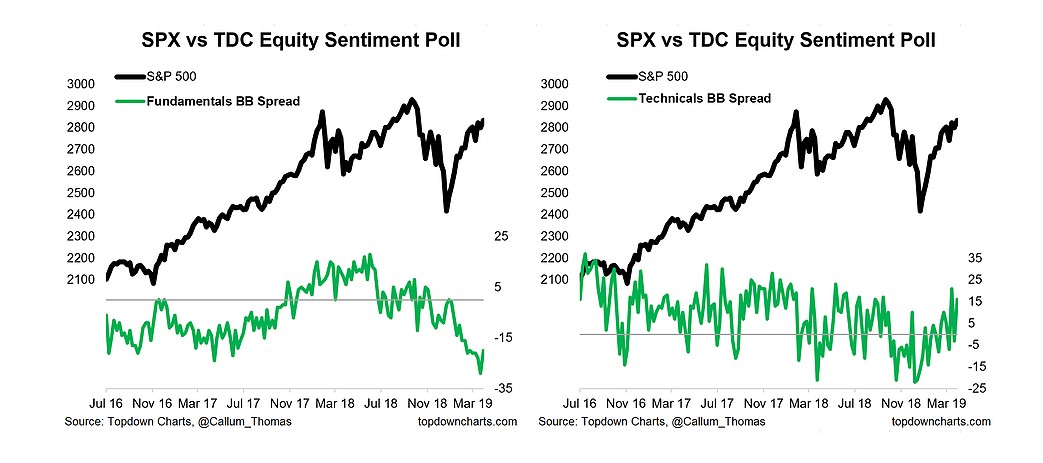

1. Fundamentals vs Technicals Sentiment: As I was going through the results of the latest weekly survey, I stopped to reflect on these two charts. The first thing that struck me was the obvious bounce in the fundamentals bull/bear spread, but the second thing is that almost missable yet discernible uptrend in technicals net-bulls.

Basically, phase 1 of the rebound is that sort of reluctant bull phase: where sentiment is dragged higher by prices, but only expressed in technicals sentiment, while participants remain bearish on fundamentals. A possible phase 2 is where participants stay bullish on technicals, but begin to capitulate on the bearish fundamentals view…

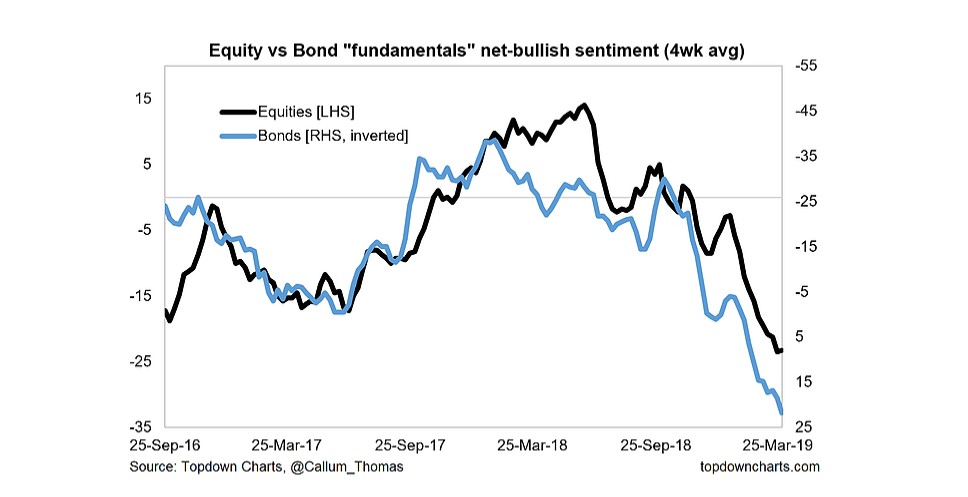

2. Stocks vs Bonds Fundamentals Sentiment: Yet looking at the 4-week average for equity fundamentals sentiment, it’s slightly less discernible on this chart, and reminiscent of some of the previous false dawns. It’s also standing in contrast to the increasing optimism of bond investors on the fundamentals outlook… which given bonds tend to see the world upside down from equities, means bond investors remain as pessimistic as ever on the macro outlook.

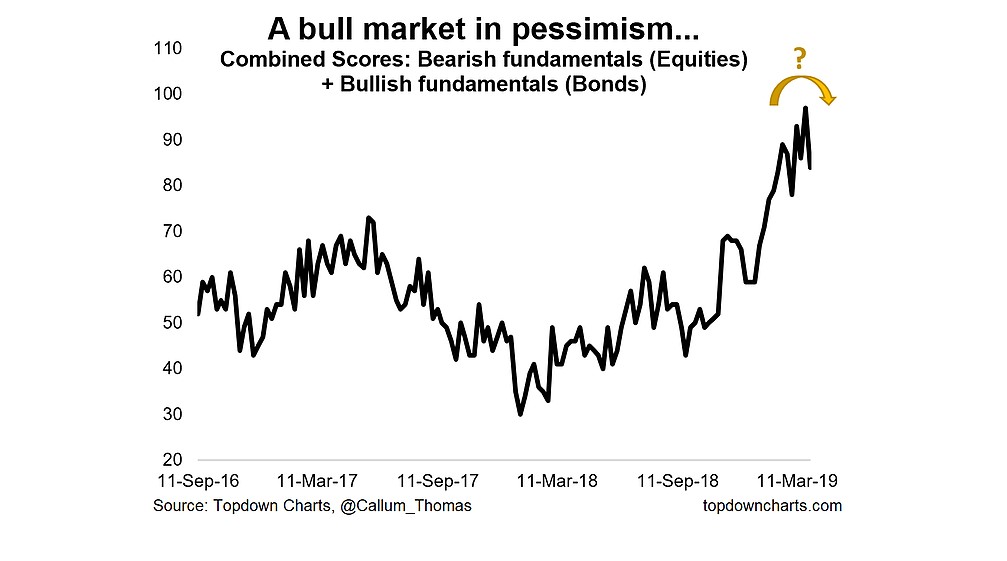

3. The “bull market in pessimism” – is it near an end? But carrying this theme further, I show again this chart from last week, where I mused about a “bull market in pessimism” to describe the pervasive and progressively bearish mood that seemed to permeate the market. This in my view is true whether you look at this or other surveys and a little anecdotal evidence.

This time I’ve inserted a handy little yellow arrow to imply that it looks like we might have seen a peak in this indicator (is it OK if I ask if we’re about to see a bear market in pessimism??). Again, I highlight that the low point in this indicator last year was when the global PMIs peaked.

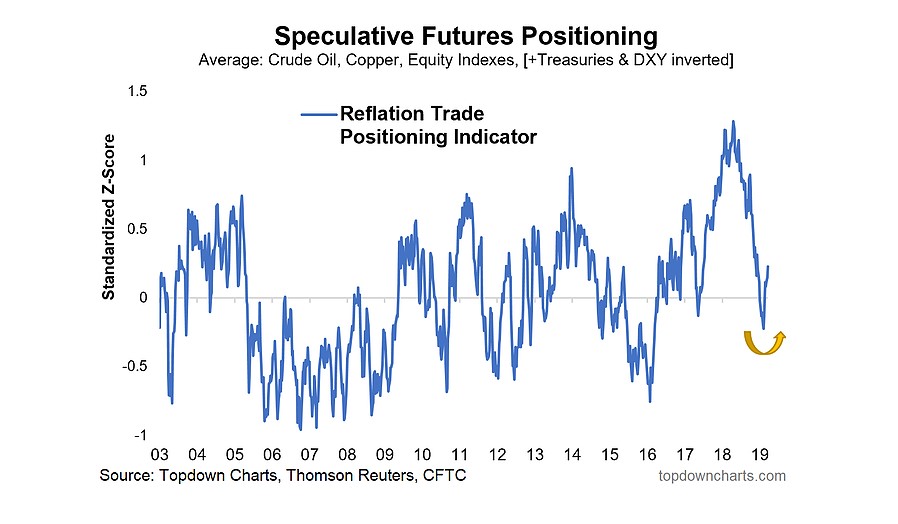

4. The Reflatometer Rebound: Another old favorite of mine, the Reflatometerhas rebounded off the lows. This comes after a complete and total reset of the extreme optimism that had taken hold around late 2017 to early 2018. Given the components of this indicator (crude oil, copper, equities, and USD + treasuries inverted), you would say that this represents a clear reassessment of the fundamental/macro outlook… in other words, the capitulation has run its course.

So we’re now faced with a set of charts that seem to argue for an imminent change (upgrade) in the macro outlook/fundamentals sentiment. If this thesis proves accurate it will be pivotal in a possible next leg up in risk assets (i.e. stocks, commodities, EM).

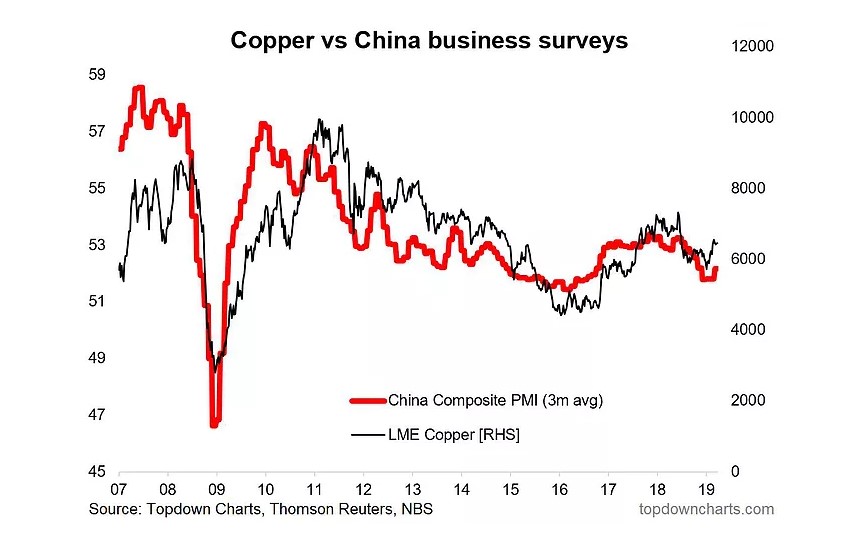

5. China PMI vs Copper Price: So it’s only fitting to end this week’s sentiment snapshot with a quick look at a key piece of global macro data that came out over the weekend; the China PMI. Now it is true that there is likely to be some element of Chinese New Year holiday distortion (Feb PMI may have been understated, and thus March may be overstated), but what’s interesting is how the rebound in the PMIs maps to the price action in Copper.

One thing that we can probably agree on is that at least for now, the Chinese PMIs have stopped getting worse, and that’s typically the first step on the road to recovery/reacceleration.

Last Word: The 3 Transitory T’s

As I mentioned on Twitter this morning, the softening of the macro/earnings pulse globally has been impacted or driven by 3 things:

- Tax cut washout

- Trade war (tariffs + uncertainties)

- Tightening monetary policy (globally + esp. US)

The tax cut washout is transitory (the boost was transitory and the negative impact on YoY growth figures from a high base comparator is also transitory). The trade war negative impact is arguably one-off (certainly at least the initial imposition of tariffs, and the uncertainty effects were probably at their worse last year, with a certain numbness now in place). Tightening is done with for now as a global monetary policy pivot is underway (fed stopping QT, shadow rates falling, dovish talk from ECB and others). So with a passing of these 3 transitory T’s, maybe it is indeed back to business.

Did you know we offer a world-class institutional multi-asset investment research service? Why not take a free trial for an extra level of insight and service…

Article by Top Down Charts