Does Social Media Trump News? The Relative Importance of Social Media and News Based Sentiment for Market Timing

Q2 hedge fund letters, conference, scoops etc

- Stan Beckers

- Journal of Portfolio Management, Winter 2019

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

With a growing availability of filtered (news) and unfiltered (social media) information, the author investigates the following question:

- Do news or social media contain any information that is of relevance for investment decision making and if so are the two sources are complementary or overlapping?

What are the Academic Insights?

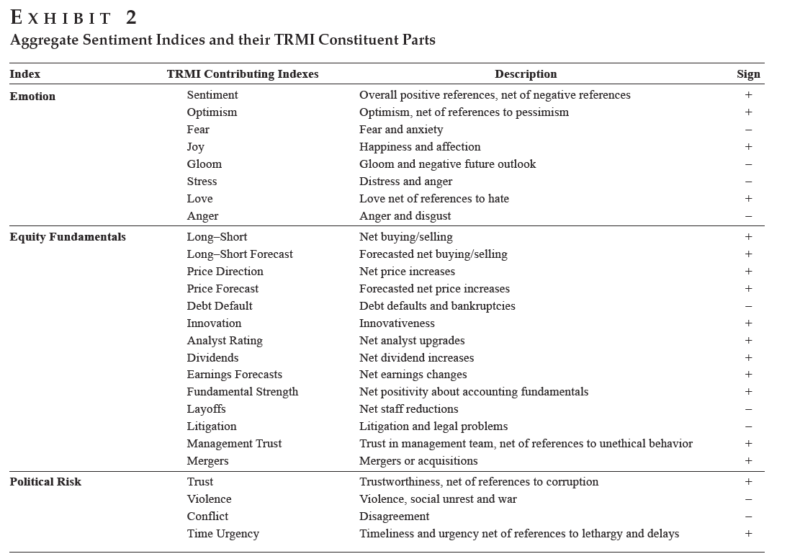

By using an extensive sample of directly comparable news- and social media–based sentiment variables ( based on Thomson Reuters Market Psych Indices- TRMI) the author attempts to infer any predictive relationship with monthly global equity market returns. The sample covers 1998-2017 data and the author finds:

- News-based variables appear to have on average healthy and promising correlations with future returns. In contrast, social media-based signals have patchy predictive power and tend to be dominated by the corresponding news-based variables.

- When testing an investing strategy, the emotion and fundamental equity social media-based signals are dominated by their news counterparts.(1)

- The authors find a statistically significant distraction effect.

Why does it matter?

This study compares news based sentiment with social media sentiment. Based on a 20-year history of both social media and news, the author infers that the social media–based sentiment is mostly already captured by that reflected in news-based sources. Despite the proliferation of social media over the study period, the investment importance of the embedded sentiment does not appear to improve through time: the noisy nature of social media chatter does not dissipate as the number of sources increases.

One thing to keep in mind: this study focused on monthly data. It is possible that social media sentiment contains information over shorter investment horizons.

The Most Important Chart from the Paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

The author uses a broad set of news and social media sources to infer sentiment about the global equity market. The author evaluates the contemporaneous and lagged relationship between the two sources and establishes how they inform each other. This study finds that lagged social media and news can help forecast next month’s global stock market return. However, adding social media information to news-based sources does on average not improve the results of a market timing investment strategy. Overall, the news-based equity fundamentals sentiment is the more consistent and reliable source for monthly timing of the MSCI World Index.

- The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

- Join thousands of other readers and subscribe to our blog.

- This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

References

- If the monthly percentage change in any sentiment variable exceeds 10% (in absolute value), it is assumed to invest 130% (70%) in next month’s index. If the change is less than ±10%, it goes just 100% long the market

The post “Social Media, News Based Sentiment, and Market Timing” appeared first on Alpha Architect.