Spruce Point Capital Management is pleased to issue a “Strong Sell” opinion on Aerojet Rocketdyne Holdings, Inc (NYSE: AJRD).

Q1 hedge fund letters, conference, scoops etc

Highlights

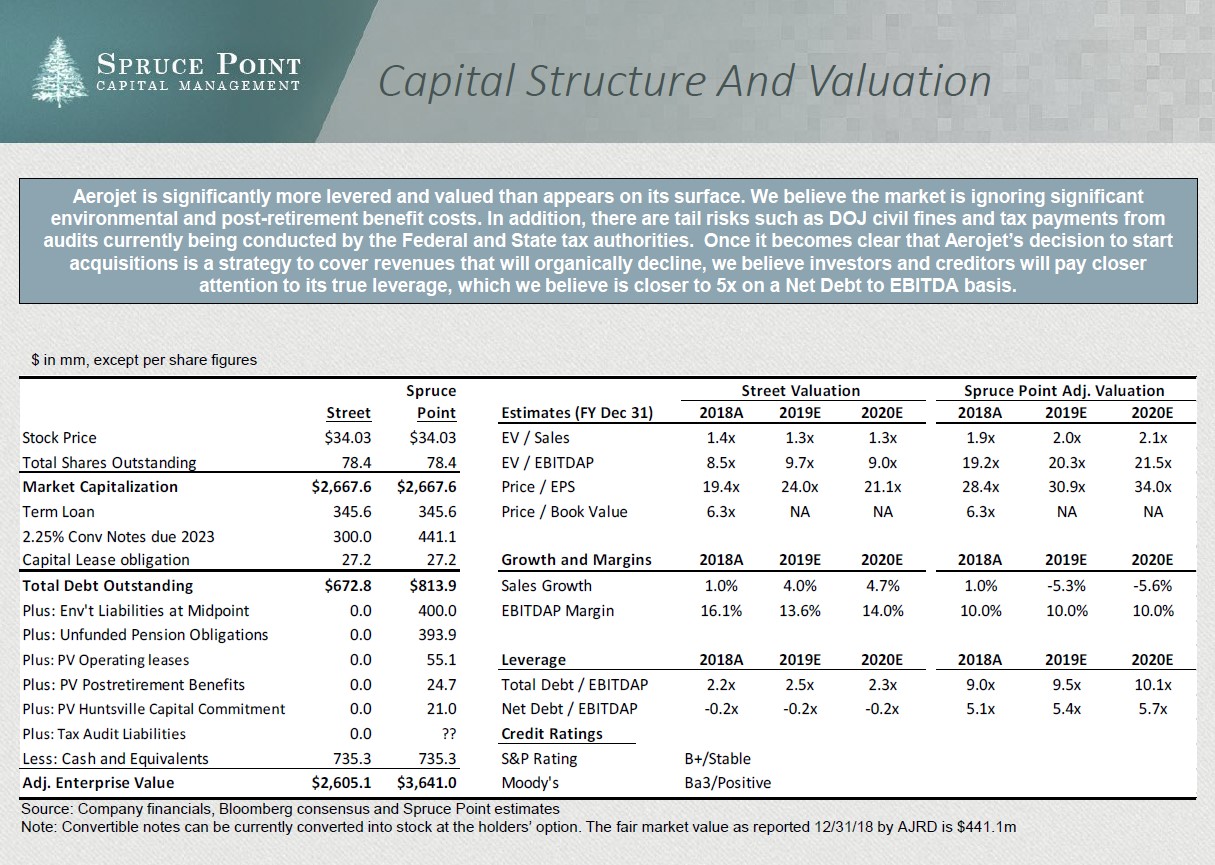

- In our opinion, Aerojet Rocketdyne (NYSE: AJRD) – formerly Gencorp (NYSE: GY) – is facing fundamental pressures, masked by complicated and aggressive accounting, which gives investors a potentially misleading impression of stability and growth. While holding no conference calls, and having only four analysts cover the stock, we believe the market is fundamentally ignoring ~$900M of liabilities associated with the business, making the Company 5x more levered than it appears and its valuation “cheap”. Furthermore, analysts blindly pencil in 4% revenue growth in the next two years, despite hundreds of millions of dollars in revenue programs that are disappearing. We see 40% – 60% downside once investors piece the puzzle together.

- Aerojet’s primary rocket propulsion business has historically benefited from high barriers to entry, oligopolistic pricing and favorable cost-reimbursable contracts. In our opinion, these dynamics appear to have enabled the Company to win business and protect margins, despite many claims it lacks a culture of innovation

- These dynamics have shifted in recent years with the emergence of disruptive low-cost competitors driven by lionized CEOs (Blue Origin / Bezos and SpaceX / Musk ), and the impact of the Northrop’s Orbital ATK acquisition on AJRD’s missile business

- The winding down of various platforms (AJ-60 + RS-J8) and failure of AR1 to low cost competitor Blue Origin’s BE-4 engine for the Vulcan Rocket. We believe the loss to Blue Origin was the death blow to Aerojet by losing ULA, its only customer in space launch. ULA, a material 17% customer, is expecting to coming under pressure: earnings are forecasted to be down 47% in 2019. Spruce Point estimates these losses eliminate $300m of expected revenues in the near and long-term

- Revenues from RS-25 for the SLS program (14% of 2018 revenues), are set to decline from the Sept 2018 completion of a $2.0bn contract, and the run-off from the 2015 $1.5bn contract to be completed by 2023. Longer-term challenges remain with NASA’s over-budget Space Launch Systems (SLS) program dubbed the “rocket to nowhere”, and a recent change of tone at NASA suggest it is taking steps to find cheaper commercial alternatives to the RS-25.

- In 2018, Aerojet benefitted from boosts in missile orders from key programs which are set to decline by 5% and 11% in 2019/2020, respectively, according to the recent March 2019 DoD budget request. We estimate that Aerojet’s revenues increased $117m in 2018 from the growth in just two key programs: Standard Missile and THAAD. These two key programs are budgeted to decline by 2% and 35% in 2019 and 2020, respectively

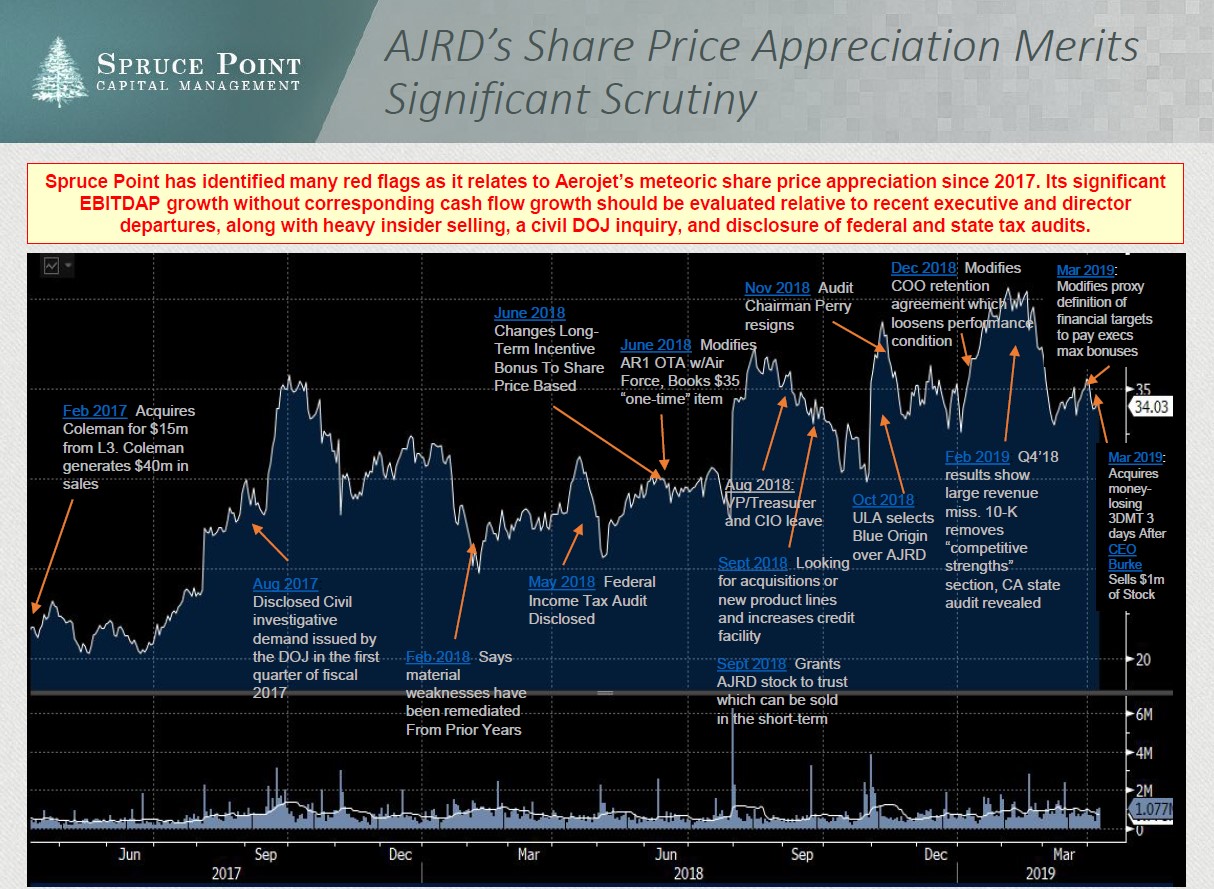

- Management And The Board Have Little At Risk Owning Just 3.0% Of The Company (1.9% ex: Chairman Lichtenstein’s Ownership). Years Ago, The Employee Savings Plan Was A Material Owner >10%, Now It’s Effectively 0%. Short-Term Incentive Bonus Definitions Becoming Much More Subjective, Conveniently Allowing The Board To Lavish Management With Credit For Maximum Cash Compensation

- Upon Hiring, The CFO’s Bio Claimed He Was A CPA, Yet His Bio Now States He “Completed Exam Requirements”. General McPeak was the Lead Director at Miller Energy Resources (NYSE: MILL), a bona-fide accounting fraud that went to zero. The SEC charged management with securities violations and even fined the auditor. Perry was CFO and Treasurer of United Industrial Corp during a period the SEC blasted it for fraud concerning foreign corruption and stated the Company “lacked meaningful controls to prevent illicit payments.

- By applying a discounted multiple range to our adjusted enterprise value and financial results, we derive a price target of $13.00 – $20.00 (40% – 60% downside) including entitled land value. Follow the money: Many long-term owners are consistently selling stock and reducing ownership. Aside from passive investor Vanguard, Aerojet has attracted only one new fundamental investor of size in recent years

Executive Summary

Spruce Point Believes Aerojet Rocketdyne(NYSE: AJRD) Is A “Strong Sell” And Sees 40% -60% Downside Risk ($13 -$20 Per Share)

In our opinion, Aerojet Rocketdyne (NYSE: AJRD) –formerly Gencorp (NYSE: GY) –is facing fundamental pressures, masked by complicated and aggressive accounting, which gives investors a potentially misleading impression of stability and growth. While holding no conference calls, and having only four analysts cover the stock, we believe the market is fundamentally ignoring ~$900M of liabilities associated with the business, making the Company 5x more levered than it appears and its valuation “cheap”. Furthermore, analysts blindly pencil in 4% revenue growth in the next two years, despite hundreds of millions of dollars in revenue programs that are disappearing. We see 40% -60% downside once investors piece the puzzle together.

Aerojet’s Changing Competitive Landscape Has Revealed Complacency And Caused Fundamental Strain

- Aerojet’s primary rocket propulsion business has historically benefited from high barriers to entry, oligopolistic pricing and favorable cost-reimbursable contracts. In our opinion, these dynamics appear to have enabled the Company to win business and protect margins, despite many claims it lacks a culture of innovation

- These dynamics have shifted in recent years with the emergence of disruptive low-cost competitors driven by lionized CEOs (Blue Origin / Bezos and SpaceX / Musk ), and the impact of the Northrop’s Orbital ATK acquisition on AJRD’s missile business

- We believe these shifting competitive dynamics have in-part contributed to the following revenue pressures:

- The winding down of various platforms (AJ-60 + RS-J8) and failure of AR1 to low cost competitor Blue Origin’s BE-4 engine for the Vulcan Rocket. We believe the loss to Blue Origin was the death blow to Aerojet by losing ULA, its only customer in space launch

- ULA, a material 17% customer, is expecting to coming under pressure: earnings are forecasted to be down 47% in 2019

- Spruce Point estimates these losses eliminate $300m of expected revenues in the near and long-term

- The winding down of various platforms (AJ-60 + RS-J8) and failure of AR1 to low cost competitor Blue Origin’s BE-4 engine for the Vulcan Rocket. We believe the loss to Blue Origin was the death blow to Aerojet by losing ULA, its only customer in space launch

- Revenues from RS-25 for the SLS program (14% of 2018 revenues), are set to decline from the Sept 2018 completion of a $2.0bn contract, and the run-off from the 2015 $1.5bn contract to be completed by 2023

- Longer-term challenges remain with NASA’s over-budget Space Launch Systems (SLS) program dubbed the “rocket to nowhere”, and a recent change of tone at NASA suggest it is taking steps to find cheaper commercial alternatives to the RS-25

- In 2018, Aerojet benefitted from boosts in missile orders from key programs which are set to decline by 5% and 11% in 2019/2020,respectively, according to the recent March 2019 DoD budget request. We estimate that Aerojet’s revenues increased $117m in 2018 from the growth in just two key programs: Standard Missile and THAAD. These two key programs are budgeted to decline by 2% and 35% in 2019 and 2020, respectively.

- Declining backlog quality: largely unchanged since 2015, now becoming more unfunded and taking longer to convert to sales

- In Q2’18, AJRD’s CFO said backlog conversion to NTM sales is a critical metric. By year end 2018, it declined

Spruce Point Believes Aerojet Rocketdyne(NYSE: AJRD) Is A “Strong Sell”

Given the fundamental backdrop, Spruce Point is not surprised to see aggressive accounting and financial presentation methods being used by Aerojet that project an image of stability and growth.

Actions By Aerojet’s Management And Pivoting To Acquisitions Validate Our Concerns About Troubles Ahead:

- Aerojet Has Had Three Recent Executive Departures From A Team of Eight Members, Including Its SVP of Space

- Aerojet Stopped Disclosing “Competitive Strengths”, “Revenue Visibility” and “Propulsion Leadership” In The Recent 10-K

- Aerojet Is Now Turning To Acquisitions For Growth, A Classic Sign That Organic Growth Is Disappearing:

- The recent March ‘19 acquisition of 3DMT (announced after market on Friday month end), appears defensive, and has declining sales and accelerating losses, while CEO Burke sold $1m of stock just three days before the deal was announced

We Believe Aggressive Accounting And Financial Obfuscation Are Being Used To Materially Mask The Slowdown

- Headline EPS, EBITDA and Cash Flow Appear Aggressive And Overstated Considering Spruce Point’s Adjustments:

- Numerous subjective contract adjustments being used to boost results and “one-time” items not being treated as such

- We Believe EBITDAP margins are inflated by 610bps and its YoY growth is only 3.3%, not 16.1% as depicted by management

- Adjusted for a one-time contract modification benefit disclosed in Q2’18, which Aerojet later omitted from disclosing in the recent 10-K, we estimate operating cash flow grew 2.3%, not 18.8% as depicted by management

- Changes in working capital accounts delivered exactly $0 to total operating cash flow In 2018, supporting our view of no underlying organic growth

- Unbilled Receivables Exploding: Indicative of Aggressive Revenue Recognition Ahead of Billing and Collecting Cash

- Aerojet recently stopped disclosing the definition of unbilled receivables

- New Revenue Adoption Obscuring Recent Results:

- Comparability of Revenue: Aerojet hasn’t restated 2017 results making YoY comparability difficult

- Obscures Working Capital Strain: Absent the restatement, working capital to sales has been growing materially negative each quarter throughout 2018

- Inventory Being Obscured: No longer provides complete inventory transparency, which is unusual for a manufacturing company. Inventory to backlog ratio had been shrinking prior to the change

Read the full article here by Spruce Point Capital