Spruce Point is pleased to issue a unique investment research opinion on Cintas Corp. (“CTAS” or “the Company”), a uniform rental, safety, and fire inspection service company. The report outlines why we believe shares face 60% – 75% downside risk to approximately $69 to $107 per share.

Q3 2019 hedge fund letters, conferences and more

Spruce Point Estimates 60% –75% Downside Risk ($69 -$107/sh) At Cintas Corp. (NYSE: CTAS)

We Believe Cintas Overpaid For G&K, Is Struggling To Integrate It, And Spinning A Weak “Beat And Raise” Story

- To consolidate share and extract synergies, Cintas acquired G&K Services in 2017 for $2.1bn with new debt. Based on proxy statement disclosures, Cintas paid an additional $425m above its initial offer to acquire a business that was described to us as having a poor reputation

- Cintas touted a “Beat and Raise” story post acquisition, but based on our forensic review, it appears that Cintas may have suppressed G&K’s sales, only to raise sales guidance by a similar amount to the sales that had been suppressed

- Even worse, evidence points to Cintas over-estimating expenses, only to roll-them back and claim outperformance. In addition, Cintas said one thing, but did another by subtly changing capital priorities (cutting capex, increasing share repurchases) in an effort to artificially grow EPS. For FY 2019, we estimate Cintas had no underlying outperformance relative to initial guidance

- There are classic signs of a mismanaged acquisition and financial stress post acquisition:

- COO and 22yr Cintas veteran J Phillip Holloman “retired” in mid 2018

- Post deal closing, receivables are growing at nearly 2.0x sales; DSOs are at record levels; inventory growth is diverging from sales growth. Cintas’ credit facility size has increased 3x in size despite sales up only 40%

- Working capital to sales and bad debt has exploded to 20% of sales and 4% of receivables, respectively: both metrics are higher than Cintas and G&K on a standalone pre-acquisition basis. Cintas has still failed to consolidate its national receivables collections practice, while scores of customers are complaining about billing practices

- Cintas’s leverage is higher than it appears with material cash that is restricted and trapped abroad. We observe the Company is becoming more dependent on short-term financing with commercial paper as cash collections worsens

- Cintas recently sold a $73m investment for a reported 35x return, yet won’t disclose any details about the mysterious divestiture. The timing of the sale to generate cash is suspicious in context

- Weakness in oil and gas is emerging. Cintas took on added exposure to this industry from acquiring G&K

- Based on our analysis, ex: G&K’s financial contributions to Cintas, we find no underlying EBITDA margin improvement in the core Cintas business, and that earlier leverage benefits of EBITDA growing faster than revenues have evaporated

Spruce Point Estimates 60% –75% Downside Risk At Cintas Corp. (NYSE:CTAS)

Investors Misunderstand The Risks Associated With Fraud Conducted At Cintas’ Fast Growing Fire Protection Business

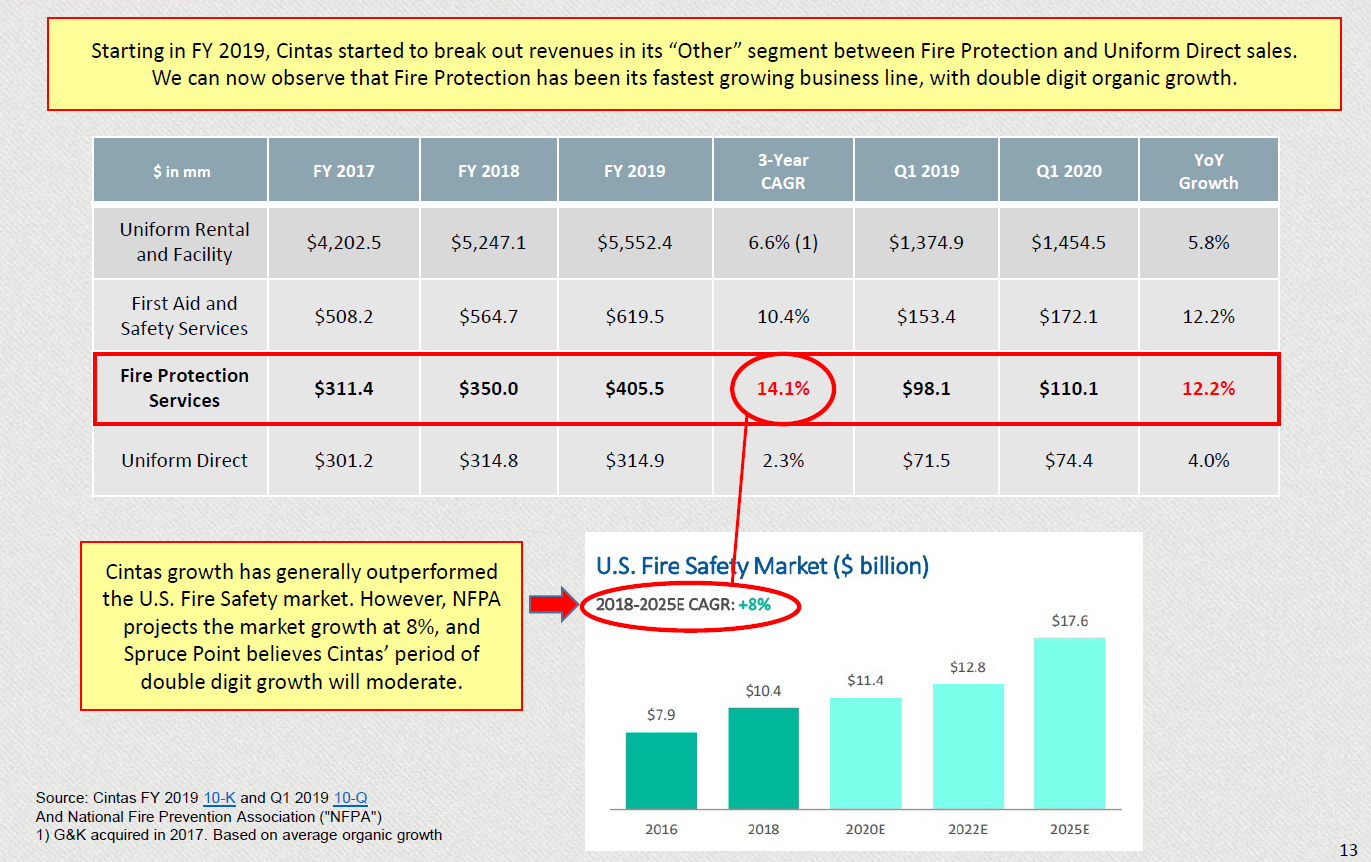

- Recent changes in revenue disclosure reveal for the first time that Cintas’ fastest organically growing business is fire inspection, which has grown at a 3 year CAGR of 14%, above the historical and projected industry growth rate of 8% as illustrated by National Fire Prevention Association

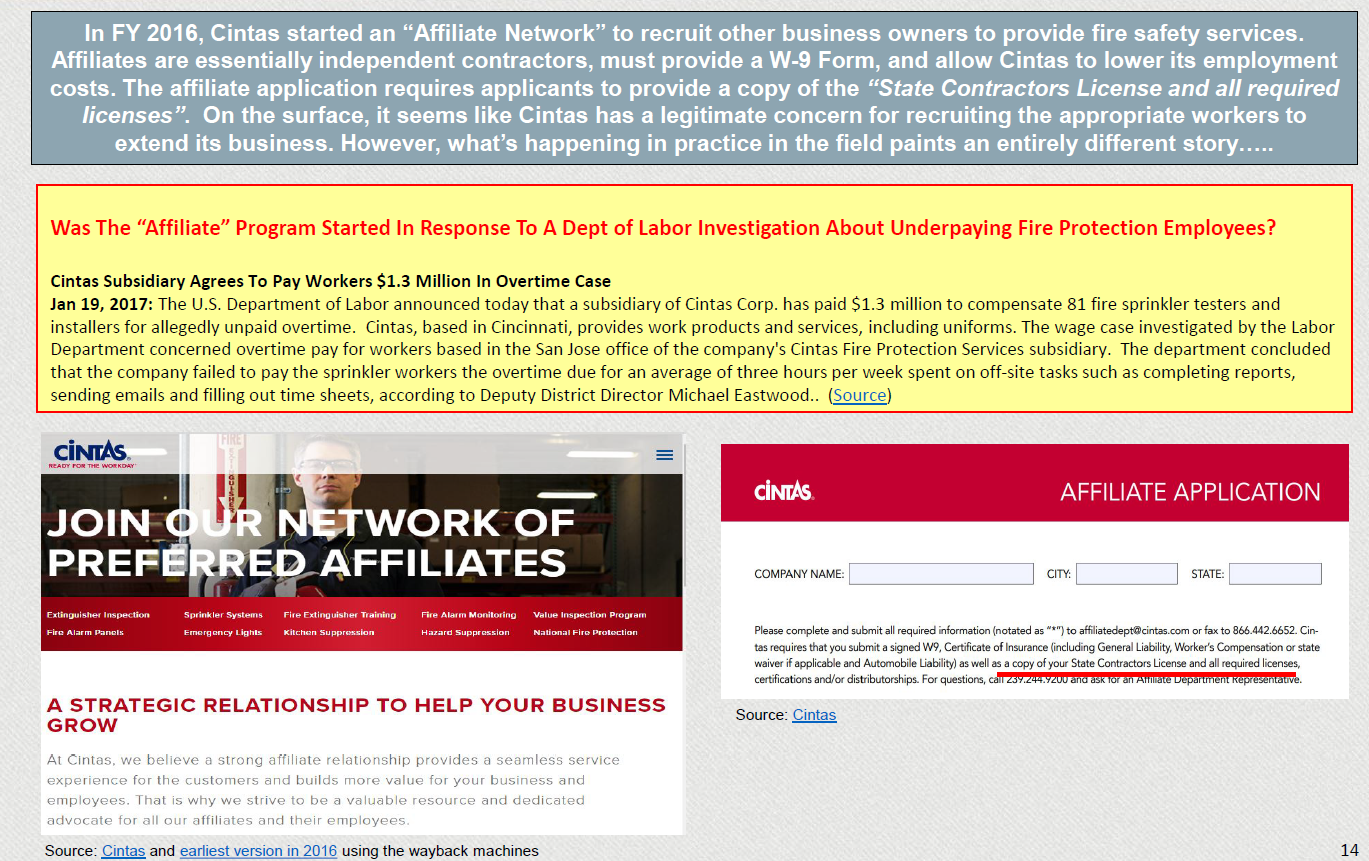

- Based on our research, the biggest fundamental challenge in the industry is a qualified labor shortage. Cintas has used an “affiliate network” to expand its reach, but this approach brings challenges such as monitoring the quality and capability of its workforce

- Using a Freedom of Information Act (FOIA) request, we find that Cintas was charged with fraudulent business practices. Upon a fire outbreak in Aurora, IL, it was determined that Cintas had 8 of 12 inspectors unlicensed and unfit to carry out inspection duties for the 22 properties within Aurora’s jurisdiction. These inspectors were thus falsifying inspection records. Based on our research, we believe this may not be an isolated incident, and that Cintas may have breeched its credit agreement by incorrectly representing that it holds all the necessary licenses to conduct its business in compliance with the law

- Cintas must conduct an independent and formal review to assure all its stakeholders that it is in compliance with all applicable laws, and holds all necessary permits when conducting life-critical inspection operations

- Cintas is also being sued in a wrongful death lawsuit for inaccurate inspections in a mining accident that was documented by the Mine Safety and Health Administration. Incidents such as this, while very unfortunate, add complex tail risks to its business

- Given lapses in judgement such as this, and based on industry conversations, it doesn’t appear to be a secret in the industry that Cintas has a poor reputation. As a result, new money is flooding into the industry to disrupt Cintas’ national market position

- We find evidence that historical contracts that locked in customers for 3-5 years are being shortened to just 1 year, and that prices are compressing; both are negative outcomes for Cintas

- Fueled by cheap financing and the ability to leverage contractually mandated inspection revenues, private equity players are creating regional platform acquisition vehicles to seize market share from disgruntled Cintas customers. In addition, APiGroup, a large national competitor was just acquired by a UK SPAC, and will be listed on the NYSE, giving it broader access to public capital to compete against Cintas

Read the full article here by Spruce Point Capital Management