Spruce Point is pleased to issue a unique investment research report on Mettler-Toledo International Inc. (NYSE:MTD) (“Mettler,” “MTD” or “the Company”), formerly known as Taser International, an analytical equipment provider to industrial, lab, and retail industries.

Q2 hedge fund letters, conference, scoops etc

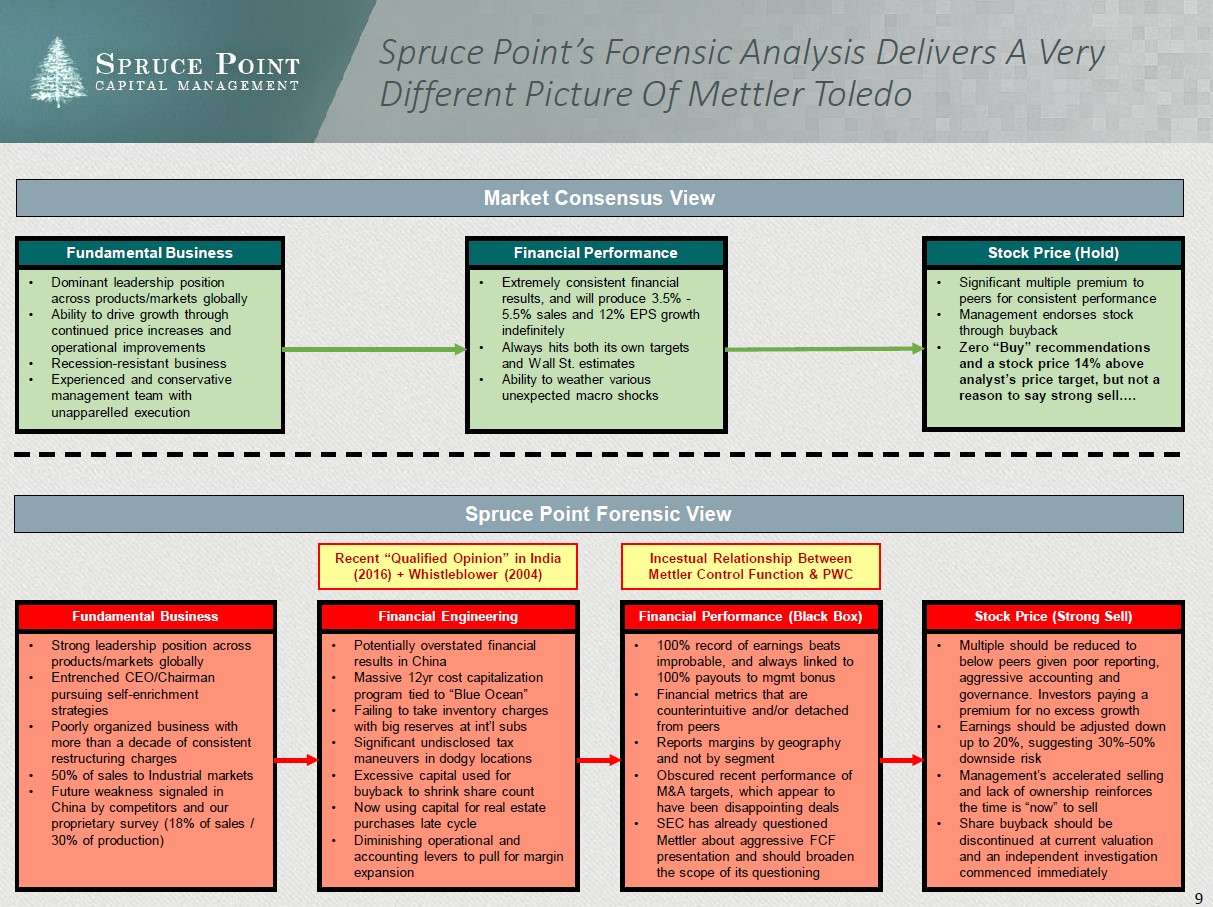

Executive Summary

Spruce Point Estimates 30% –50% Downside Risk At Mettler-Toledo (NYSE:MTD)

Spruce Point has significant concerns about Mettler-Toledo (NYSE: MTD), an analytical equipment provider to industrial, lab, andretail industries. Since CEO Olivier Fillioltook over in 2008, Mettler’s ability to never miss quarterly Wall St earnings estimates raises doubts about the quality of its financial statements. Run by secretive management in Switzerland, and with key U.S.-based financial, tax, and audit managersall having worked at current auditor PwC, we worry that adequate, independent questioning of its financial results are lacking. Prior allegations of financial misreporting 15yrs ago may hold weight in light of our fresh look at the allegations and broader information available today.Wefind strong evidence of aggressive financial, tax and accounting policies used to bolster earnings, notably outlandish share repurchases that are being conducted at 36x P/E, which rewards management with cash bonuses for buying stock. Our diligence into Mettler’s China business shows evidence of significant profit overstatement, and cash running through shell entities and an empty office. We call for an independent committee to evaluate our findings. We see 30% -50% ($410-$574/sh) downside once investors dissect EPS quality and realize MTD’s valuation is extreme.

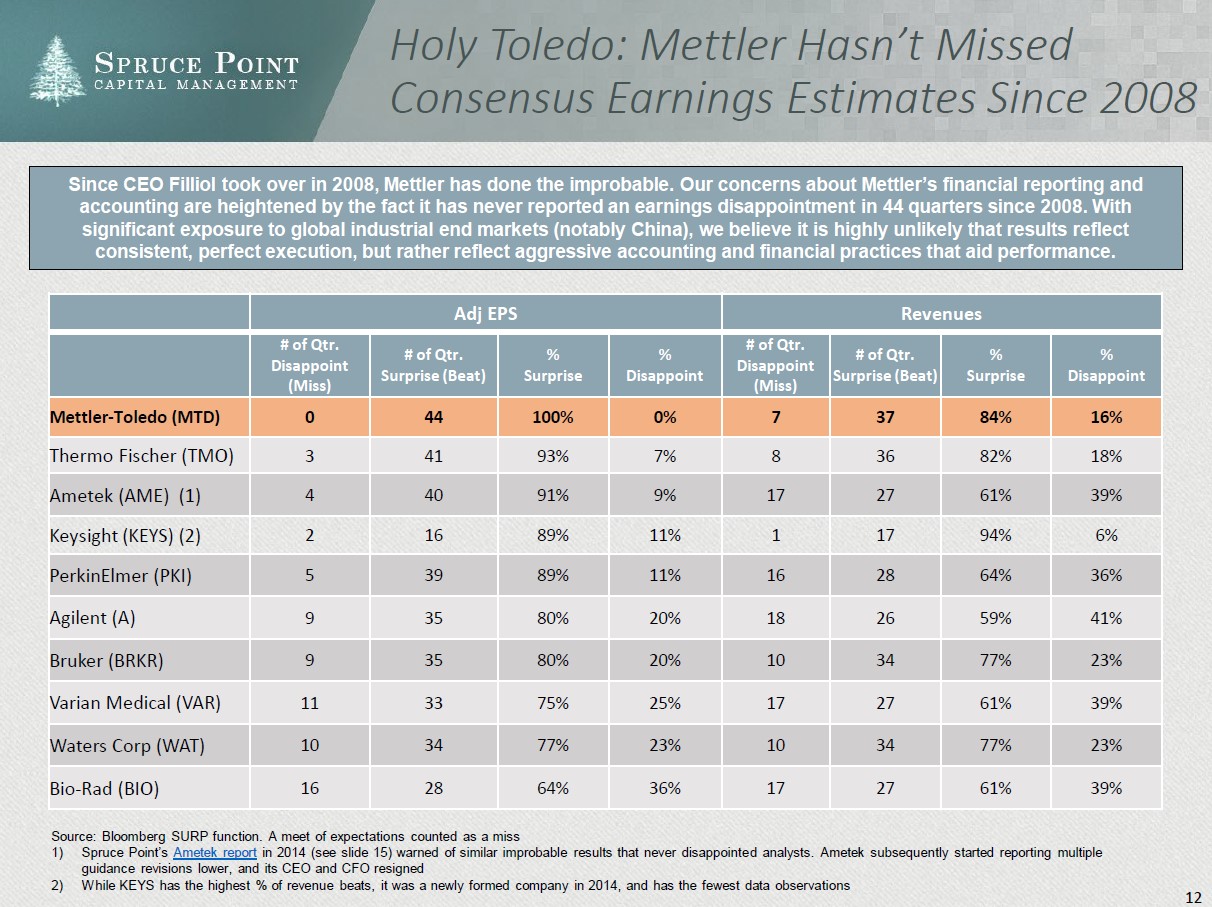

A High Precision Company That Never Misses Numbers, Or Worse, Highly Manipulates Financial Results?

Mettler has exceeded sell-side quarterly EPS targets 100% of the time since 2008, and by no coincidence, management has always met 100% of its annual cash bonus targets. This is a miraculous achievement given our belief it has a ruthless culture that firesbusiness managers quickly that don’t hit numbers:

- No backlog and short order business with significant industrial market exposure:Yet, Mettler is immune from cyclicality

- Able to navigate through every emerging market/trade crisis unscatheddespite large China exposure (18% of sales & 30% of production)

- Acquisition folly: Mettler has generally avoided acquisitions, but we find evidence that its past two deals in 2016/2017 that it spent $200m+ to acquire have not performed to plan and/or have financial reporting anomalies

- Able to navigate black swan currency events: EUR/CHF and USD/CHF are two of its biggest FX exposures. In 2015, during the unexpected Swiss Franc revaluation, causing a 20%+ move, Mettler claimed only a modest guidance revision, and that it had miraculously timed an increase to 90% of its EUR/CHF hedge. Yet, it rapidly borrowed money and its audit director abruptly resigned thereafter

- Never exposed to commodities: Mettler never mentions commodities as a component of its business in any SEC filing or conference call, however, we have evidence that commodities such as steel are an actively managed input cost

- No material customer concentrations: Mettler claims no customer is >1%, however, we believe it may be exposed to Pitney Bowes, a significant customer based on import trade records, who is facing increasing bankruptcy risk and a disruption headwind is notpriced in

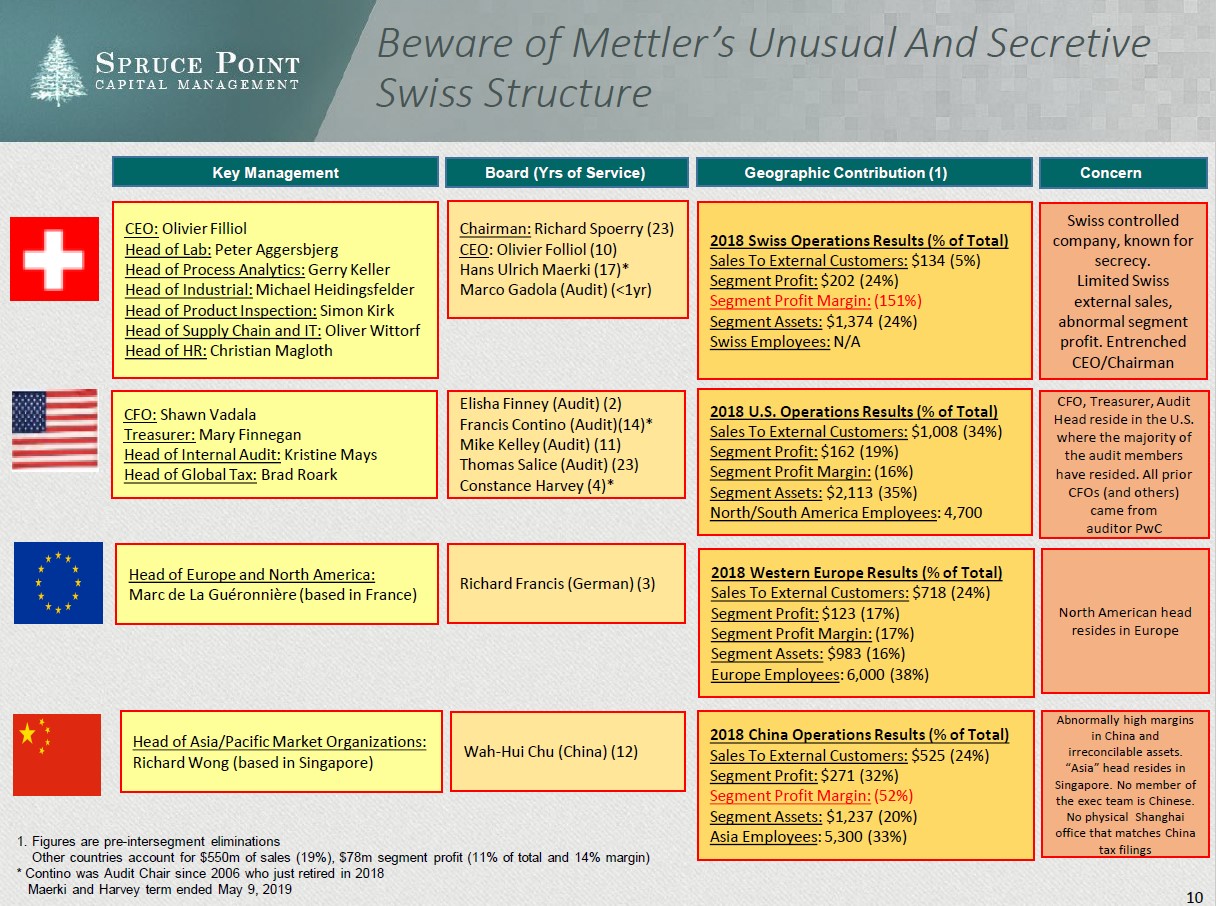

Oddly Organized Company That Doesn’t Seem To Match Customer Footprint

Top management resides in Switzerland, and is known for being secretive:

- The Head of North America is based in France, managing a key Mettler business from the other side of the Atlantic

- The CFO, Treasurer, Head of Internal Audit, and Head of Global Tax all reside in the U.S.

- China is a material part of its business, yet its Head of Asia is in Singapore, and no Chinese manager is part of the executive team

- Mettler’s website is organized around products, industries, and four distinct geographies. However, its financial reporting doesnot reflect its go-to market strategy to customers. Mettler does not disclose sales by industry end market, instead reporting sales by laboratory, industrial, and retail without providing margins in these categories. Instead, Mettler points to geographic margins, and uses enormous intercompany eliminations and sales that complicate the analysis of underlying segment performance

Past Allegations Made 15 Years Ago May Have Merit With The Benefit of a Fresh Investigation

Investors forgot that in 2004, Mettler delayed its 10-Q and commenced an audit committee investigation:

- An employee made an allegation that later revealed questions about Mettler’s information systems, inventory write-downs and reserves, and the operating of internal controls. In essence, key practices affecting financial reporting quality

- While claiming no need for financial restatement, Mettler stated further “the Audit Committee and the Board have determined that it would be in the best interests of the Company to make changes in the leadership for the oversight and control of its financial operationsto correct the “tone at the top” and ensure it is consistent with the Board’s commitment to maintaining strong corporate governance. The Company will enhance the accounting organization, both by adding personnel to that function and by increasing training for all members of theorganization.” Many of the same managers are still at Mettler (notably CEO Filliol) from the time of this investigation

Spruce Point Estimates 30% –50% Downside Risk

Relationship Too Close With PwC, An Auditor Slapped With Dozens of Lawsuits For Failing To Catch Fraud

- PwC has financially settled many high profile cases charging it with failure to detect fraud, including the largest settlement in U.S. history related to the collapse of Colonial Bank

- Every Mettler CFO since coming public in 1998 has worked at PwC

- Mettler’s Head of Internal Audit is a 14yr PwC veteran, and its Head of Global Tax also worked at PwC

- Mettler has no named Chief Accounting Officer/Controller signing the 10-K per securities law requirements

- In India, where PwC audited Satyam, the biggest corporate fraud in India’s history, auditors can be detained and face jail time for facilitating fraud. We find that PwC resigned as Mettler’s auditor in 2016. Upon appointment of Deloitte, it issued a “material weakness” and “qualified opinion” related to unbilled revenues and accruals assessments of provisioning for various asset balances”. This sounds eerily familiar to the employee allegations made in 2004.

CEO With A Potentially Misrepresented Bio Undermines Confidence

- A close look at a subtle change in his biography reveals he may have overstated his work experience at Bain & Co.

- His biography claims he ran the Process Analytics Division from 1999-2007. However this is contradicted by old proxy statements and his original employment agreement and title appointment that dates to 2001

- Various company sources suggest he ran the Analytics Division, was Head of Marketing, Sales, Service, and ran the China business too all at the same time, a major concern we will detail further. With a CEO in charge of so many aspects of the business, we worry that Mettler does not have the appropriate separation of duties in place. This concern is mirrored by the fact that long time CFO William Donnelly was in charge of Investor Relations, Finance, Supply Chain Management, Information Technology, and the Blue Ocean Program all at the same time

- Employee allegation of financial misconduct came weeks after Filliolwas promoted to Head of Marketing, Sales, & Service

- We estimate Filliolhas extracted $257m from Mettler (salary, bonus, stock sales) and controls another $270m of stock post the implementation of aggressive financial, accounting and tax policies, notably diverting billions of cash flow to buybacks while always hitting cash-incentive based Adjusted EPS targets that don’t adjust for excessive stock repurchases

Evidence of Massive Cost Capitalization of Software And A 12yr ERP Implementation Dubbed “Blue Ocean”

- Around the time CEO Filliol took charge in 2007, Mettler embarked on its “Blue Ocean Program” described as “a new global operating model, with standardized, automated and integrated processes, with high levels of global data transparency.”

- 12yrs later, Mettler claims the program has another 15-20% to completion. Mettler stopped disclosing direct costs related to theprogram in 2012, and has made $133m of total restructuring payments since 2009 (recognizing them every single year)

- When we asked former employees about Blue Ocean, each snickered, and all agreed it is overly ambitious and dragged on far longer than planned. Recent Glassdoor reviews show that outdated technology is still a consistent and recurring theme

- We believe it may be serving as massive bucket to capitalize significant R&D costs, while delaying earnings recognition:

- Mettler has an anomalous high capex to sales ratio, and a relatively low R&D to sales and per employee metrics

- It changed its software amortization policy: 3-5yrs to 3-10yrs post 2007 (Amort of capitalized dev. costs inc. from 5 to 10yrs)

- Based on current annual amortization of capitalized software expense, we estimate Mettler amortizes costs upwards of 13yrs

- We estimate Mettler has capitalized an average of $50m of software per year

- History shows ERP troubles can result in admission of material financial weakness. Bio-Rad (BIO) serves as a case study for the challenges of implementing an ERP. It started its ERP in 2010, and admitted implementation challenges that ultimately resulted in the admission of material weaknesses of internal controls. Bio-Rad completed its ERP in 7 years.

Read the full article here by Spruce Point Capital Management