Spruce Point initiates strong sell opinion on XPO Logistics Inc. (XPO), sees 40%-60% downside potential in a report titled, “Trucking Ridiculous; End Of The Road.”

Q3 hedge fund letters, conference, scoops etc

Spruce Point believes that XPO Logistics, Inc. (NYSE: XPO or “the Company”) is a classic stock promotion orchestrated by a web of individuals with a checkered past, including ties to convicted felons, and an individual that abetted a Ponzi-scheme. As a result, we see 40%-60% intermediate downside risk to $24.00-$36.00 per share, with up to 100% long-term downside risk as a result of a $4.7 billion debt overhang, flawed business model, questionable governance, dubious financial and accounting methods, increased regulatory scrutiny, and a loss of confidence in management.

Spruce Point Estimates 40% – 60% Intermediate Downside Risk, 100% Long-Term Downside

Spruce Point has been following XPO Logistics (NYSE: XPO) for years, a transportation and logistics roll-up founded by Bradley Jacobs, co- founder of United Rentals (URI) which collapsed in an accounting scandal during his leadership. Based on our forensic investigation, we believe XPO appears to be executing a similar playbook to URI – resulting in financial irregularities that conveniently cover its growing financial strain and inability to complete additional acquisitions despite promises. Given its unreliable and dubious financials, $4.7 bn debt burden, inability to generate sustaining free cash flow, and dependency on external capital and asset sales, we have a worst-case terminal price target of zero.

A Value Destructive Roll-Up, Covering Financial Strain and Dependent On Financing For Survival

XPO has completed 17 acquisitions since Jacobs took control in 2011 and deployed $6.1 billion of capital. Yet by our calculations, the Company has generated $73m of cumulative adjusted free cash flow in an expansionary economic period. In our view, this is indicative of a failed business strategy yielding a paltry 1.2% return on invested capital. XPO is dependent on external capital, asset sales, and factoring receivables to survive and is covering up a working capital crunch that can been seen by bank overdrafts – just like Maxar Technologies (MAXR). As credit conditions tighten, cost of capital increases, and XPO’s business practices come under greater scrutiny (eg. U.S. Senate), its share price could swiftly collapse in Enron-style fashion.

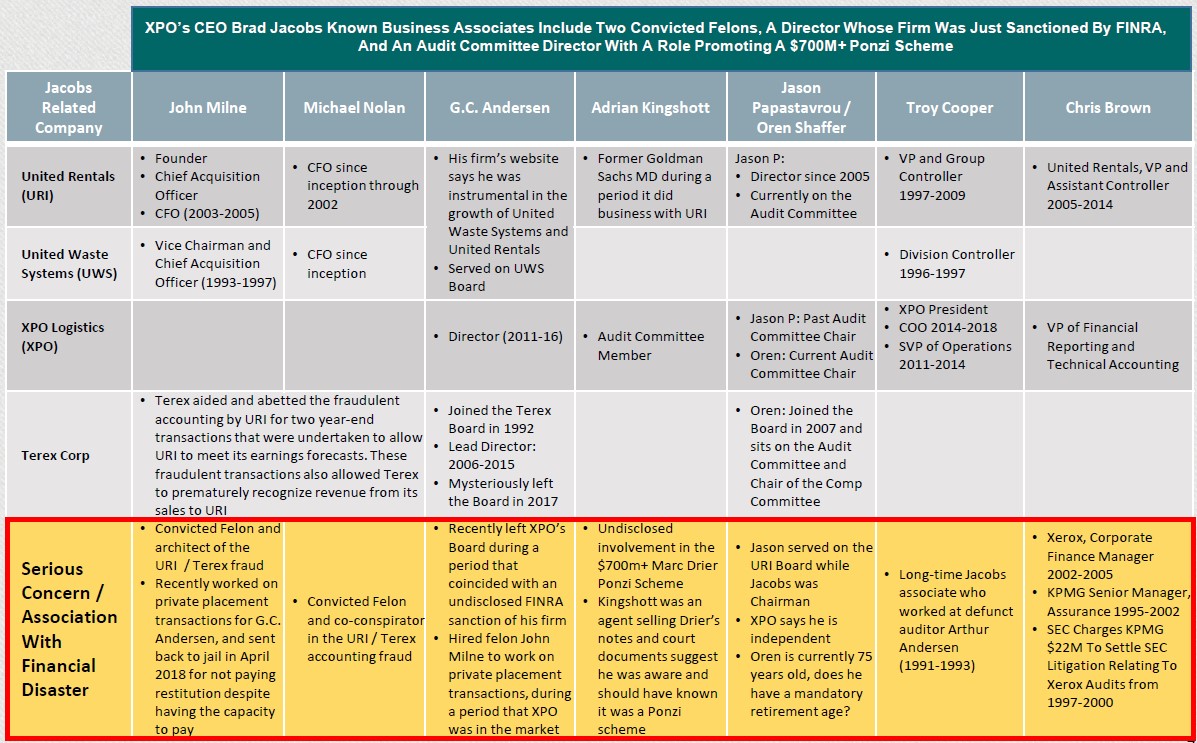

Insider’s Undisclosed Association With Convicted Felons And A Massive Ponzi Scheme

CEO Jacobs has surrounded himself with a web of associates from his United Waste Systems and United Rentals days. Two of his partners, Mike Nolan and John Milne, were convicted of accounting fraud. XPO’s director G.C. Andersen recently employed Milne at his financial advisory firm during a time the company worked on private placements (potentially XPO’s deals) and was sanctioned by FINRA. This wasn’t disclosed to investors. XPO’s audit committee director, Adrian Kingshott, has omitted from his bio his role in the distribution of note securities in the $700m Marc Drier Ponzi scheme.

Dubious Financial Presentation And Aggressive Accounting

In our opinion, XPO has used a nearly identical playbook from United Rentals leading up to its SEC investigation, executive felony convictions, and share price collapse. We find concrete evidence to suggest dubious tax accounting, under-reporting of bad debts, phantom income through unaccountable M&A earn-out labilities, and aggressive amortization assumptions: all designed to portray glowing “Non-GAAP” results. Additionally, we provide evidence that its “organic revenue growth” cannot be relied upon, its free cash flow does not reflect its fragile financial condition, and numerous headwinds will pressure earnings.

Ridiculous Compensation Scheme To Line Insiders’ Pockets

XPO insiders have aggressively reduced their ownership interest in the Company since coming public, and recently enacted a new compensation structure tied to “Adjusted Cash Flow Per Share” – defined in such a non-standard way that it is practically meaningless. Conveniently, it ignores any measure of capital efficiency, which is critical in the capital intensive transportation industry, and would expose XPO’s poorly constructed roll-up. In our opinion, the Board is stacked with rubber-stamping Jacobs loyalists, none of which have requisite experience in the transportation and logistics industry. As noted above, the Board includes an audit committee member who abetted a notorious $700m Ponzi scheme.

An Epic Wall St Stock Promotion That Can End In Tears: Intermedia Target: 30%-60% Downside Long-Term Target: $0

XPO has recruited 19 brokers to cover it, with only 1 “Sell” opinion and an avg. fantasy price target of $114 (implying 90% upside). No analyst has conducted a forensic look at XPO’s earnings quality, or revealed its Board and management’s connections to convicted felons. XPO promotes itself to investors as a “technology” company and how it uses “robots” for warehouse automation, but ignores its growing financial strain, precarious $4.7 billion debt load, and inability to hit its cash flow target. Warren Buffett famously said, “Only when the tide rolls out do you know who as been swimming naked” – words of wisdom for XPO shareholders. A crisis of confidence in management and a loss of access to capital could wipe out shareholders. In the interim,we see 40% – 60% downside risk as the market reassess XPO’s earnings quality, outlook, and sum-of-parts multiple.

Spruce Point’s Honest Opinion of XPO’s Investment Prospects

XPO’s CEO Bradley Jacobs has lectured in the past about honesty. Our report will stress test XPO’s financial statements and accounting to see if they give an honest view of its financial performance and outlook.

Source: Automotive Logistics 2016, CEO Jacobs’ Presentation

A Careful Look At XPO’s CEO Jacobs And His Business Associates Raises Multiple Red Flags

XPO’s CEO Brad Jacobs Known Business Associates Include Two Convicted Felons, A Director Whose Firm Was Just Sanctioned By FINRA, And An Audit Committee Director With A Role Promoting A $700M+ Ponzi Scheme

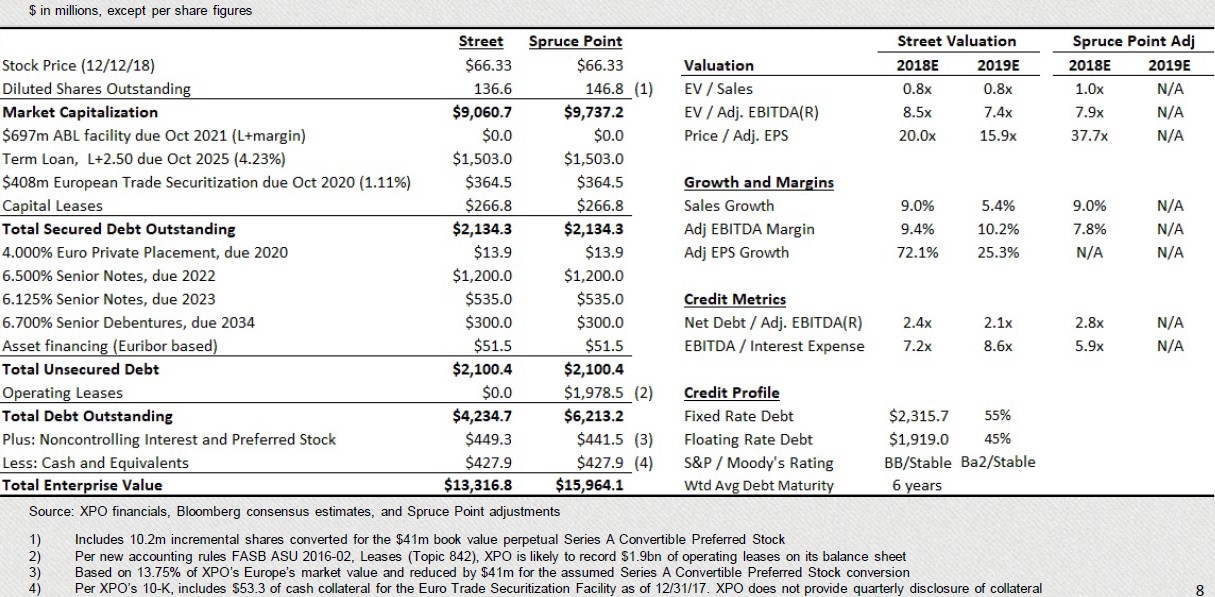

Capital Structure And Valuation

XPO is more expensive than it appears given its highly “adjusted” Non-GAAP results, and analysts’ inability to correctly account for the 10.2m shares that are freely convertible from the Series A Convertible Preferred stock (market value = $615m). Our report will detail XPO’s aggressive tactics to bolster reported Adjusted EBITDA and EPS, and will argue that XPO trades at a premium to the sum-of-the-parts of its acquisitions despite no evidence it has created tangible financial value from its levered (junk) acquisition spree.

See the full article here by Spruce Point Capital Management