Spruce Point Capital Management is pleased to issue a “Strong Sell” opinion on PetIQ Inc (NASDAQ:PETQ). Our report outlines why PETQ faces 75-90% downside risk to approximately $2 to $8 per share due to fundamental challenges in its core pharmaceutical distribution business, unrealistic growth expectations in its recently-acquired services segment, and a broader appreciation of the company’s dubious past and questionable management team.

Q1 hedge fund letters, conference, scoops etc

Executive Summary

Spruce Point Sees 75% -90% Downside To PetIQ, Inc. (Nasdaq: PETQ)

PetIQ, Inc. (“PetIQ,” “PETQ,” or “the Company”), a recent JOBS Act IPO, is the product of an acquisition of an unattractive veterinary services business by a shady veterinary drug distribution business. The distribution business, built on the ethically-nebulous practice of veterinary drug diversion into the retail channel, appears to depend heavily on access to vendor rebates for earnings, and is currently at risk to changes in drug manufacturers’ approach to retail distribution. PetIQ’s planned rollout of 1,000 new pet wellness centers could also burn over $200M in cash over the next five years without even achieving break-even profitability until FY23. The Company has already changed its story and growth targets numerous times despite being public for just 20 months, and is not fully transparent about the risks facing both businesses. Management is asking investors to trust it to execute despite having missed nearly all prior projections. Further, we find that PetIQ management –whose CEO has close ties to the notorious Petters Ponzi scheme and the Fleming Corp accounting fraud (which go undisclosed on his online bio) –has a history of engaging in business practices which have come under legal and regulatory scrutiny. Investors should proceed with extreme caution.

- PetIQ Occupies A Murky Space In The Pet Pharmaceuticals Market: PetIQ purchases prescription and OTC veterinary pharmaceuticals from veterinarians and licensed distributors. Manufacturers have historically restricted themselves from selling to non-licensed distributors or directly into the retail channel in order to protect veterinarians from retail competition for pet medicine sales. However, veterinary drugs do ultimately reach the retail channel –both brick-and-mortar and online –through non-veterinarian distributors (such as PetIQ) which purchase excess product from veterinarians, and which often form arrangements with veterinarians to purchase inventory in size. While not technically illegal in most states, the practice is frowned upon by vets, and has been the subject of congressional hearings and FTC commentary through the last several years. PetIQ’s General Counsel, who presumably blessed its business practices –yet whose personal bankruptcy was never disclosed to investors –recently resigned in Mar 2019. Manufacturers are increasingly beginning to bypass the grey market and sell directly to retail –as is Merial with its Frontline product, as of FY18 –showing cracks in PetIQ’s economic ecosystem. Wider competition in the pet medicine distribution space and greater transparency into distributor margins among retailers could bring PetIQ product segment operating margins –8-9% as of today –closer to the 1-3% margins shown by other pharmaceutical distributors.

- Core Pharmaceutical Distribution Business Is Under Pressure: Consumers are shifting away from topical flea and tick medications (30-40% of PetIQ sales) in favor of more dependable and hassle-free oral and other treatments. Frontline, one of PetIQ’s major sellers, is facing pressure from both this and the proliferation of cheaper substitutes. Consumers are also reporting that Frontline has become less effective following a recent formula change.

- Recently-Acquired Services Segment From VIP Will Deliver Slow Sales Growth And Burn Significant Cash: Whereas PetIQ management has publicized its new services business as a 25% organic grower, total segment growth was just 9% in FY18, and we estimate that growth from existing stores was just 1-2%. Management is planning to roll out 1,000 new health and wellness centers in retailers such as Walmart through 2023, and expects each store to offer 30% contribution margins at maturity, but we estimate that the roll-out could burn $200M of cash through the next five years (perhaps more thereafter) while just barely achieving break-even profitability in FY23.

- Suspicious Circumstances Around VIP Acquisition: PetIQ eliminated $111M of inter-company sales in the combined company’s pro forma 2017 income statement (over half of PetIQ’s COGS), revealing the closeness of the relationship between PetIQ and VIP. Of the $220M purchase price, $76M was allocated to VIP’s “customer relationships” which were written down twice from $90M, suggesting that these relationships wereofdeclining quality or were reduced to suppress amortization and cut prospective GAAP losses in half. After the acquisition, over 100% of earnings for the pro forma 2017 combined company were attributable to vendor rebates, which grew by 175% in the year prior to the deal. We find it suspiciousthat PetIQ would spend $220M on the $250M-revenue VIP business after its EBITDA appears to have declined for two straight quarters and go negative prior to the acquisition.

- Acquisition Driven By Fragile Industry Dynamics: Spruce Point believes that PetIQ was motivated to acquire VIP for more direct access to manufacturer relationships and vendor rebates as it outgrew the capacity of its previous vendors. At the time, this arrangement would havebeen beneficial to Merial as well, as it would have allowed Merial to drive retail sales of its pet medications more directly while maintaining the appearance of selling only to vets. However, now that Merial has begun selling directly to retail, PetIQ is at risk of seeing its margins regress to those of pharmaceutical distributor peers as retailers gain greater visibility into distributor margins and wholesale pricing.

- Poor Earnings Quality With Widening Rift Between GAAP/Non-GAAP Results And Cash Flow: VIP financials suggest that combined-company earnings depend heavily on rebates. Management adjustments are responsible for close to half of Adj. EBITDA as of FY18, and these adjustments should increase as one-time store opening expenses are added back with the accelerating wellness center build-out. Adj. EBITDA grew by ~100% in FY18 despite OCF –which has been close to or below zero since the IPO –falling deeply negative.

- A Company With A Dubious Past And A History of Questionable Vendor Arrangements: PetIQ appears to have been born as W.T.F. Wholesale in the early 2000s. W.T.F. formally closed shop in 2011 –but not before accepting hundreds of thousands of dollars’ worth of product from veterinary suppliers without paying, after which it appears to have continued to do business as “True Lines Distributors,” as alleged in lawsuits.True Lines was a subsidiary of “True Science Holdings, LLC,” which became PetIQ in 2016. True Science appears to have formed non-arms-length relationships withveterinary drug wholesalers through the first half of the 2010s. A former supplier alleged that, during this period, True Science used these close relationships to manufacture artificially inflated assets and earnings. He also alleged that its accounting practices triggered a federal investigation in 2014.

- CEO With A History Tied To Vendor Rebate Schemes: CEO McCord “Cord” Christensen was a major funnel of investor money into the Petters Ponzi scheme –a fact which goes unmentioned on his online bio. He was characterized as an unknowing victim in court proceedings, but was closely associated with Petters as an employee and business partner through the 2000s, and controlled several entities which recruited millions of dollars of investor money for Petters. He was also involved with subsidiaries of Fleming Corp, which was identified as an accounting fraud for inflating earnings through the improper application of vendor rebates. The fraud was so egregious that the business was nicknamed “Flem-ron” in the scheme’s fallout.

- Downside Risks To Valuation Abound: We believe that PetIQ earnings are heavily dependent on access to manufacturer rebates. We consider these earnings of low quality at best. With Merial now selling Frontline directly to retail, we expect the value of PetIQ’s rebatestodwindle as Merial and larger retailers increasingly squeeze its markups. Should regulation surrounding the grey market change –for example, if regulators legitimize the retail channel for veterinary drugs –PetIQ could be at risk of disintermediation, and industry legitimization would likely lead to greater industry competition and pressure PetIQ’s unusually high margins. We also wonder whether PetIQ’s demonstrated profitability is sustainable given its questionable rebate accounting. The possibility of further regulatory investigation into PetIQ’s accounting builds further downside risk into thestock.

- Disappointing Services Growth & Product Segment Margin Contraction Yield Downside To PETQ: We believe that PETQ is set up to disappoint due to sell-side optimism around sales growth and margin expansion despite headwinds facing its distribution business and poor wellness center economics, and despite the fact that product segment gross margins are at risk to changes in animal drug distribution practices. Analysts valuePETQ using a multiple more than double that of other pharmaceutical distributors due to expectations of strong top-line growth, but we believe that any premium earned by its sales growth potential is offset by its poor earnings quality and downside risks to margins. We see 75-90% downside to PETQ on lower-than-expected services growth and margin contraction in the products business, as well as on multiple contraction as the market’s understanding of PETQ evolves.

PETQ: Yup, Another Low-Quality JOBS Act IPO

Studies have shown that the Jumpstart Our Business Startups Act (JOBS Act) –designed to ease IPO-related disclosure requirements for smaller, “Emerging Growth Company” firms –has permitted a growing number low-quality firms to go public. We see PetIQ as yet another low-quality Company which took advantage of the JOBS Act to go public.

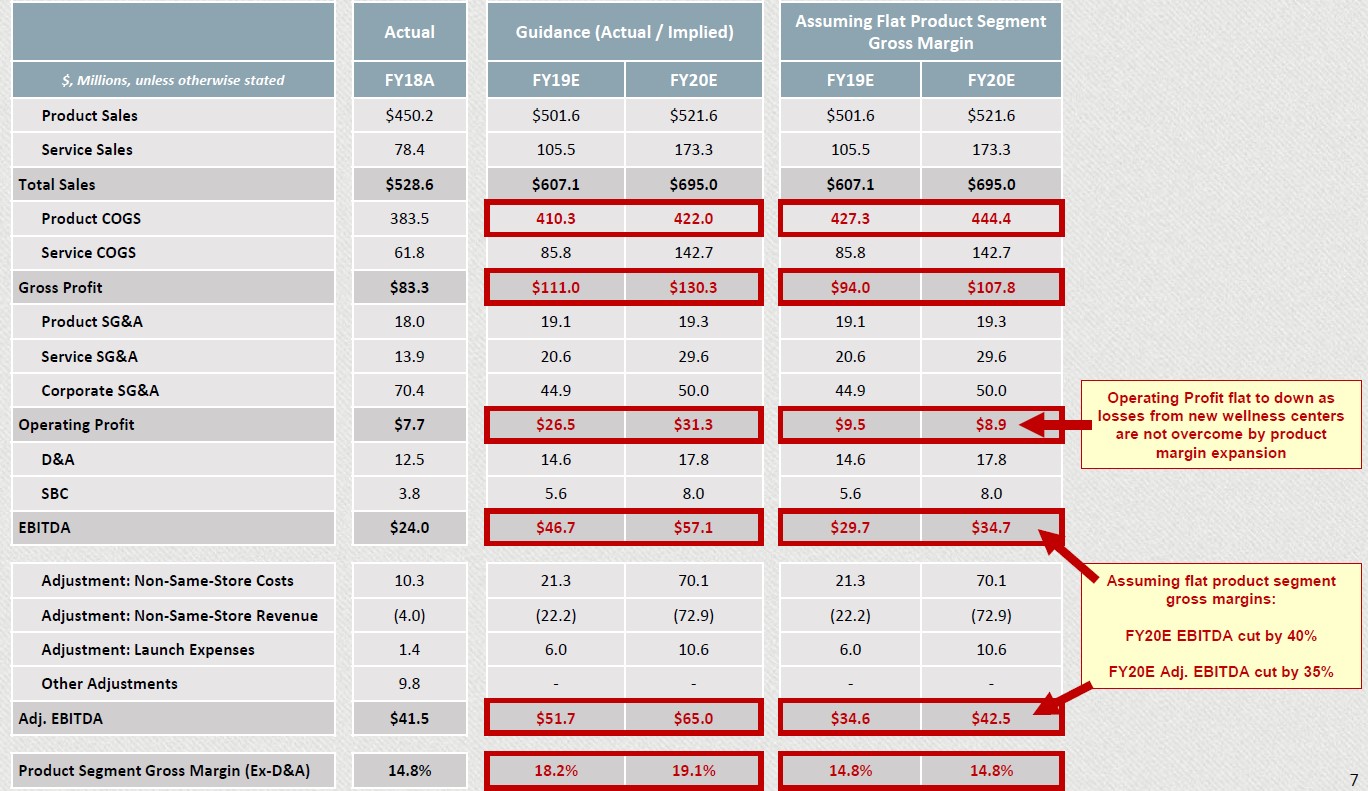

Street EBITDA Projections Imply Unlikely Product Segment Gross Margin Expansion

Spruce Point believes that, assuming the wellness center rollout is modeled according to management guidance, Street estimates imply material product segment GM expansiondespite demonstrated GM pressure. More realistic GM projections yield material EBITDA downside.

Read the full report here by Spruce Point Capital Management