Back in the heat of COVID, I pitched Kura Sushi (KRUS) to our Collective members. The stock traded around $14/share then, and everyone hated the idea.

“Why would you invest in a restaurant during COVID? What are you, some idiot?”

Today, KRUS is a $120/share stock.

That trade worked well for us.

But I think I found an even better setup with GEN Restaurant Group (GENK).

I pitched GENK to our Collective on March 13th. Since then, the stock is up 62% as insiders gobble up shares in an already low-float environment.

I’ve seen the name circulate on value investing Twitter and thought I’d share my write-up publicly.

Please note that we/I own shares in GENK. Do your own work. None of this is investment advice … you know the boilerplate mantra.

Let’s get after it!

Kura Sushi (KRUS) is my white whale. I wrote about it during COVID-19, got ridiculed online about it, and said everyone else was wrong. We bought some for the MO port at around $18/share and sold them at $37.

We felt like heroes. Until it hit $100/share, and I swore I’d never look at the stock chart again (it’s now at $120/share, laugh through the pain, lol).

Fortunately, other Collective members were smarter than us. One member emailed me claiming “that one trade (KRUS) paid for a few lifetime memberships.”

We walked so you can run. You’re welcome.

But then I found GEN Restaurant (GENK). And I realized that this is my redemption story. This is my chance to right all those wrongs of selling KRUS.

GENK is a Korean BBQ-themed all-you-can-eat restaurant. Guests cook their food over open flames and can choose between three main proteins: chicken, beef, and seafood.

The price-to-value ratio is incredible. You pay anywhere from $20 to $30 for all-you-can-eat Korean BBQ. Do I need to write anything else?

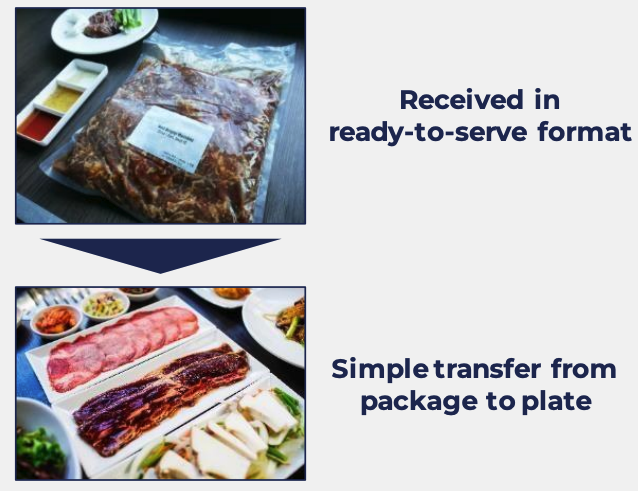

GENK saves time and money because the guests (i.e., customers) cook the food. The meats come in ready-to-serve packaging from Sysco. The packaging reduces the need for ample kitchen space. It allows GENK to fit more tables inside each store, thus maximizing revenue and profit per square foot.

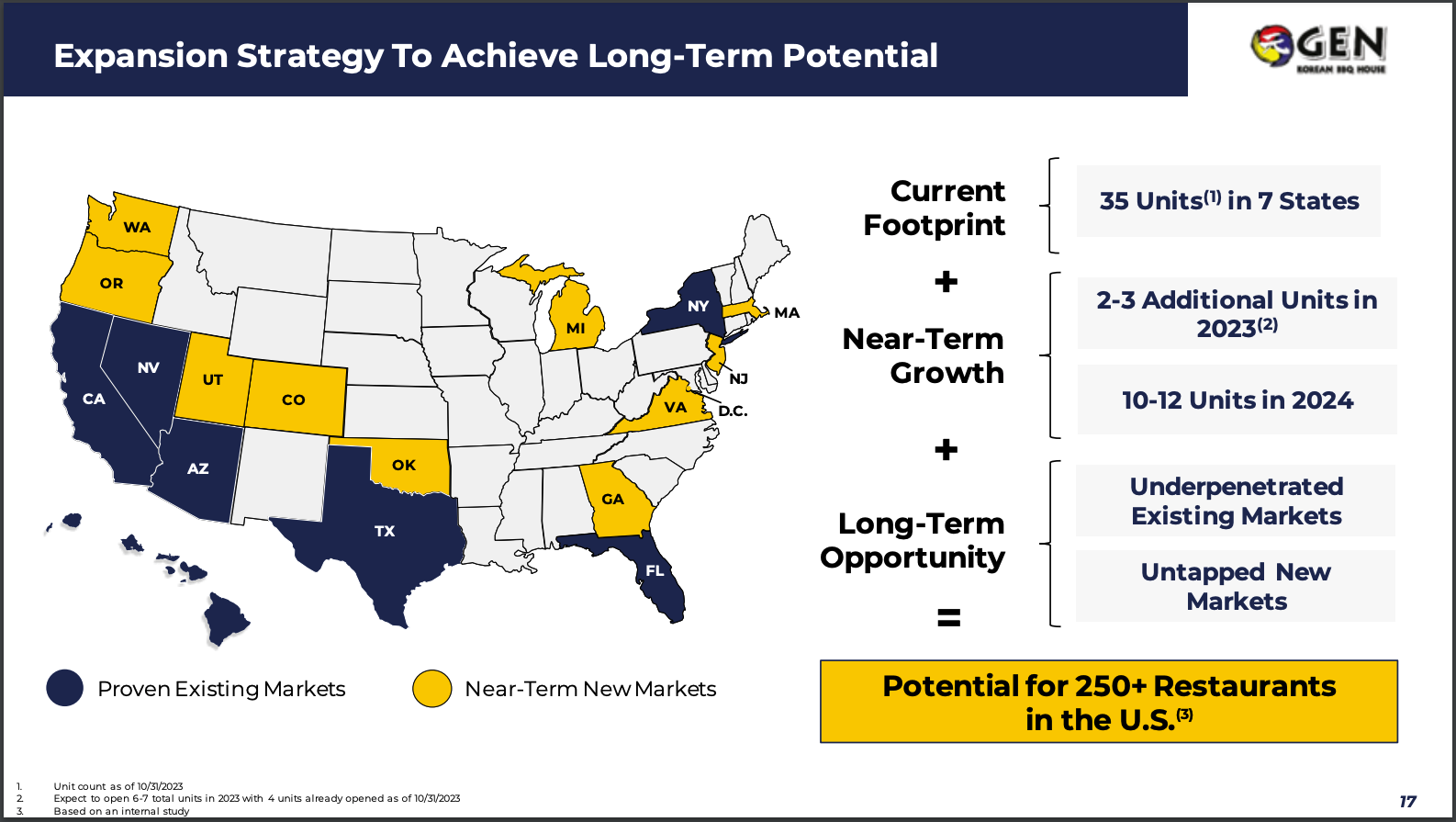

The company has 37 stores as of 2023. They plan on adding 10-12 in 2024 with a long-term goal of 250+ in the US. Each restaurant generates ~$5M in revenue with 40% cash-on-cash returns at 20%+ store-level EBITDA margins.

GENK has no debt, is already profitable, and uses its cash from operations to open new stores. The founder owns 1% of the company, and there’s barely any float left.

We get all this for 0.7x EV/Sales and ~6x 2027E EV/EBIT.

What Makes GENK Unique: Guest Experience, Food Delivery, & Price

Earlier I said that GENK is better than KRUS. I’m not just saying that because I’m bitter (I swear). There are a few reasons why I believe that.

First, GENK’s customers do most of the labor (i.e., cooking the food). This saves GENK money because they don’t need to hire chefs and outfit a large, expensive kitchen.

KRUS has some automation in its restaurants. For example, robots deliver your drinks, and the sushi arrives on a conveyor belt, not via a waiter. But they still have cooks in the back making the sushi and putting it on the trays. So, while this allows KRUS to have smaller kitchens, they still need chefs on the payroll.

Second, GENK’s partnership with Sysco provides a much simpler food delivery system. The food comes pre-packaged two to three times a week. All GENK has to do is open the package and put the meat on the plate.

Think about how much easier training new staff at GENK is compared to KRUS or other restaurants. Instead of finding a chef who knows how to cook, you just need someone who can open a bag.

Then there’s the price point. GENK is an all-you-can-eat restaurant, with lunch prices ranging from $18-$22 and dinner prices ranging from $29- $30.

Sure, KRUS isn’t the world’s most expensive sushi. But you’re still paying $5-7 per roll. And who doesn’t eat more than 5-7 rolls of sushi?

GENK’s pricing also caters to families and large groups. This makes sense because their restaurants look like hibachi grills. Everyone sits around an open flame and cooks their food. It’s perfect for families and doesn’t break the bank. Plus, kids love playing with fire.

Everything about this concept makes sense. And it shows in the company’s financials and store-level economics.

GENK’s Unit Economics & Financials

Here are GENK’s unit economics as of their latest investor presentation:

- Average annual revenue: $5M

- Average net build-out cost: <$3M

- Restaurant-level EBITDA margins: 20%

- Cash-on-cash returns: 40%+

- Payback Period: 2.5YR

The company generates positive free cash flow and uses those funds to open new restaurants. For instance, in 2023, GENK generated $181M in revenue, $33M in gross profit, and $22M in cash from operations.

The balance sheet is also clean, with zero debt (outside lease liabilities) and $33M in cash.

GENK is one of those companies where you want to invest every dollar of FCF into opening more stores because they generate such high returns. $1 invested in a new store returns 40% a year.

Like KRUS, there’s a long runway for store expansions.

GENK’s Growth Plans: 37 → 250+ Restaurants Nationwide

GENK currently has 37 stores as of year-end 2023. According to their investor presentation, they want 10-12 more units in 2024 with a long-term goal of 250+ units nationwide.

Can they get there? Yes. If there’s one thing I know about Americans, it’s that we love all-you-can-eat deals.

I have no idea when they’ll reach 250. It could take them a decade at 10-12 stores per year. But it doesn’t matter. The point is that they can realistically get there.

For reference, Golden Corral, another all-you-can-eat country-style buffet, has 397 restaurants nationwide.

This is a good place to discuss why the opportunity exists in the first place.

Why Does The Opportunity Exist?

There are a few reasons why this opportunity exists.

First, GENK is a broken IPO with unseasoned public market founders/operators. This isn’t their fault. It’s just part of the growing pains of a new public company, especially a restaurant stock.

The stock IPO’d at $18.30/share for a $590M market cap (3.6x 2023 sales). Since then, it’s declined by 66% as investors YOLO’d into NVDA and BTC.

There are also fundamental reasons why you would’ve sold the stock. The company reported ~10% YoY revenue growth, which didn’t justify the nearly 4x sales valuation. And gross profit margins declined from 23% in 2021 to 18% in 2023, while net income margin fell from 35% to 5%, respectively.

Finally, have I mentioned that it’s a restaurant stock?

However, I believe these reasons are temporary. The founders still run the business; this is their first year as a public company. Learning how to set market expectations, engage with shareholders, and pitch your story will take time.

Also, the stock now trades at a $200M market cap or <0.7x NTM sales. That’s a much cheaper valuation than its IPO price of nearly 4x sales, even after accounting for “slower” 10% YoY growth.

What about the margin decline? Recent earnings calls suggest that the company is investing through the PnL today to enable the business to service more restaurants tomorrow.

It’s a short-term pain for long-term value creation.

But there’s another twist. Most of GENK’s stores today operate in California. California is one of the worst, most expensive places to do business. It should see a per-restaurant decrease in COGS and higher gross margins as the company opens more stores outside California.

Then there’s valuation. What if GENK is KRUS 2.0? How much can we make if we’re right?

GENK Valuation: 5-Bagger Potential

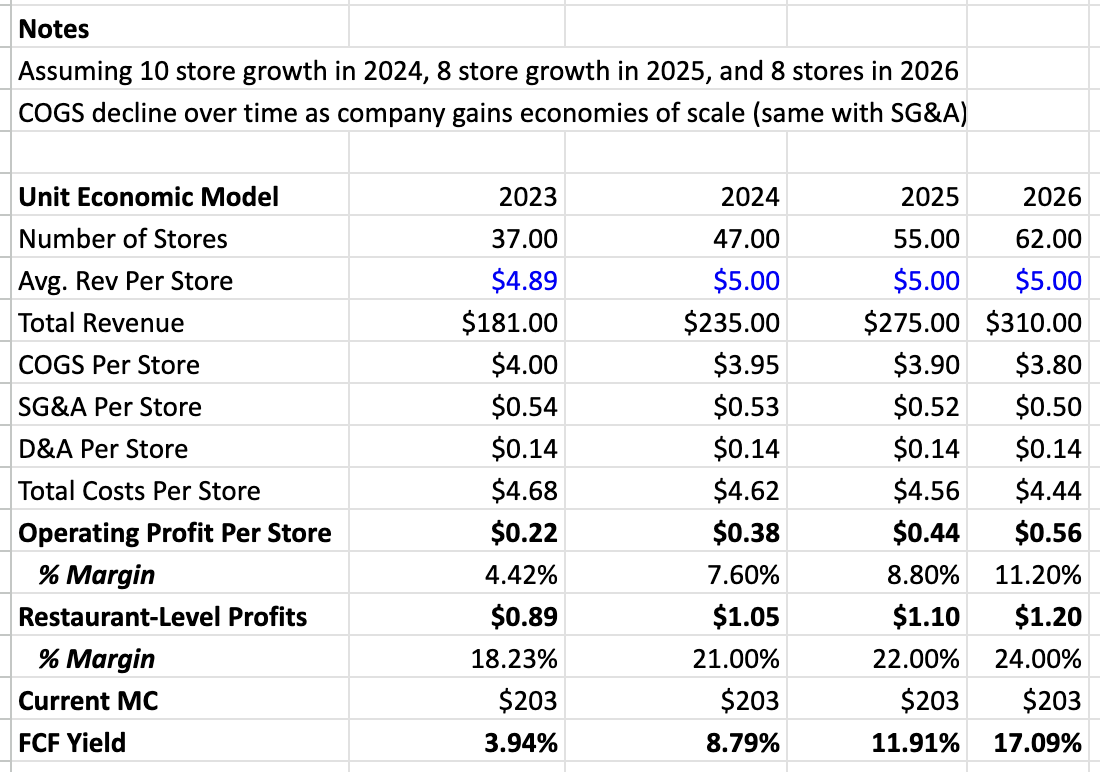

Let’s start with my back-of-the-napkin unit economic model (see below).

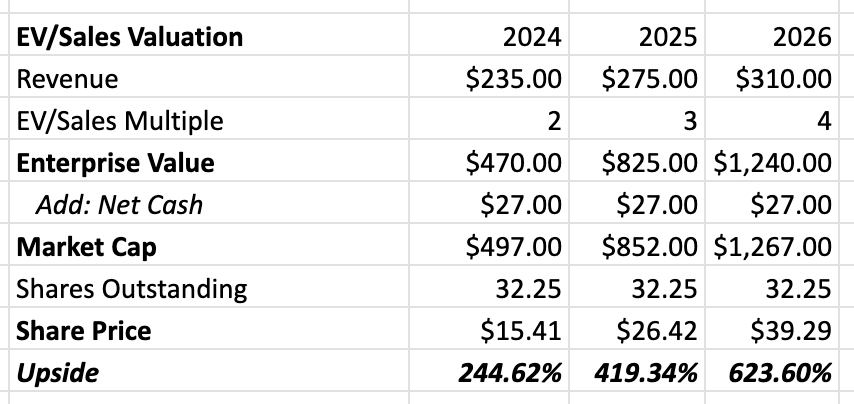

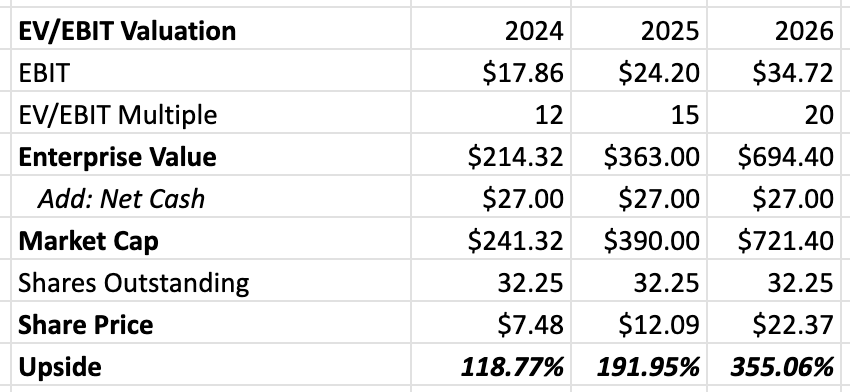

I’m assuming restaurant growth of 10 stores in 2024, 8 stores in 2025, and 7 stores in 2026 (fairly conservative). I also assume $5M in average annual revenue per store, which aligns with management’s estimates.

However, I assume that GENK gains economies of scale in lowering food prices (buying more for more restaurants), lowering labor costs as it shifts more stores outside California, and lowering SG&A as it spreads marketing across a larger restaurant base.

As the model shows, I estimate ~$310M in revenue by 2026 with ~$35M in operating profits at 11% margins. The math works out to ~17% annual revenue growth from 2023-2026 and EBIT margins in line with what the company generated historically.

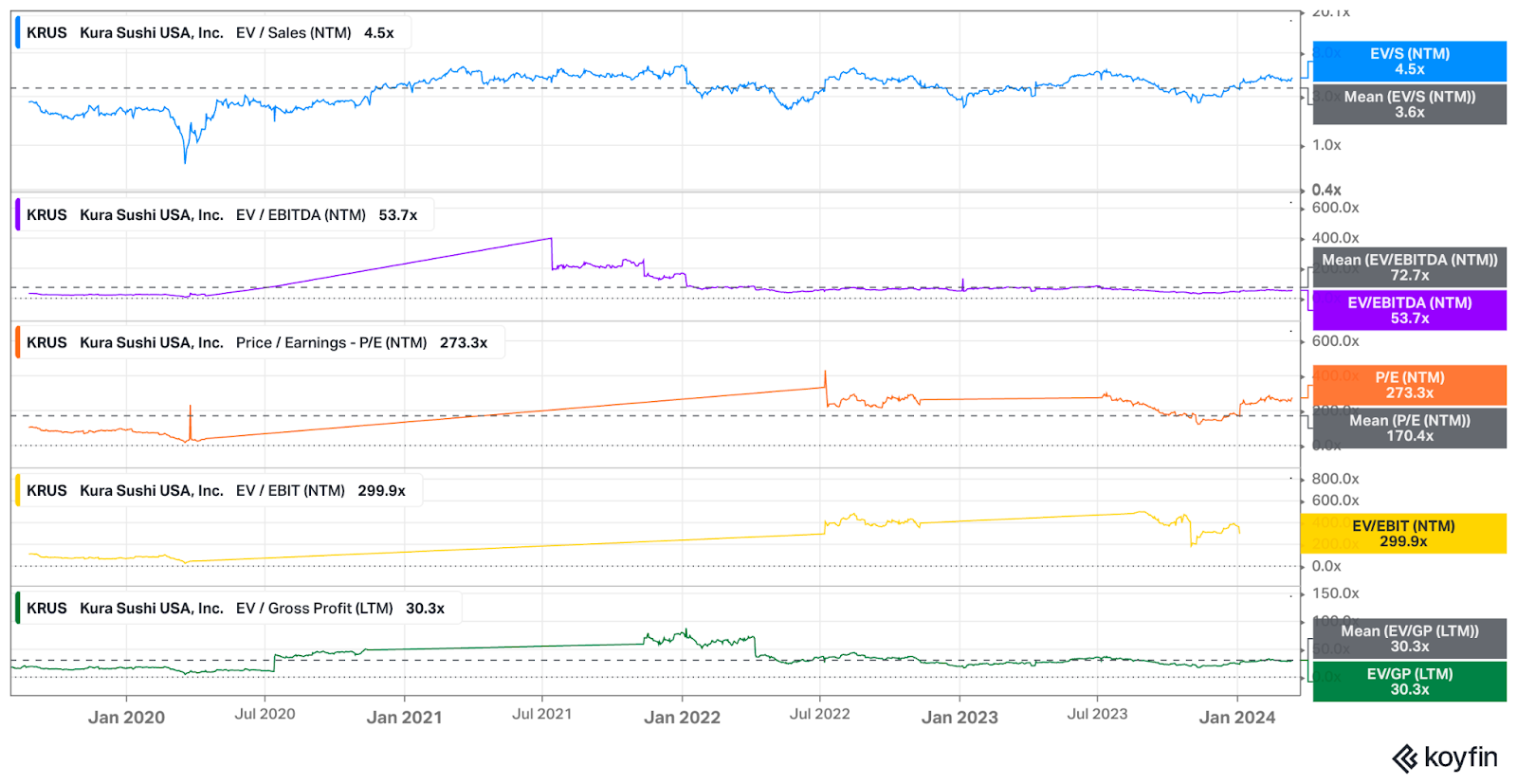

Investors will pay 3-5x sales and 15-20x EBIT for GENK. Just look at how they value KRUS (see below, chart via Koyfin).

Here’s what an EV/Sales valuation looks like.

And here’s the EV/EBIT version.

On average, GENK could be worth anywhere from $11.45/share to $31/share or 181% to 500% upside.

I want to stress two things. First, I don’t think the revenue and restaurant count growth assumptions are unreasonable. Store count growth is probably conservative.

Two, these valuation multiples aren’t outrageous, either. KRUS routinely traded above 5x NTM sales and over 30x gross profits. Texas Roadhouse (TXRH) historically trades at 25x EBIT and 12x gross profits.

GENK will have no problem commanding 3-5x sales and 15-20x EBIT if they can prove the concept works and the growth exists.

Conclusion: The Benefits Of Pattern Recognition

There’s a story about Buffett investing $5B in Bank of America because “he dreamt it up in the bathtub one morning.”

The lesson there isn’t to take more baths. But to understand the power of pattern recognition. Buffett knew bank stocks better than anyone. He knew what a good bank looked like and, more importantly, what a bad bank looked like.

So while the decision to invest $5B in BofA seemed to take a nano-second, it was decades of developing pattern recognition tools and mental models.

That’s how I feel about GENK and KRUS. I understood GENK in what felt like two seconds. But that’s because I did the work on KRUS. I already developed pattern recognition tools and mental models to analyze these situations.

That doesn’t mean GENK will work. But if it looks like a duck and walks like a duck …