Fix the roof while the sun is shining.

Q1 2020 hedge fund letters, conferences and more

Summary

- Tail risk funds tend to be most in demand when they are least attractive

- Short-term bonds provided similar benefits to tail risk funds

- The TAIL ETF closely replicates the performance of tail risk funds

Introduction

In a year where the S&P 500 lost more than 30% in a few weeks, there are few headlines that draw as much attention as these:

- This Black Swan Trade Saw 1,000% Profits This Week (MoneyMorning, 12 March 2020)

- Up 3,000%: The Tail Risk Funds That Mastered Coronavirus Market Mayhem (Reuters, 18 March 2020)

- Billionaire Bill Ackman Made 100-Fold Return On Coronavirus Hedge That Yielded $2.6 Billion (Forbes, 25 March 2020)

- Wimbledon’s Organizers Set For A $141 Million Payout After Taking Out Pandemic Insurance (Forbes, 9 April 2020)

Unfortunately for investors, by the time they read such headlines, the severe market dislocation that allowed to generate such abnormal profits has already happened. Volatility has spiked and credit default spreads (CDS) of companies or governments are no longer trading at cheap levels, as well as insurance premia.

Naturally, this does not mean that there might not be need for additional tail risk coverage since we might be facing a long bear or sideways market ahead. Investors can still reposition their portfolios for such a scenario, but the opportunity to buy inexpensive portfolio protection has passed.

It usually takes many years after a crash for markets to feature the unique conditions that provide the fertile grounds for stellar tail risk fund performance again. Investors need to be complacent about risk and ideally believe this time it is different for the price of protection to come down. Best on an epic scale like during the tech bubble in 1999 where standard valuation metrics like PE ratios were considered obsolete or during the US housing boom in 2005 where the assumption was that house prices can never decline on a national level.

However, although it might be too late for investors to consider tail risk funds currently, recent events provide a good framework to evaluate how well these have protected portfolios historically.

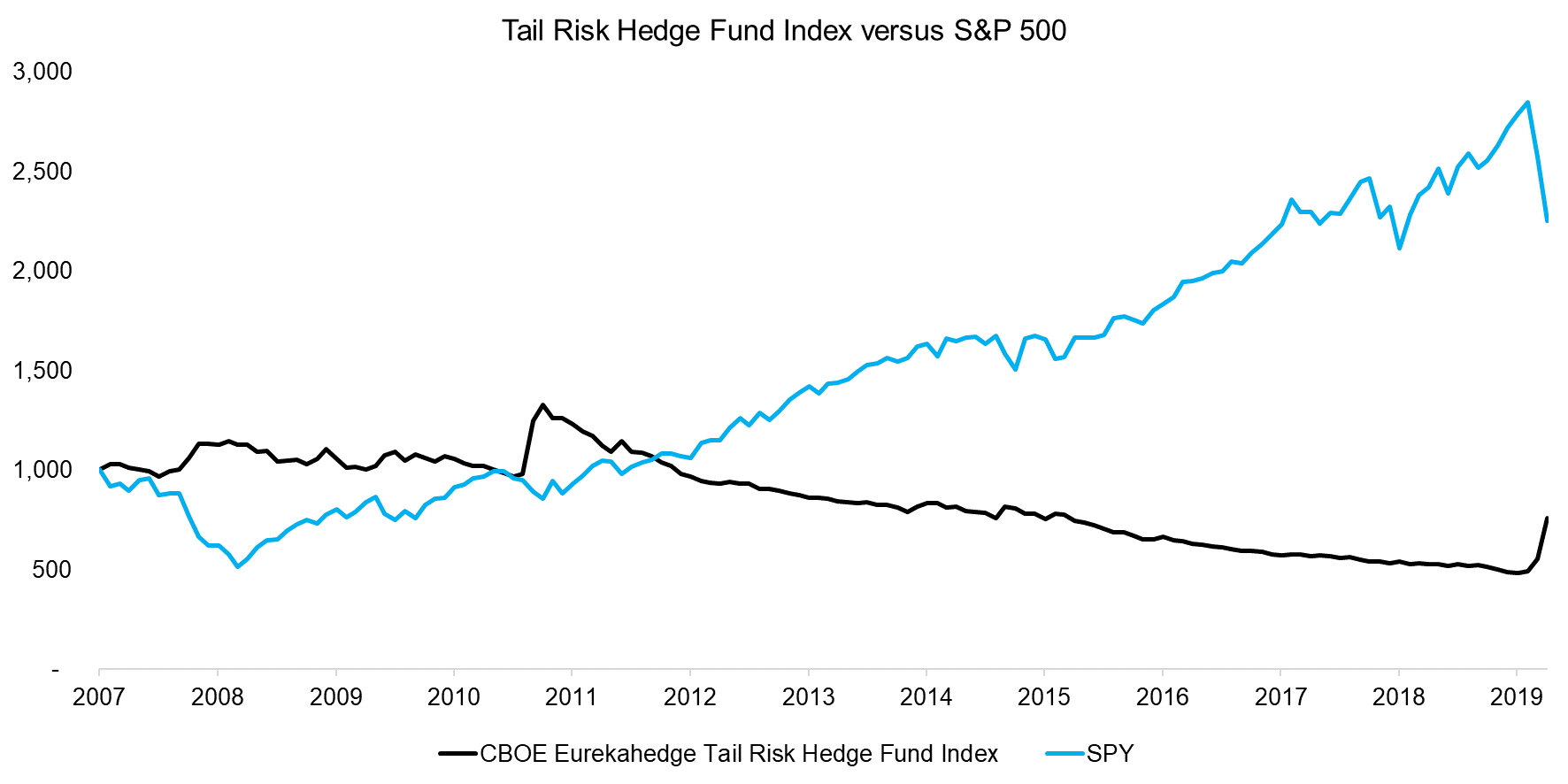

CBOE Eurekahedge Tail Risk Hedge Fund Index

Tail risk funds primarily use complex financial instruments like options or CDS to structure portfolios against a market downturn, which makes them less well-suited for mutual funds and more adequate for hedge funds or similar investors comfortable with the use of sophisticated instruments.

The CBOE Eurekahedge Tail Risk Hedge Fund Index (“Tail Risk Index”) is one of the few time series available in the public domain and provides data from 2007 onward, which therefore includes two major stock market crashes. The data should be viewed with caution as the index only contains few constituents. As of March 2020, the index was comprised of eight funds from asset managers like 36 South Capital Advisors and Capstone Investment Advisors, which are dedicated to hedging tail events.

We observe that the Tail Risk Index exhibited an almost perfect asymmetrical profile to the S&P 500 in the period from 2007 to 2020. Although investors would expect the index to show positive returns when the stock market declines dramatically, ideally tail risk funds should not lose much money at other times. However, between 2011 and the onset of the coronavirus crisis, the index generated consistently negative returns and accumulated a 60% loss. This is in part due to the compounding effect of small losses over such a long period of time between crises periods.

The performance of the Tail Risk Index highlights the challenge of investing in such strategies as they are mostly losing money and only generate positive returns in very short time periods, more likely days rather than weeks. Such a product is clearly unsuitable for retail investors and even most institutional investors struggle with the highly skewed returns.

There is no public data on the total assets under management in tail risk funds, but it is likely a rounding error compared to the assets in long-only strategies. Universa Investments, which is one of the well-known and largest players in the space, manages $5 billion. In contrast, there are approximately $3 trillion invested in US equity ETFs and multiples of that in equity mutual funds.

Source: Eurekahedge, FactorResearch

Tail Risk Funds For Portfolio Protection

Portfolio protection has had a bad reputation since the stock market crash in 1987, where automated selling programs designed to protect portfolios are often held as the culprits for the crash. Most investors prefer to diversify equity portfolios by investing in bonds, commodities, or alternative asset classes like private equity or real estate.

However, bond yields globally have reached extremely low levels, which reduces expected returns and makes them less attractive for diversification than historically. Similarly, private equity and real estate provide equity exposure with lagged valuations that only offer uncorrelated returns on paper. Although painful to hold, tail risk funds may be more attractive for portfolio protection going forward.

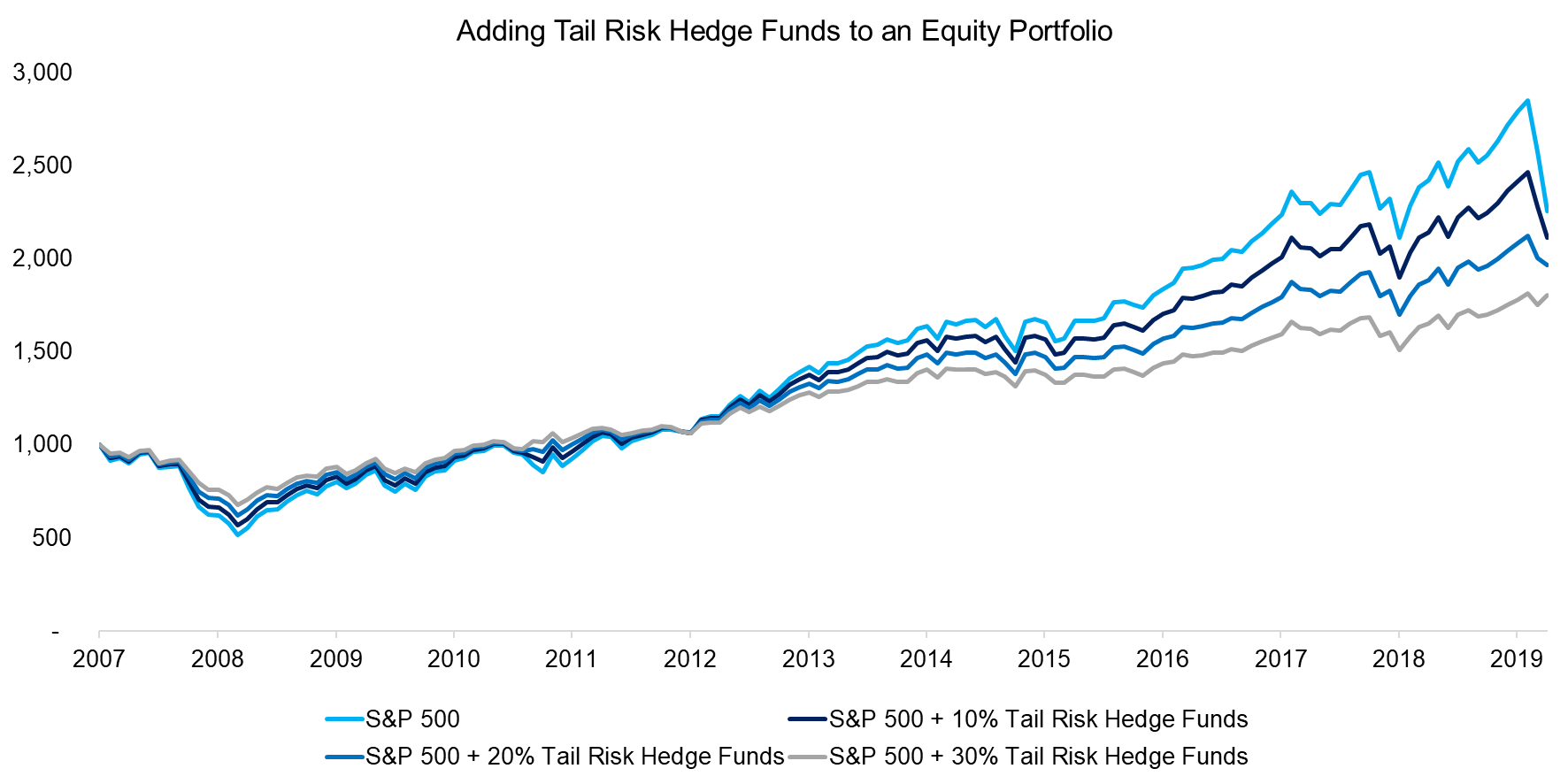

We start our analysis by simulating the performance of an equity portfolio comprised of the S&P 500 and an allocation to the Tail Risk Index, rebalancing annually. The results highlight the larger the allocation to tail risk funds, the lower the total return in the period from 2007 to 2020. However, we can also observe that the drawdowns during the global financial crisis in 2008 to 2009 as well as during the coronavirus crisis in 2020 were reduced, which fulfills the core objective of tail risk funds.

Source: Eurekahedge, FactorResearch

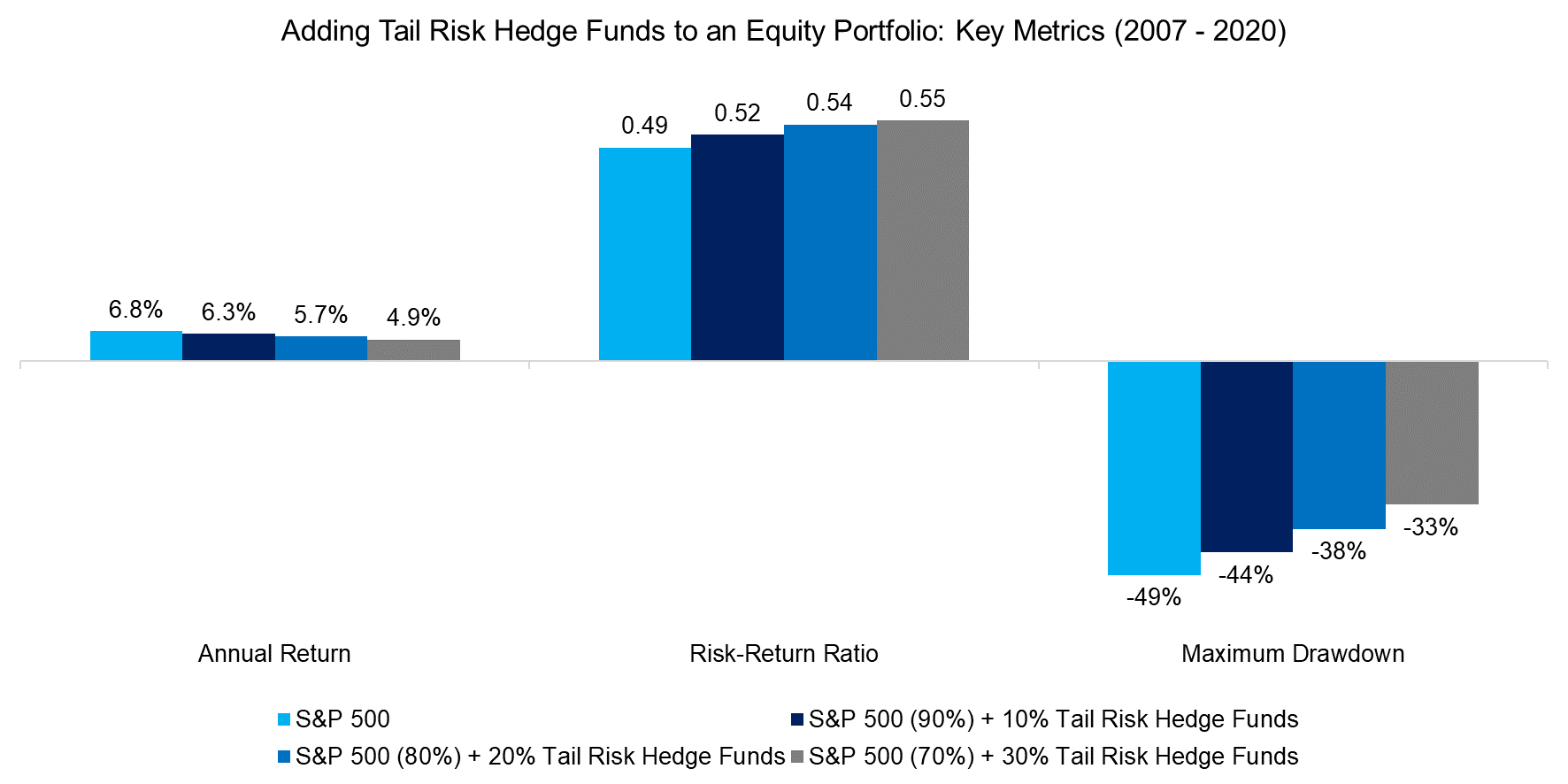

Next, we switch the perspective to risk-adjusted returns, which highlights that the larger the allocation to tail risk funds in an equity portfolio, the higher the risk-return ratios. We observe a decline in the return as expected, but also a corresponding one in the maximum drawdown. The pain-to-gain ratio, which is defined as the return divided by the maximum drawdown, is almost identical across the different portfolios.

Source: Eurekahedge, FactorResearch

Although tail risk funds did reduce maximum drawdowns of equity portfolios during market crashes, the increase in risk-adjusted returns was moderate. A skeptical investor might question if they provided more benefits than a cash allocation. Also, the same skeptical investor could make an argument that tail risk funds are not devoid of default risk. Taking this argument to the extreme, one might remember the experience with catastrophe bond issuers that collected payments during good times only to default when disaster struck.

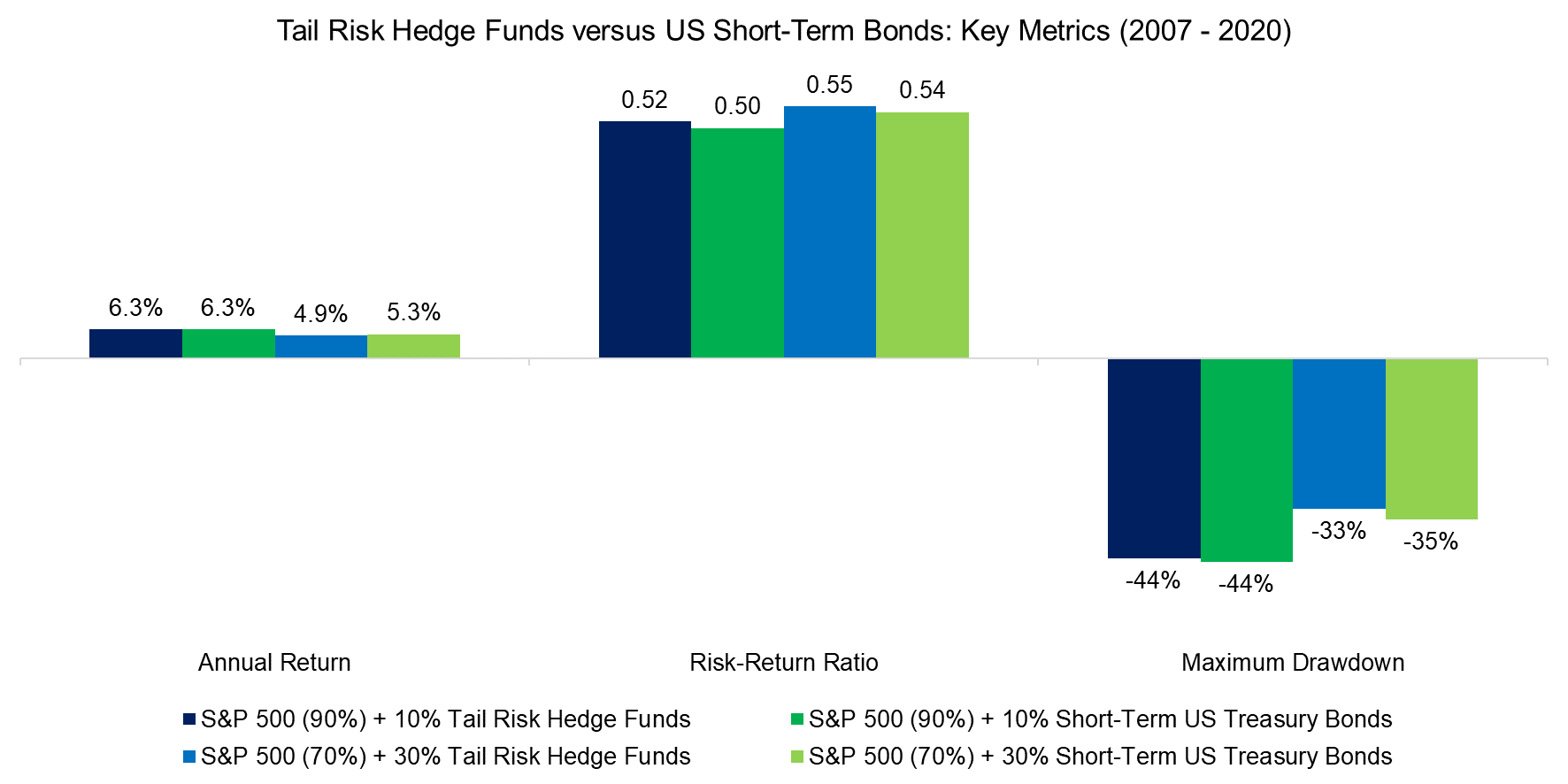

We use short-term US treasury bonds as a proxy for cash and contrast an allocation to these compared to tail risk funds. The analysis highlights that there was little benefit to investing in tail risk funds compared to short-term bonds as both resulted in similar risk-return ratios and drawdowns in the period from 2007 to 2020.

It is worth noting that we could have alternatively used long-term US treasury bonds, which would have showed even better diversification benefits as they were largely negative correlated to equities in the recent decade and therefore provided excellent crisis alpha. However, given that the 30-year bond market rally has peaked with yields close to zero, these are likely less attractive going forward.

Source: Eurekahedge, FactorResearch

One of the challenges of analyzing tail risk funds is the diversity of strategies. These can be discretionary or systematic and be expressed via various financial instruments, which results in a large dispersion of returns. The strategies are complex and require significantly more due diligence than other investment products. Furthermore, market crashes occur only every few years, therefore there are few data points where asset managers can prove that their strategies have created value.

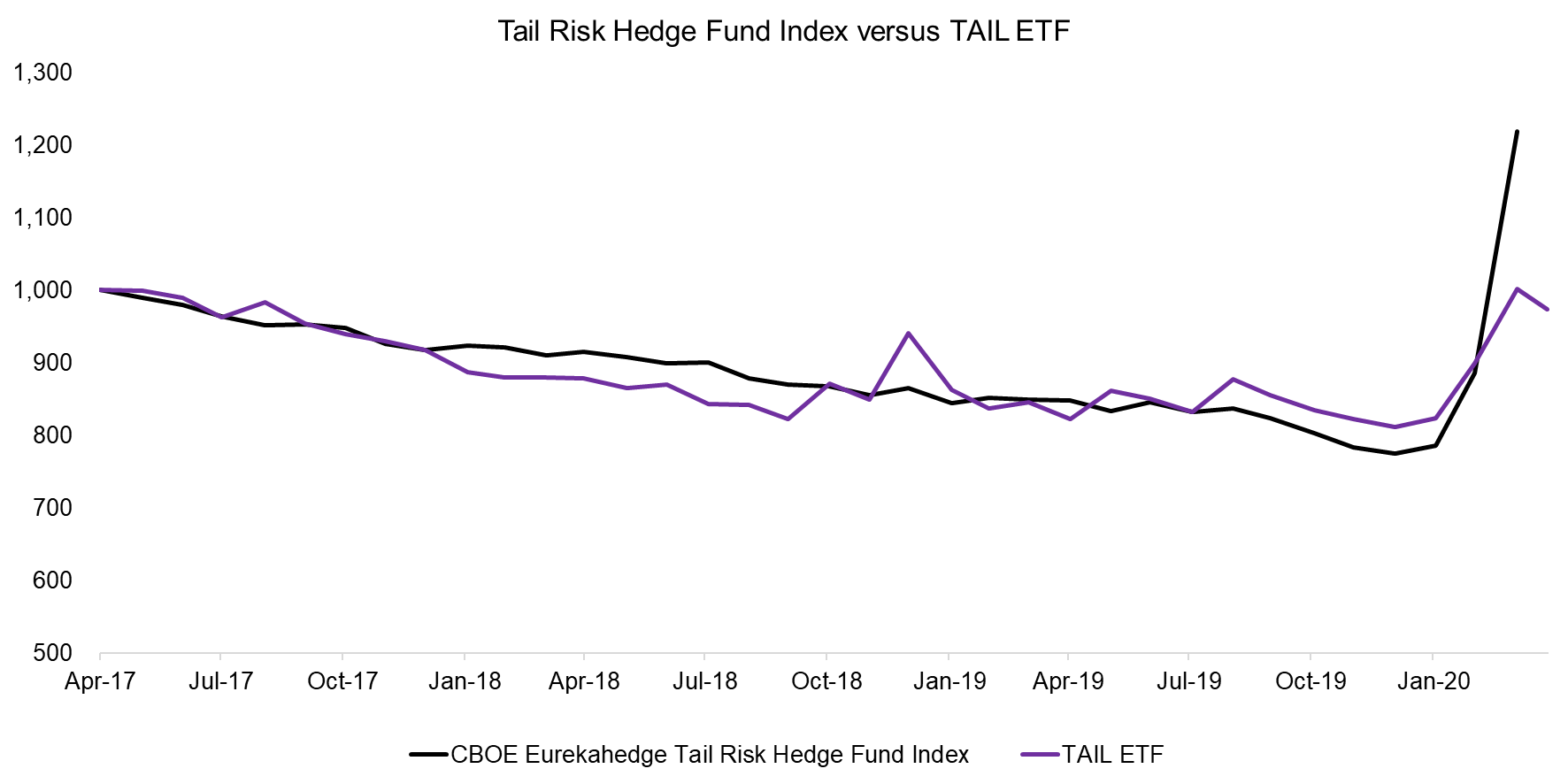

However, instead of selecting individual strategies and investing in funds that are typically structured as hedge funds, investors can consider Cambria Investment’s TAIL ETF (“TAIL”). The product offers daily liquidity, is trading on a regulated exchange, charges 0.59% per annum, and provides exposure to out-of-money put options on the US stock market. TAIL was launched in April 2017, so there is limited data history, but since then it has tracked the Tail Risk Index closely.

It is worth noting that it takes some tail risk hedge funds almost a month to report their performance data to databases like Eurekahedge, which is surprising given that they use traded instruments to create portfolios. We observe that TAIL declined in April 2020 as markets recovered, which provides an estimate on how tail risk hedge funds performed.

Source: FactorResearch

Further Thoughts

A tail risk fund is somewhat like a roller-coaster at Disneyworld in Florida: the experience is primarily waiting uncomfortably for a long time in sweltering heat rewarded by a few brief moments of glorious joy.

Investors that are seeking a strategy that does generate positive returns on the few days where markets are crashing and volatility is spiking are likely well-served by tail risk funds. However, although almost every investor prefers V-shaped recoveries, market crashes have turned into market downturns. In the case of the Japanese equity market, there has not been a recovery since the crash in 1989. Investors are likely better served by strategies that structurally offer diversification for an equity portfolio rather than a few days of joy.

Related Research

Hedging Market Crashes with Factor Exposure

Low Volatility vs Option-Based Strategies

Hedging via Managed Futures Liquid Alts

About The Author

Nicolas Rabener is the Managing Director of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Article by Factor Research