Introduction

My personal anecdotal experience suggests that many investors operate under the fallacy: “my mind’s made up – don’t confuse me with the facts.” This behavior often results from only reading the headlines while skimming over the in-depth analysis that is truly needed to make a sound or prudent investing decision.

Q1 hedge fund letters, conference, scoops etc

A current case in point is the attitude towards brick-and-mortar retail that many investors currently hold. Commonly referred to as “the Amazon effect,” many investors believe that brick-and-mortar retail is dying, and all sales will soon be done only online. Moreover, many investors go as far to believe that Amazon will be the only retail outlet left standing when all is said and done. However, I would personally argue that retail is experiencing a transformation, but not an apocalypse as many people fear.

This opinion was recently shared by Wall Street Journal news editor Lee Hawkins in the video titled “Why There’s No Retail Apocalypse.”

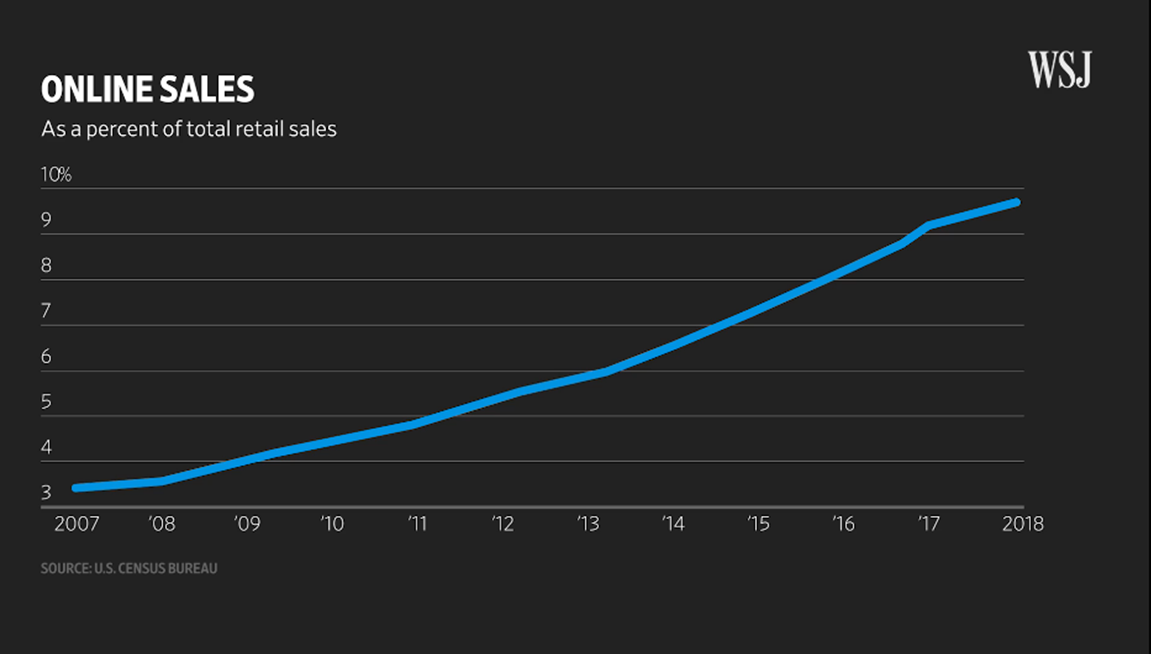

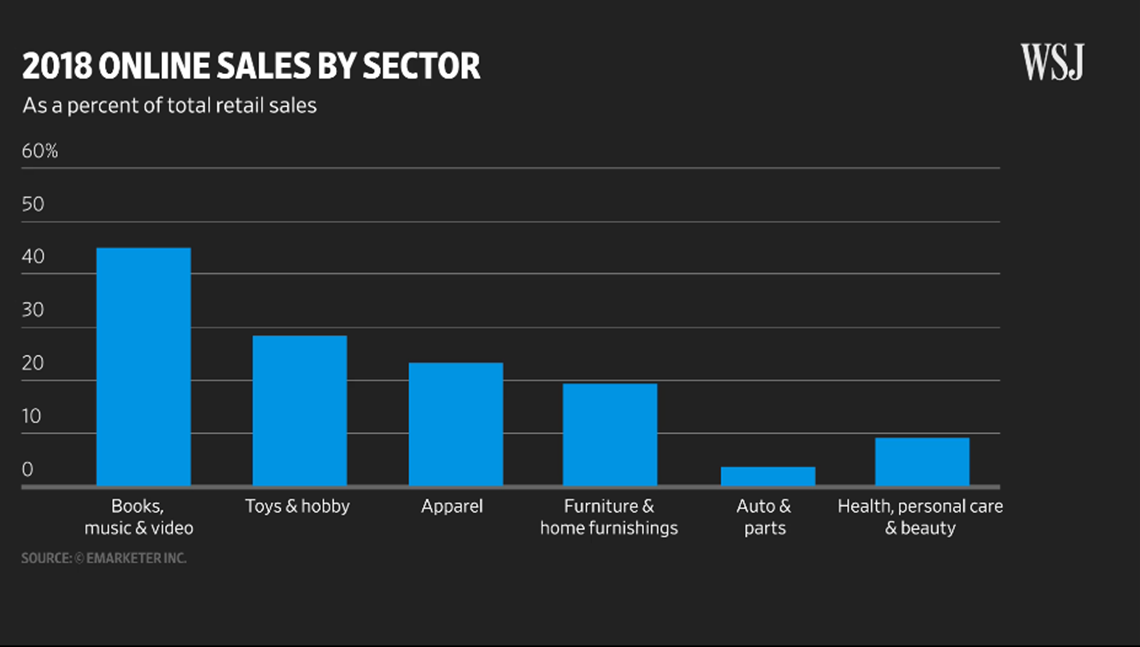

As the video pointed out, online sales are growing significantly faster than brick-and-mortar sales. However, even though they are growing faster, they still only represent approximately 10% of total retail sales. Therefore, 90% of all retail is still conducted in stores as evidenced by the two screenshots from the video below:

However, it is only fair to point out that certain sectors are more susceptible to online purchases than others. As I often say, the devil is in the details, but so are the angels. Consequently, I believe it’s important to not just skim over the headlines, but also to dig deeper into the details.

The Death of Brick-And-Mortar Retail Is Greatly Exaggerated

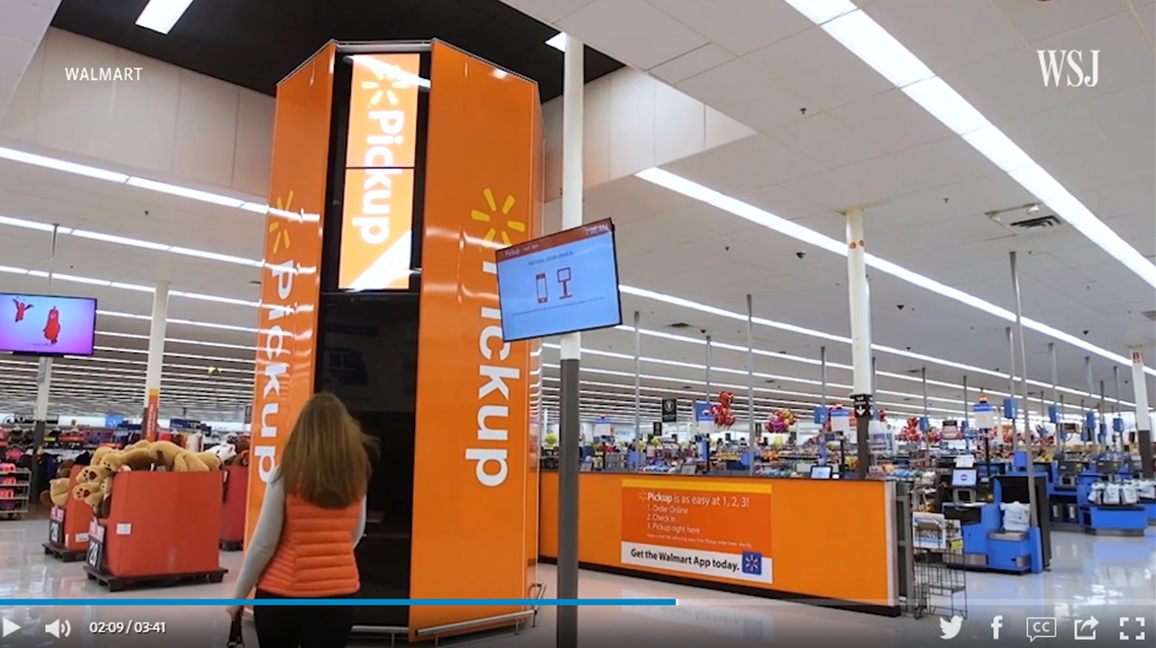

Moreover, I think it’s also important to consider that prominent brick-and-mortar retailers are not complacently standing by. Instead, they are also developing their own online businesses. Therefore, I believe this supports the reality of a transformation rather than a retail apocalypse. Furthermore, I think it’s also important to recognize that retail is an industry that has constantly experienced transformation as technology has evolved and developed. Think big box retailers such as Home Depot and/or Lowe’s, or more to the point of this article – Walmart and Target.

As the following screenshots from the video illustrate, both Target and Walmart are aggressively developing online businesses of their own to include in-store pickups and same-day delivery.

However, the online commitment that these brick-and-mortar retailers are making doesn’t just stop with themselves. Walgreens is even partnering with companies such as Levi that allow customers to order online and pick up the merchandise at Walgreens’ stores. If the merchandise does not fit, the customer can return it directly through Walgreens thereby avoiding the hassles of taking it to the post office.

Furthermore, according to JLL research e-commerce retailers that were born online plan to open 850 brick-and-mortar stores in the next 5 years. Therefore, I believe the evidence is clear that brick and mortar is not going away. Instead, there is truly a retail transformation that includes both brick and mortar as well as online retailers.

Even Amazon is entering the brick and mortar space. Amazon Go is a new kind of retail store that features advanced shopping technology with no lines and no check out. Shoppers simply activate their app and each purchase is recorded and charged.

Consequently, in conjunction with the Wall Street Journal video report, the retail apocalypse looks more like a retail transformation. Retail is clearly changing, but brick and mortar retail appears to continue to have a place in the equation. But most importantly, every major brick and mortar retailer is developing their own online presence as well.

Target Not Just Surviving – Prospering

Despite all the doom and gloom surrounding brick and mortar retailers, Target (TGT) continues to prosper. Operating earnings grew 14% in fiscal year ending January 1, 2019, and they are expected to advance another 10% in fiscal year ending January 1, 2020.

Target’s Q1 2019 earnings report produced more of the same with both GAAP and adjusted EPS up more than 15% for the quarter. Target believes that they have built a durable model that is relevant to consumers and sustainable going forward.

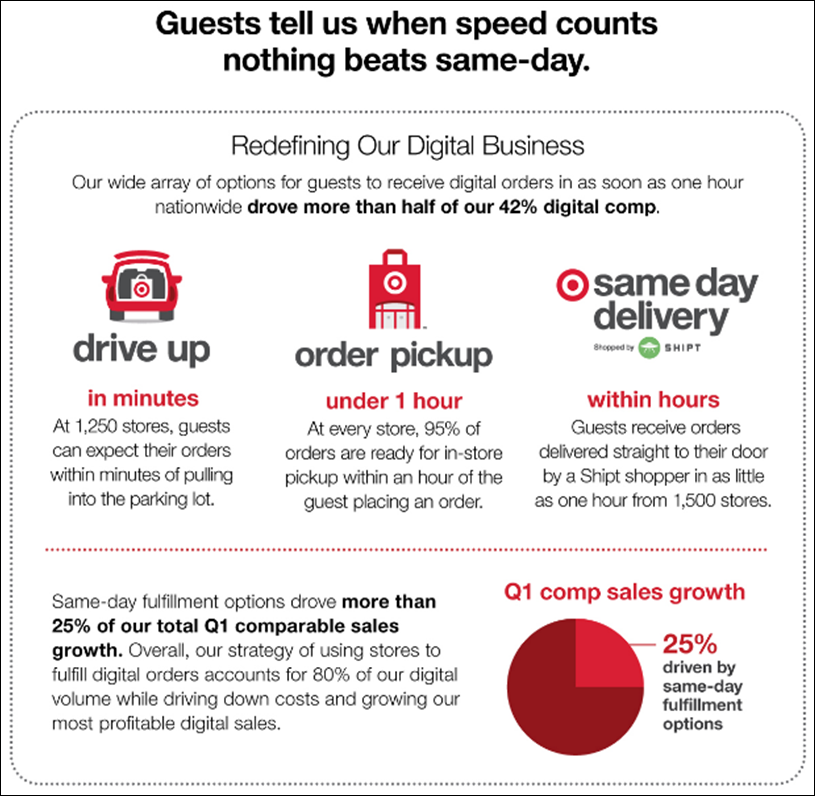

Target has produced 42% growth in their digital business and attributed it to service and convenience. Customers can quickly pick up orders at the store or receive same-day delivery. Although digital accounted for $5 billion of Target’s approximately $75 billion in sales last year, it still represents a small portion of their overall sales.

Target remains committed to their 1800 brick and mortar stores that are located within 10 miles of three quarters of the American population. Therefore, they plan to continue remodeling 300 stores a year that keep them on track to complete a thousand remodels by the end of next year.

Although the brick and mortar retail space is constantly transforming, Target remains committed to keeping their stores and their online sales relevant to their customers. The retail environment is clearly changing, and Target has been committed to reinventing itself in lockstep with those changes. You can learn more about all of these initiatives by reading their 1st quarter 2019 financial news release found here.

Target is Fairly Valued

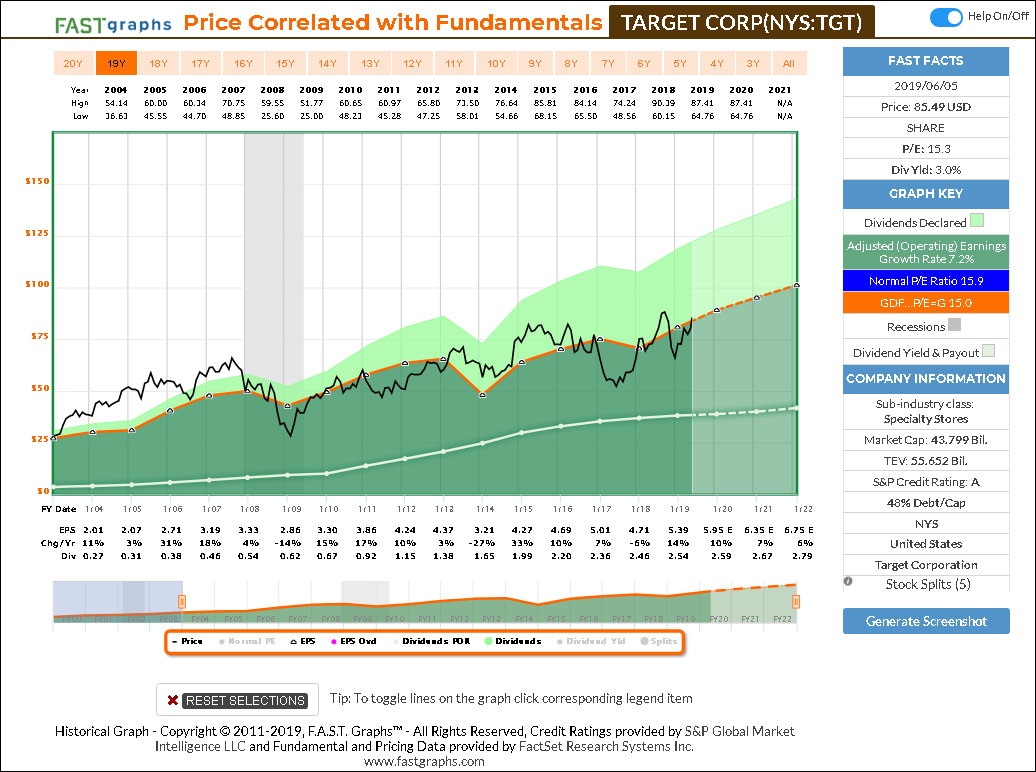

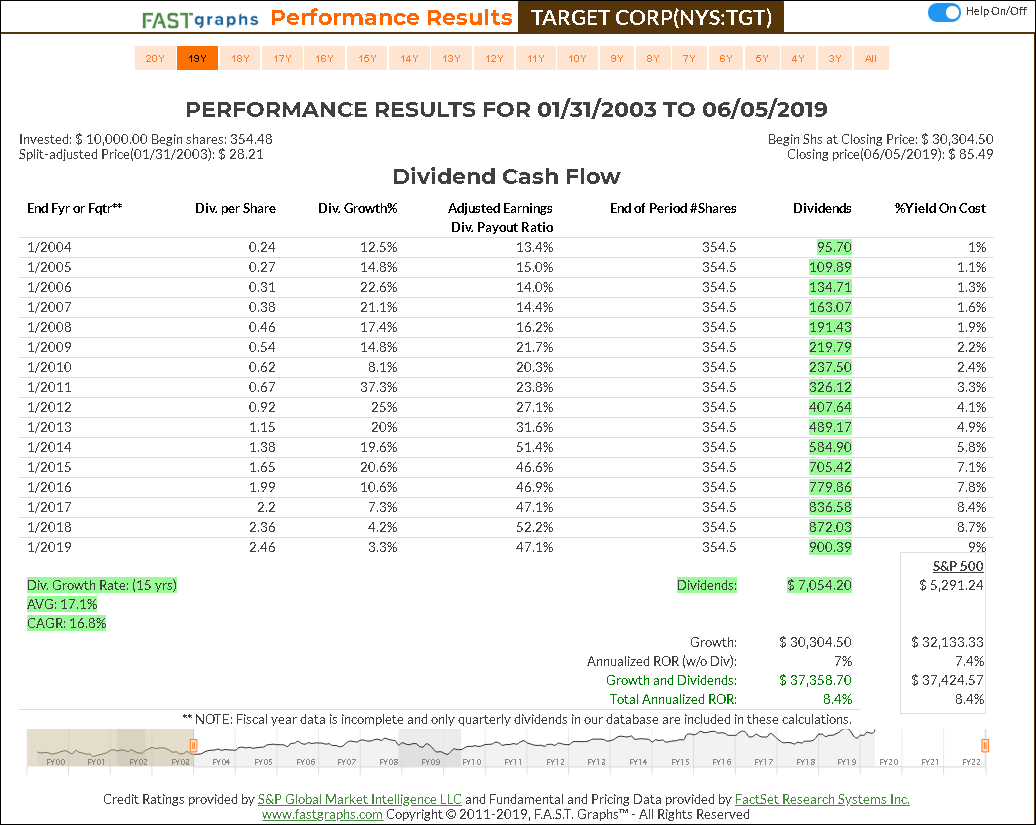

When purchased at sound valuation, Target has mirrored the S&P 500 on a total return basis since the beginning of 2003. However, for the focused dividend growth investor, Target has produced significantly more dividend income than the S&P. Consequently, I believe it is advantageous for dividend growth investors to purchase Target when valuation is sound as it is today.

But, with that said, the best time to purchase any quality company is when you can find its shares available on sale – as Target’s were at year-end 2018. Although that was a time to “be greedy when others were fearful” Target remains a prudent investment today. For those that are motivated to beat the market over time, Target offers a 3% current dividend yield versus a 2.1% current yield for the S&P 500. Moreover, Target is currently fairly valued with a blended P/E ratio of 15.3 versus a fully valued S&P 500 trading at a blended P/E ratio of 17.9.

Target: Thesis for Future Return

Personally, I believe Target currently offers a high quality, prudent and attractive long-term investment for both above-average dividend yield and total return. However, as I’ve written many times before, I do not embrace merely having a vague idea of what an investment in a stock might bring me. Of course, I understand that my future return expectations cannot be calculated with perfect precision, however, I believe they can be forecast within a reasonable range of accuracy.

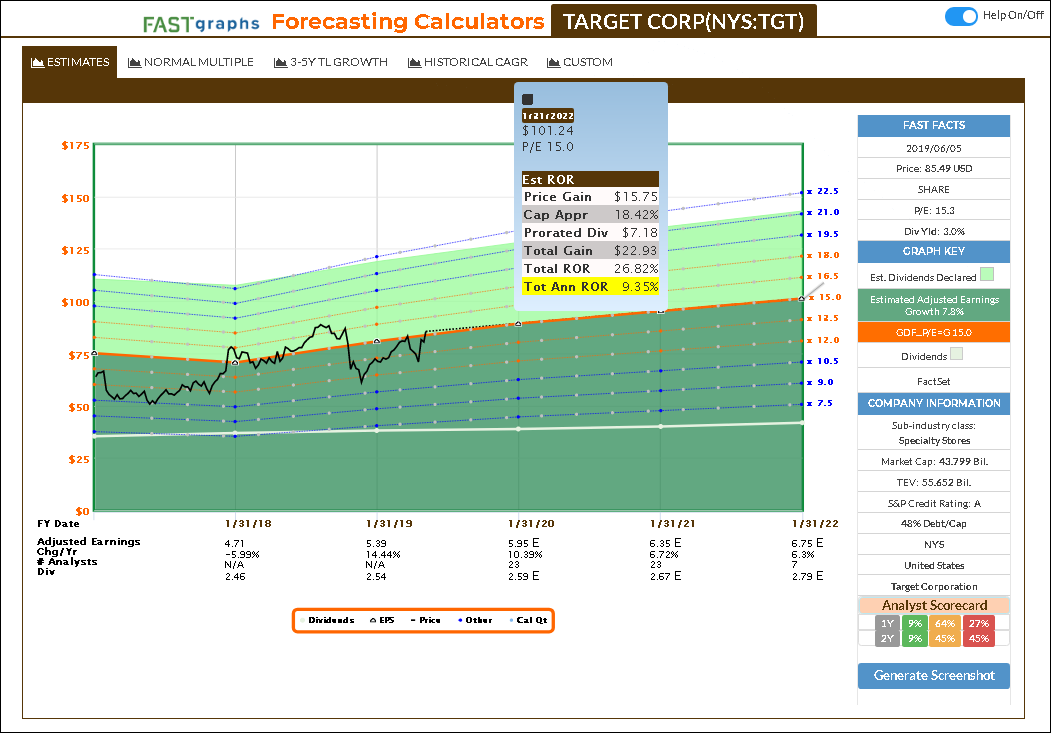

Consequently, I utilize the calculator function of the FAST Graphs forecasting tool in order to run the numbers out to their most logical conclusion. In the case of Target, I would expect rates of return exceeding 9% per annum over the next several years based on reasonable forecasts of forward growth. Although the following screenshot depicts this, I will be providing greater detail in the FAST Graphs analyze out loud video that follows.

Target: FAST Graphs analyze out loud video

Summary and Conclusions

I like Target at today’s current valuation. However, I don’t love it like I did at the beginning of this year. Nevertheless, even though the stock has risen almost 30% since the end of December 2018, I would argue that it has moved up from significant undervaluation to its current fair valuation. Moreover, I like the company’s quality and I like the management team that I see committed to not only their customers, but also their in-store associates. But perhaps most of all, I like the company’s willingness and commitment to staying current with the transforming retail environment.

Nevertheless, investors should also recognize that Target – as well as many other retailers – are faced with a very challenging retail environment and intense competition going forward. Regardless, I do believe that Target is up to the challenge. However, I leave it up to each individual investor to decide for themselves. Caveat emptor.

Disclosure: Long TGT.

Article by F.A.S.T. Graphs