I believe yesterday’s RNS released by Tharisa. They are buying out BEE minorities stake in the South African Mine for $26.5m by issuing 13 903 743 new shares. I wrote them up here (when the Rhodium price was much higher). I think the share price isn’t reflecting the amount of value they have obtained from this transaction.

Q4 2021 hedge fund letters, conferences and more

BEE stands for Black Economic Empowerment – in essence, blacks get richer by transactions depriving non blacks of their money/assets (a harsh eplanation – more balanced one is here). I understand where they are coming from but ultimately it is not in my financial interest.

I believe this is an absolulte bargain. The Tharisa Minerals minority last year earnt $38.5m – so in essence it is being bought for a year and a bit’s profits – this depends greatly on your expectation of next year’s earnings. I am going to use last year’s to simplify this as I believe it hasn’t been fully understood by the market or reflected in the share price.

Sp 38.5m in 2021 went to the minorities. (p103 2021 annual report here)

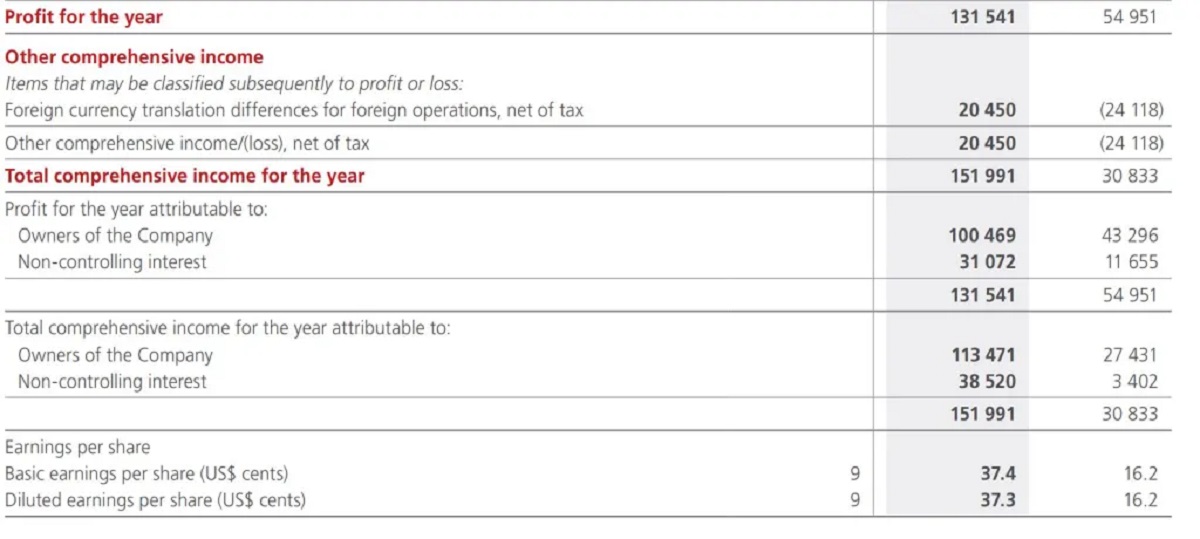

Next we go on to the effect on earnings per share (p117).

So with the 13.9m new shares we get 269,458,000+13,903,743 so 283,361,743.

Earnings go up from $100.469m to $131.541m – so headline EPS goes up from 38.3c to 46.4c – a 21% increase

On announcement of this news yesterday the share price rose from 136.5 to 145 now (@13.26 17/2/2022) – this is a c6.2% rise.

There is no logic I am aware of for this limited price move. Some on ADVFN suggest this is just a proposed transaction but the RNS says the agreement is concluded. There are conditions on the trust but this is only 6% of the holding or 3.2m shares.

I think this is an instance where a mid-day RNS was misread / not fully thought through – creating an opportunity for the sharp. I have bought more – Tharisa is now my largest position – an 8% weight. I intend to sell once the price rises to reflect the good news.

It isn’t like the company is expensive, it is on a forward PE of about 4, with healthy margins at current PGM prices. They likely have $80m cash available with no net debt. The current Rhodium price is not where it was this time last year – c 25000 but is still healthy. There may be scope for the rhodium price to rise – it’s used in catalytic converters and due to chip shortages production is down. These are anticipated to ease in 2022/2023 . They are also guiding more production in 2022.

I’d suggest if you are interested in doing this you jump on ASAP – these sorts of opportunities don’t hang around for long.

One last note (don’t usually do this) – am trying to raise money to buy a defibrillator for the gym I go to (excess . Donations would be appreciated… Think how much money (some of you) make from my ideas and how much you would miss them if I died due to overexertion / lack of a defibrillator.

Link to donate is here.

Tharisa – mispriced following minority buy out, very low risk opportunity.

Article by Rob Mahan, Deep Value Investments Blog