Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Q3 2019 hedge fund letters, conferences and more

As two recent commentaries demonstrate, in their zeal to promote their agendas, asset managers are claiming that the humble 60/40 portfolio is doomed to the dustbin. But their analysis is flawed. The 60/40 will outlive us all.

Let’s start with a recent Yahoo Finance article titled 60% stocks and 40% bonds…not so fast, which caught my attention. The theme? “The simplest investing idea in the world may have died…60% stocks and 40% bonds…” Then, for drama, the editor included a photograph of a mock 60/40 graveyard with “RIP” on the tombstone.

He continued: “The traditional 60/40 mix, which has returned about 6% a year since 1970…might not be enough to generate the returns that investors have come to expect.”

Well, that explains it.

Except he is wrong.

The traditional 60/40 mix (60% U.S. stocks, 40% U.S. bonds) has not returned 6% a year since 1970. It returned around 9.3% yearly from 1970 through 2018. If it seems he didn’t miss it by much, an investment that returned 9.3% yearly would return 350% more cumulatively than an investment that returned 6% during this 49-year period.

However, even if he knew 60/40 returned 9.3% (he didn’t realize that the source he cited was after inflation), he would have written the same story. He felt so comfortable piling on the humble balanced portfolio that, no matter what the returns, he would have found an agreeable audience – or one oblivious to returns and fact checking.

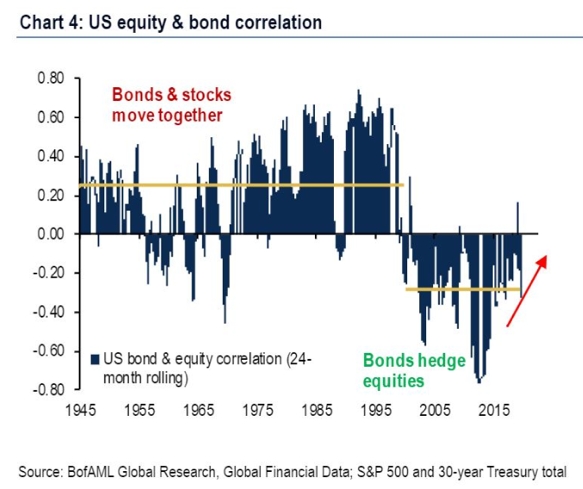

Take Bank of America, which published a recent note called The End of 60/40. Authors Jared Woodard and Derek Harris, its global research portfolio strategists, wrote ominously,

The core premise of every 60/40 portfolio is that bonds can hedge against risks to growth and equities can hedge against inflation; their returns are negatively correlated…But this assumption was only true over the past two decades and was mostly false over the prior 65 years. The big risk is that the correlation could flip, and now the longest period of negative correlation in history is coming to an end as policy makers jolt markets with attempts to boost growth.

Here is how they illustrated it.

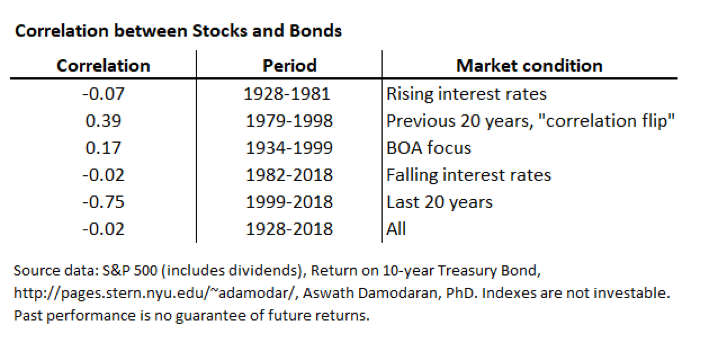

Unfortunately, the math does not add up here either, though they are correct that correlations were negative (-.75%) between stocks and bonds in the last 20 years. As shown below, during six comparative periods the correlation was only .17 for the BOA 65-year focus period (1934-1999) and was negative during rising and falling interest rate environments.

Correlation is a linear measure of two or more variables – in this case returns of stocks and bonds. A perfect negative correlation would result if stocks were up 10% and bonds were down 10%. This would be a great hedge but a lousy investment; you would never make any money.

Read the full article here by Andy Martin, Advisor Perspectives