Last week, we introduced the characteristics of a reserve currency, including a discussion of the costs and benefits of providing the reserve currency. This week, we will conclude the report with a short explanation of the S.W.I.F.T. network and its importance to international finance. From there, we will discuss the potential competitors to the dollar as the reserve currency, examining the possibility of competing trade blocs. As always, we will conclude with potential market ramifications.

Q3 hedge fund letters, conference, scoops etc

The S.W.I.F.T. Network

The Society for Worldwide Interbank Financial Telecommunication (S.W.I.F.T.) is a cooperative that operates a worldwide financial messaging network; its purpose is to allow financial institutions to easily and safely exchange messages. It was created in 1973 to replace the Telex and currently connects over 10,000 financial institutions in 210 countries. Headquartered in Belgium, it has 23 offices in major financial centers around the world and is overseen by the G-10. Although media reports suggest it is a money wiring service, this is not exactly accurate. It is a messaging service; it securely transmits information about accounts and transactions between institutions. Once a bank receives instructions via S.W.I.F.T., it can safely transfer funds to a corresponding bank. Without S.W.I.F.T., a bank would be hard pressed to determine if instructions were legitimate. Isolating Iranian financial institutions from S.W.I.F.T. would make it nearly impossible to safely move funds into or out of Iran. The U.S. was able to push Iran out of the system in 2012, but it returned in 2015.

The Trump administration wants Iran removed from the network by November.1 However, the U.S. doesn’t control the network. Instead, it is a private company with its own board of directors2 that will decide whether or not to remove Iran from the platform. S.W.I.F.T. is caught in a tough spot because it generates revenue by expanding its network as broadly as possible. If users are constantly worried about American sanctions preventing them from conducting trade with some nations, it will increase the attractiveness of an alternative messaging platform. At the same time, S.W.I.F.T. does not want to run afoul of the U.S. If Iran continues to use the platform, the U.S. could not only sanction the firm but could, at least in theory, sanction the network as well.

The Contenders

Historically, the hegemon provides the reserve currency as part of its hegemonic role. As we discuss below, there is the potential for regional reserve currencies. In this section, we will focus on potential replacements for the dollar.

The euro: In theory, the euro should be a strong candidate for replacing the dollar. If the Eurozone were a single nation, it would have the third largest economy in the world. In fact, the president of the EU Commission, Jean-Claude Junker, has recently called for the euro to replace the dollar.3 Here are the

primary impediments to the euro taking on this role:

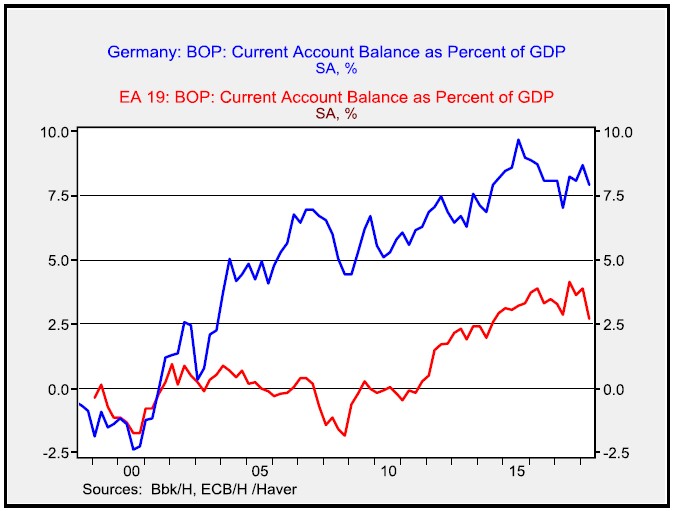

The preference for current account surpluses: The reserve currency nation must run current account deficits to supply the world with its currency. Because of Germany’s dominance of the Eurozone, it

isn’t likely the Germans would tolerate persistent current account deficits.

Since the creation of the Eurozone, Germany has been running current account surpluses. Its response to the “PIIGS” crisis4 was for these nations to implement austerity and export their surplus saving to the world. Simply put, Germany sees the world as a source for offloading its excess saving and until that policy changes the Eurozone won’t be willing to supply euros to world markets.

The lack of a unified financial system: The reserve currency nation must have a deep financial system with a plethora of available debt instruments so nations have a place to “park” their reserves in a safe asset. The U.S. offers the world Treasuries; although not all credit agencies give the bonds a AAA rating, in practice, it is actually considered an adequately safe investment.

There is no sovereign bond in the Eurozone backed by the full faith and credit of all its members. Germany has prevented the creation of such an instrument, fearful that countries would take advantage of the low interest rates that such a powerful instrument would offer and borrow too much. The ensuing debt service problems would fall on German citizens. Simply put, Germans don’t want to create a bond with their name on it that Italians could borrow in. And so, if a nation wants to use the euro for reserve purposes, it has to choose a particular Eurozone member nation bond. That limits the attractiveness of the euro as a reserve currency.

The lack of power projection: Although it isn’t necessarily a requirement, every modern hegemon that has supplied the reserve currency was also a significant military power. In part, being a major military power like the U.S. adds to confidence that the nation can defend itself in a crisis. Europe is essentially dependent on the U.S. for defense. Consequently, in a geopolitical crisis, it’s hard to imagine that a foreign reserve manager would want to hold financial assets of a region or country that couldn’t defend itself.

The yuan: China is the second largest economy in the world and, in purchasing power parity terms, it may be the largest. It has a sizeable military. Here are its impediments:

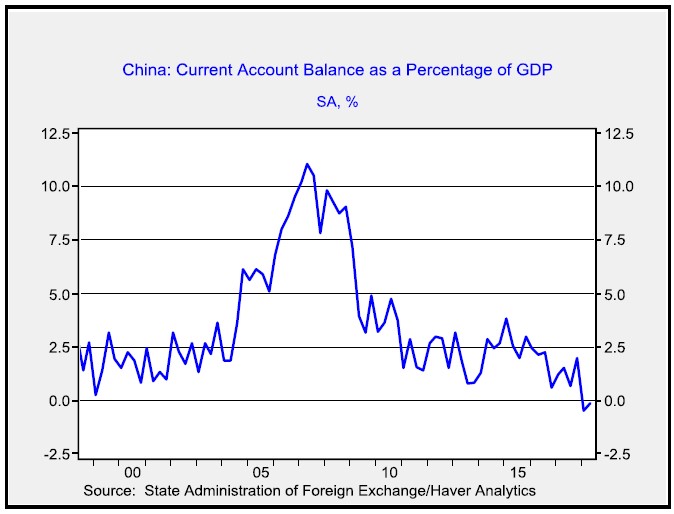

The apparent preference for current account surpluses: Although China may not be as devoted to surpluses as Germany, there is ample evidence it has tended to run them.

China does need to rebalance its economy from overdependence on exports and investment and move toward consumption. Chairman Xi has consolidated power and thus has the political capital to make the

adjustment. However, it is highly probable that the transition will lead to a period of weaker than normal economic growth. The Communist Party of China (CPC) has mostly lost its “metaphysical” allure.

Marx’s belief in progress and the eventual global victory for communism has mostly devolved into myth. Instead, the CPC offers strong economic growth for its legitimacy. Unless it replaces growth with something

else, the actual transition may not occur in the foreseeable future. If so, China probably can’t tolerate the drag on economic growth that would come from persistent current account deficits.

The lack of deep financial markets: China does not have fully open capital markets. It manages its exchange rate and has capital controls. Although China would likely allow reserve managers to hold Chinese

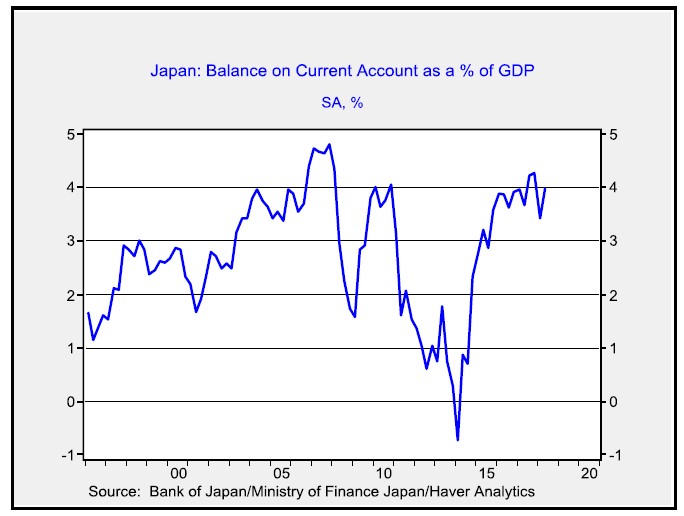

assets, those managers would have to realize that, in times of stress, China may not allow funds to leave its financial markets. Japanese yen: Although the Japanese economy is large, it fails most of the other

tests.

The preference for current account surpluses: Like Germany, Japan recovered from WWII by running trade surpluses. It continues, for the most part, to oversave and has an economy structured for trade

surpluses.

The narrowing and short-term deficit that developed was mostly due to a strong exchange rate. With Abenomics, the exchange rate has weakened and the current account surpluses have returned. It would take a major restructuring of the Japanese economy to reverse this policy preference. The lack of power projection: Although Japan has a rather impressive military, it is restricted by its constitution from projecting power. Although this legal restriction may eventually be removed, Japan probably would not pass this requirement for a generation.

The others: The British pound, once a reserve currency, is no longer a candidate. Its global influence will likely shrink further after Brexit. Non-fiat, non-liability backed currencies, such as a gold or metallic standard or cryptocurrencies, are possible replacements but would likely not be acceptable to most nations for two reasons. First, they would not want to give up sovereignty. Second, democracies today would not be willing to enforce austerity to hold the “peg.” Historical evidence suggests that support for the gold standard is strongest when suffrage is restricted to creditors.5 When the vote is expanded, the ability of governments to remain in a restricted currency system is lessened.

There is the potential for a shared reserve currency, managed by an international body such as the IMF or the G-20. Something akin to the Standard Drawing Rights (SDR) has been proposed. However, there is no collective government body that could guarantee the full faith and credit of sovereign debt issued in such “basket” currencies. And, it isn’t obvious which one of the collective nations contributing to the basket would be willing to run current account deficits in order to keep the supply of global currency available.

The U.S. dollar may not be the best reserve currency; however, it maintains that role because there isn’t a more attractive alternative at this time.

Deglobalization

Although the reserve currency role does offer benefits to the U.S., the political situation in America makes it clear that either (a) voters don’t perceive it as such, or (b) the benefits of the reserve currency are not equally distributed. To some extent, it’s a bit of both. One of the main benefits of the reserve currency is that the competition from imports keeps inflation down. However, inflation has been low for so long that an increasing majority of Americans have no memory of the high inflation years of the 1970s. As a result, they are acutely aware of the pressure on employment and wages from globalization but underestimate the value of low-cost goods.

At the same time, a globalized world allows those with the talent, ambition and circumstance to ply their trade on a global scale. This boosts the value of their labor relative to those without such advantages. It is clear that inequality has become a key issue not only in the U.S. but across the West. And, globalization is taking some of the blame for those woes.

One potential solution is to create regional blocs that would use regional reserve currencies. To some extent, this is what the U.S. had during the Soviet era. The ruble, renminbi and the eastern bloc currencies were non-convertible in the West. The Soviet Union did have a trading and aid bloc6 that would transact in barter-like trade. The Soviets acquired hard currency with commodity exports that they used to help the communist bloc acquire goods. But, from the U.S. perspective, it did not have any reason to be the importer of last resort for the non-free world nations.

The regional hegemons would have at least some of the requirements of a reserve currency provider. They would likely need to run current account deficits unless they created colonies that they could “dump” their excess saving upon while accepting the imports of the “free” nations within the region. China’s “one belt, one road” system could perhaps be a way to manage a yuan bloc. The poorer nations would become effective colonies of China while the richer nations would become part of the broader China trading region. In theory, Europe could be dominated by Germany, although anyone with a modest knowledge of history would likely have some discomfort with this plan. Still, it might be workable.

A world with three regional blocs (the U.S. would dominate at least North America and probably the Western Hemisphere) would be much more manageable for the hegemons. Military spending would likely drop in the U.S. but rise elsewhere. Trade would obviously become concentrated within regions and become less common outside these regions. To some extent, this would be a turn to a global power duopoly or oligopoly. That outcome may not be ideal, but it may be the solution the world is moving toward.

Ramifications

A world of regional hegemons would be partly deglobalized. Supply chains would shorten which would be less efficient. Without a global hegemon guaranteeing open seas, trade would likely decline. It’s a world where price levels would rise due to less efficiency, but it would also be a world where job competition would be lessened, which would be politically attractive. Perhaps the best way to think about it is that the globalized elites have benefited for the past four decades, whereas the next forty years might be a reversal.

Regarding market impact, the short-run concern is primarily the dollar. Because trade restrictions and sanctions are raising concerns about dollar supply, the administration’s actions are bullish for the greenback. Over time, the dollar could suffer greatly if we start to see regionalization develop. Longer term, a regional world is an inflationary world. Long-duration rates will rise, commodity prices will benefit and equities will suffer, but to a lesser extent than bonds.

Article by Bill O’Grady of Confluence Investment Management