It has been more than four months since the European Central Bank has officially finished currency printing. It would seem that it was a short period of time, and yet bankers were able to prepare themselves for several important changes. Interestingly, the ECB’s plans primarily concern the banks rescue. By all means.

Q1 hedge fund letters, conference, scoops etc

The current situation in Europe

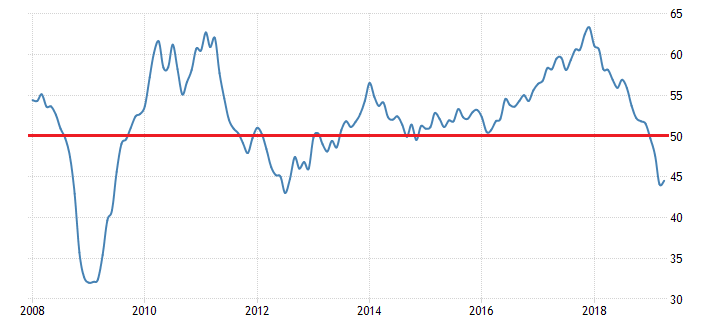

Europe’s latest economic data does not look very optimistic. Rapidly declining Manufacturing PMI index in Germany (based on the data from enterprises accounted for 20% of the German economy) is at its lowest levels since 2012. We would like to remind you that the level above 50 means the sector expansion, and below 50 contraction.

source: tradingeconomics.com

Such dramatic results were mainly due to the largest drop in factory orders and exports since the financial crisis.

Over the last few months, the growth rate has also decreased throughout the Europe. Italy is in recession. GDP in France regularly falls. German economy have not experienced growth over last two quarters. As a result, the annual GDP growth rate in the Eurozone is only 1.1% (see chart below) – despite the fact that at the end of 2017 it was 2.7%.

The deteriorating economic data leads European Central Bank, which is struggling to save the situation to more desperate activities.

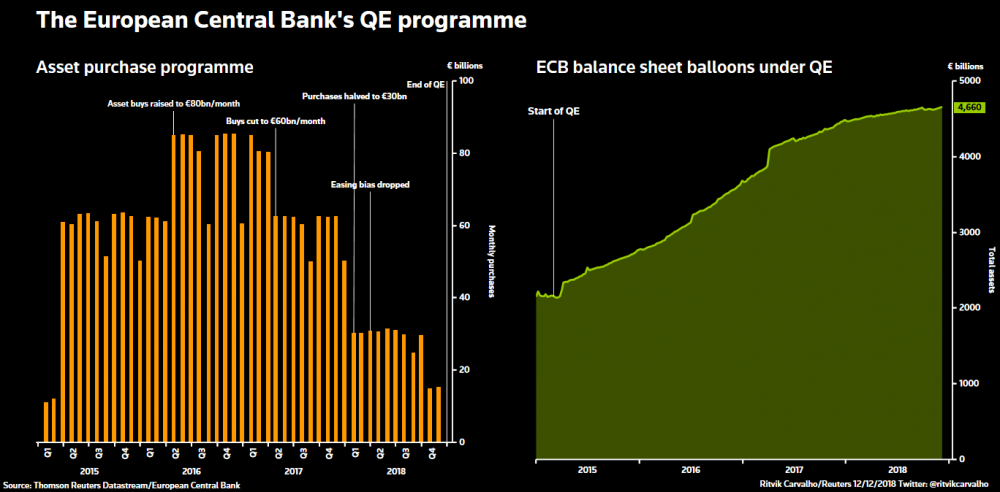

At the end of 2018, after more than 3 years, the ECB has officially finished currency printing, called Quantitative Easing (QE). At that time, the central bank’s balance sheet almost doubled to around 4.66 trillion euros (the right part of the chart). In turn, on the left side of the chart, we can see that at the peak moment the European Central Bank was printing as much as 80 billion euros a month.

In our opinion, the banking system in Europe is still not capable to operate without the central bank’s help. We have described this in the article: “Did the ECB really end up printing?“. We stated there, that the ECB will again introduce another form of currency printing. In line with our expectations, on March 7, ECB announced the third round of TLTRO (Targeted Longer-Term Refinancing Operations), which are cheap loans for commercial banks, We will return to these operations later. Subsequently, on April 10, the central bank has announced that they leave their key interest rates unchanged.

As a reminder, the European Central Bank sets the level of 3 interest rates:

- The interest rate on main refinancing operations (MRO), i.e., the level of interest that commercial banks must pay to the central bank for borrowing money for a period of 7 days. Currently, it is 0%.

- Deposit facility rate – it determines the amount of interest that commercial banks receive for keeping their excess reserves overnight at the central bank – currently it is -0.4%, it means that commercial banks actually have to pay the central bank.

- Marginal lending rate determining the amount of interest on a central bank overnight loan granted to commercial banks. Currently, it is 0.25%.

To all above mentioned activities of the central bank, we must also include never ending market supporting statements of the European Central Bank representatives. At a recent ECB conference, President Mario Draghi said that: “we are ready to use all available instruments.” This is kind of a reference to July 26, 2012, when Draghi said that ” Within our mandate, the ECB is ready to do whatever it takes to preserve the euro”. As you know, since then, the euro has significantly weakened against the dollar. On the other hand, bankers have managed to achieve their highly desired goal: the euro area is still operating.

Different ways of rescuing banks in Europe

Over the last several years the European banking sector has been in a dramatic situation. ECB and particular governments desperately try to help the European banks to stay afloat. Unfortunately, everything takes place at the expense of citizens, furthermore leading to a even greater wealth inequality between the rich and the poor.

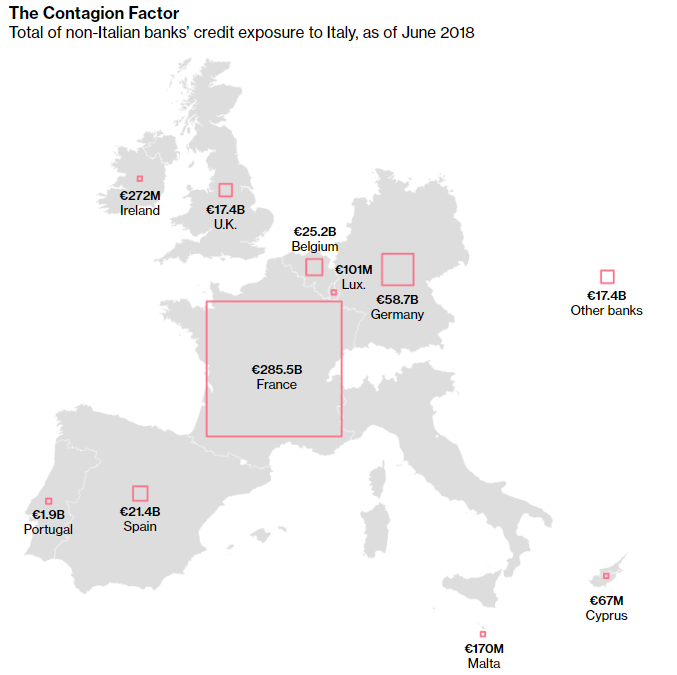

Over the recent years, bailouts became one of the ways to save banks with taxpayer’s money. In other words, working people finance irresponsibly managed financial institutions. Over the last three years, there have been 7 bailouts in Italy. The main reason for saving the Italian banks is huge exposure of the Eurozone banks to the Italian debt – it amounts to as much as 425 billion euro. The chart below presents individual European countries credit exposure to Italy.

source: bloomberg

The chart shows that the most exposed country is France, owning 285.5 billion euro of Italian debt.

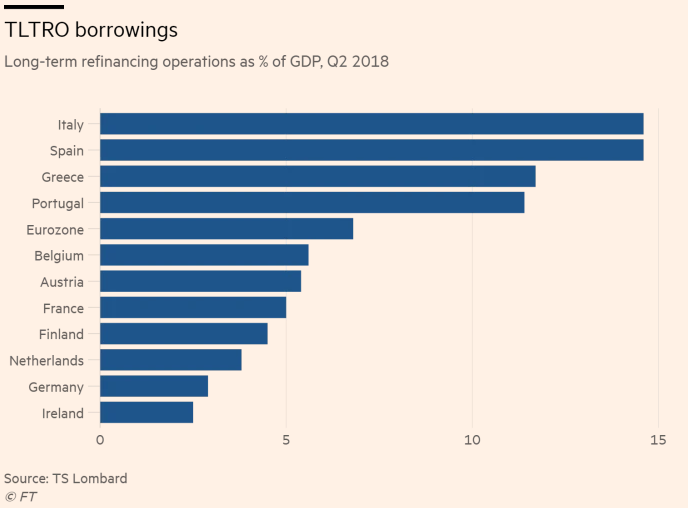

The other way to help European banks are less-known, hidden under mysterious name (TLTRO), which are cheap loans to commercial banks. So far in Europe, two rounds of this program have been implemented, whereas details of the third one are already discussed among the ECB representatives. According to the ECB, their goal is to stimulate economic development and raise inflation. In fact, however, this is another financial support for banks of euro area. It has to be emphasized that during the previous two rounds of TLTROs, the ECB created 724 billion euro from the air. It is also not surprising that Italy and Spain are the countries which benefited the most. In both countries, the so-called cheap loans account for 15% of their GDP. It can be seen on the graph below.

How much currency ECB will create during the 3rd round? We do not know yet. We know however, that plans for even further support of European banks do exist. Those plans are in fact a part of the monetary policy which benefits the richest.

A special relief for banks in Europe

To make it easier to understand what are we talking about, let us remind you the above mentioned deposit facility rate set by the European Central Bank. Currently, it is set at -0.4%. Thus, commercial banks have to pay interest to the central bank for holding overnight their excess reserves on the ECB account. In 2018, the interest amounted to 7.5 billion euros per annum.

For comparison, the total profit of all euro area banks in 2017 was 100 billion euros. Thus, an amount of 7.5 billion euros is important part of the banks income.

Why do we mention this? The ECB is considering setting the deposit rate which will be more favorable for banks. Assuming that it will be raised to 0%, it will mean an extra 7.5 billion euros in the bankers’ pockets. We are not sure if this will happen, but the last words of the ECB president about the willingness to use all available instruments suggest that the bankers determination is enormous.

Note that, in the optimistic scenario for the banks, we can see simultaneous preparations of:

- a) A better deposit rate for banks;

- b) Cheap loans for banks hidden under TLTRO abbreviation (previously the interest rate on loans was 1%, now it will probably be similar).

It seems that the ECB is trying to prepare as soft environment as possible for the banks, in order to help them survive in case of further problems. Saying that, we mean even more unpaid loans by individuals and businesses (this will be the effect of the recession that has just appeared in Europe). To put it simply: the ECB officially states that its activities are aimed at stimulating the economy. In reality, however, it is only about providing liquidity for banks, so that they will be able to survive another difficult period.

Summary

The current problems in the Eurozone begun with the introduction of the euro in 2002. Since then, many Western European countries has started to operate in the low interest rates environment. Banks in the pursuit of profits, commenced to massively give loans, often acting too hastily.

Now, the European economy is in such deplorable situation, that the ECB representatives are moving towards more radical solutions in terms of the monetary policy loosening in the euro area. As usual, saving banks is a priority. Above, we just described that commercial banks will be probably relieved from paying 0.4% interest for excess reserves held the the central bank. This is another step towards:

a) Special treatment of banks – if you once introduce such a special interest rate for banks, it will stay there forever. Nothing is as permanent as the temporrary decisions of politicians and bankers.

b) Maintaining the ultra-loose policy – this is the reason why the European economy suffers. A very cheap credit, maintaining irresponsibly operating banks and constantly injecting liquidity means that economy can not “clean up”. Thus, unprofitable entities are still functioning, which are blocking the development of smaller companies and banks. The productivity increase is practically invisible.

The European Central Bank should be remembered as the one who has destroyed Western European economies. One can guess, that when real problems show up, the media will look for reasons in Brexit or other political events. However, the facts are that this is the ECB who has contributed the most in economic stagnation of the euro area. Instead of allowing the revival of Western Europe economies, they introduced cheap loans conducting monetary policy for the rich. At the same time, as it was in case of the U.S., “too big to fail” banks has been created. After 10 years of this stupid policy, it is evident that prosperity can not be printed.

Despite the dramatic situation of the European banking sector, we think that shorting banks does not make sense. Most of them already have low valuations, and Draghi’s announcement (about using all available instruments) sounds very serious. One ECB decision may lead to the strong spike in European banks stock prices, which is a good reason not to bet against them.

Article by The Independent Trader