As growth stocks continue to dominate, we examine what’s driving growth’s performance and why we believe value’s time will come.

[timeless]

Q2 hedge fund letters, conference, scoops etc

Year after year, growth has beaten value. Although we can’t forecast when value will once again outperform growth, we know it will happen — and it will happen in a big way when it does. Here’s a framework for putting value’s struggle in perspective.

- Has the period of value underperformance been as bad as it seems?

- What’s driving growth’s outperformance?

- Is this truly a new paradigm for investing?

- Are we bold enough to call a bottom of value versus growth performance?

- How should value investors cope?

- How do value managers keep up until the turn?

- Bottom line

Has the period of value underperformance been as bad as it seems?

In a word, yes. For the first six months of 2018, growth, as measured by the Russell 1000 Growth Index (+7.3%), has crushed value, as measured by the Russell 1000 Value Index (-1.7%), by nearly 900 basis points, bringing the trailing 12-month total outperformance to 15.7% as of June 30. For the trailing 10 years, growth has outperformed value by an astounding 7,987 basis points. This appears to be the longest stretch of growth outperformance since Russell rolled out its style indices at the end of 1978.

What’s driving growth’s outperformance?

Disintermediation is a driving force in capitalism. It has removed the middlemen in many transactions, allowing companies to deal with customers more directly. This particular era of disruption has been substantial in both size and duration. Over the past decade, companies like Amazon have accelerated their growth rates and valuations, much like snowballs rolling downhill. As a direct consequence, disintermediated businesses like retailers have seen compressed margin structures and valuations. Combined, this accounts for much of the performance disparity between growth and value. Of course other factors have played a role as well, including:

- Low interest rates and slow economic growth. These conditions favor growth stocks because the lower the interest rate, the more valuable a percentage point of growth is to an investor.

- Explosive growth in passive index funds, many of which are weighted heavily toward high-growth, large-cap disruptors.

- Record-low market volatility. Unusually calm markets have provided neither a break in growth stocks’ momentum nor motivation for investors to buy value.

Is this truly a new paradigm for investing?

As powerful as these recent results have been, we believe we’re nearing the end of what’s been an elongated cycle, not a new paradigm.

Looking at economic history, we can see that today’s growth names are not guaranteed to stay dominant.

- The end of the 1990s was also a period of radical change and disruption. Back then, it was the dot-com era and, though in contrast with today, valuations were propelled more by hope and hype than demonstrated growth, which is the case today. Though we are not making the case that many of today’s leaders are going to zero as was the case 20 years ago, it might be instructive to remember that companies like Yahoo and Alta Vista were the dominant search engines before Google, and Motorola and Nokia were dominant in phones before Apple.

- Things change, and while some companies adapt and thrive, others fall behind — a process economist Joseph Schumpeter described more than 75 years ago as “creative destruction.” Just a few years ago, Best Buy and WalMart were viewed as “Amazon road-kill,” yet both adapted to the e-commerce threat and are now enjoying all-time highs this year. Not everyone adapts, and once-juggernauts like Blockbuster Video and Sears have been relegated to the same dustbin of history where the buggy whips went after cars became mass produced.

To Schumpeter’s point, Amazon and the handful of similar growth names dominating the market today are no more disruptive than automobiles or other innovations that once captured investor interest — and not guaranteed to stay dominant.

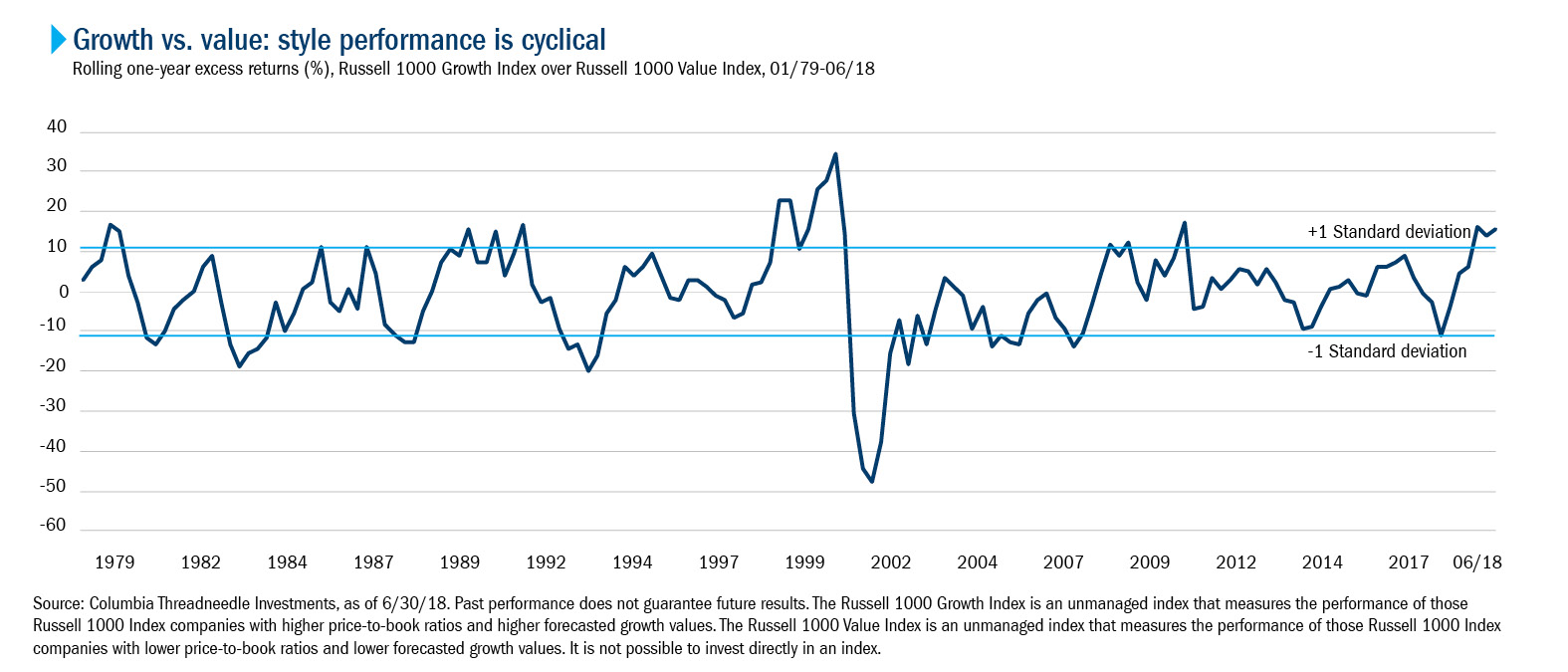

Looking at the numbers, a rolling-period analysis strongly suggests that relative style performance is cyclical, and the current growth premium may be near a peak. The following chart shows the rolling one-year return differential between the Russell 1000 Growth and Value Indices. Note that the current growth premium is well outside one standard deviation, a relationship that has only occurred 25% of the time since inception (half of which came during the tech bubble/burst nearly 20 years ago). Cyclicality is even more pronounced over longer periods of time.

Are we bold enough to call a bottom of value versus growth performance?

No! We’re simply trying to provide context for the current environment. Market strategists and hopeful value investors have proclaimed an end to the growth dominance for years now, and other than a four-month respite in 2016 around the election, the trend has been relentless.

So, what will cause the pendulum to swing back to value? There are a couple of possibilities, neither of which is yet in evidence:

- Typically, value does best after a recession when a lot of pent-up earning power is about to be unleashed. Clearly we aren’t at that point today — rates are low, earnings are high, growth is strong, volatility is depressed and flows continue to move into passive strategies.

- Market dominance has always had natural limits, either caused by competition or, failing that, regulation. We believe that if Amazon were a Chinese company selling billions of dollars of retail goods at breakeven, putting Americans out of work and companies out of business, it would be accused of predatory dumping. Google and Facebook command market shares that would have made John D. Rockefeller blush. Remember: Just before regulators broke up AT&T in 1982, many investors never thought it would happen.

How should value investors cope?

Bear in mind that active growth and value managers buy the same thing when investing: earnings and earnings growth. The real difference between the two disciplines is what they’re willing to pay for those earnings. At the benchmark level, the difference between what we call value and growth is not always so intuitive. For example, 280 companies are constituents of both the Russell 1000 Growth Index and the Russell 1000 Value Index. Movement from one index into the other is far from uncommon and can further muddy style distinctions. Not just companies, but entire industries can migrate from growth to value and vice versa. Take biotech stocks, for example. Once growth index darlings, they are now mired in the value camp, selling at lower valuations than some of the airlines, despite having potential to change the world.

How do value managers keep up until the turn?

The best thing that investment managers can do in an environment like this is to stay even more faithful to our established and proven investment process, even as value continues to underperform growth. We firmly believe that consistent implementation of any investment process through all market conditions is itself a source of alpha, regardless of style. Any manager changing their stripes to accommodate a “new” environment means forfeiting whatever discipline they had previously employed.

When disruption hits, great companies do what great companies always do — they restructure their businesses, both operationally and cost-wise, so that when conditions inevitably improve, they thrive like never before. That’s the essence of value investing, and it’s where we’re focusing our efforts today: low expectations with a catalyst. Whether we find value in the biotech space, supermarkets or retailers, there are great opportunities developing for the next cycle ahead. While focusing on such opportunities, we maintain conviction in two concepts: reversion to the mean and buy low, sell high.

Bottom line

One hundred years of data doesn’t tell you when value will have its day in the sun, only that it will happen. They don’t ring a bell when style trends start to shift, but what is clear is that catalysts like accommodative money policy that have driven growth’s outperformance are ending. As a result, we believe that investors should be prepared to be early. Systematically rebalancing a portfolio (buying low and selling high) helps ensure that allocation to growth and value are always in sync with target allocations.

Article by Richard Rosen, Columbia Threadneedle Investments