Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Q2 2020 hedge fund letters, conferences and more

The financial markets operate in cycles. A bull market is a period when prices are generally rising, whereas a bear market is a period when prices are generally falling. Not all types of investments behave the same in bull and bear markets, which changes portfolio composition over time.

If a portfolio is left unchecked during a bull market, you run the risk that the equity allocation grows relative to the other asset classes in the portfolio, such as bonds. During a bear market, the reverse occurs and the allocation to bonds increases relative to equities. In both cases, you are left with risk and return characteristics that don’t match those of your strategic asset allocation.

To maintain the intended mixture of investments that delivers the risk and return expectations of the investor, the time-tested process of rebalancing reduces exposure in asset classes that have done well, while increasing exposure to asset classes that have fallen out of favor. Although it might seem to be counterintuitive, rebalancing requires taking some profits from your winners and redistributing those profits to your losers. You are selling high and buying low, which is what all of us should be doing.

However, emotions sometimes drive us to do the opposite.

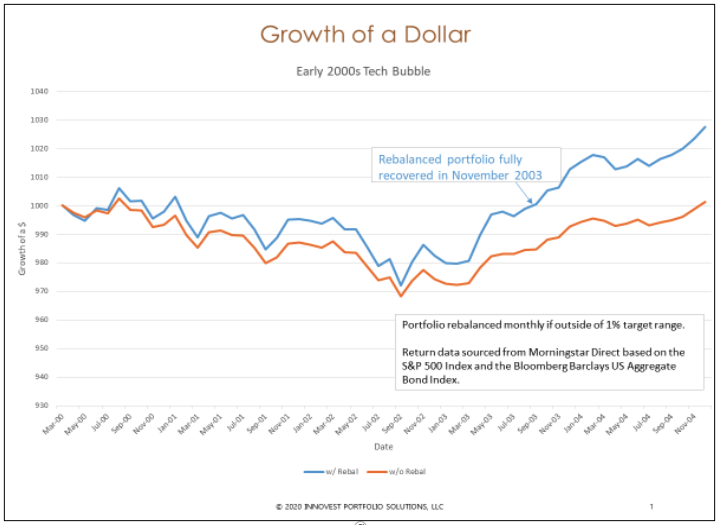

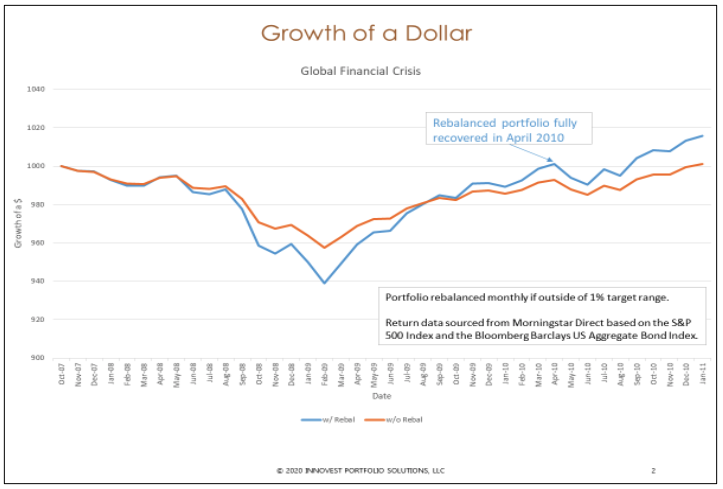

Below are two studies, conducted by Morningstar and Innovest Portfolio Solutions, which demonstrate how periodically rebalancing your portfolio can reduce downside risk, shorten the recovery time following a market downturn, and enhance return potential compared to never rebalancing.

Rebalancing can improve investment performance

Innovest Portfolio Solutions conducted a study to examine the effects of rebalancing on portfolio performance following the tech bubble in the early 2000s and the global financial crisis in 2007-2008. Innovest included both calendar-based and percentage-change rebalancing approaches. The below chart shows the results of a buy-and-hold strategy versus an annually rebalanced portfolio for a 60/40 stock/bond allocation.

A rebalanced portfolio outperformed a buy-and-hold strategy in the years following both the tech bubble and the global financial crisis. Employing a rebalancing process during the 2000s tech bubble would have resulted in approximately 2.7% of excess return and employing a rebalancing process during the global financial crisis would have resulted in approximately 1.5% of excess return.

Read the full article here by Michael Corbett, Advisor Perspectives