Owning a large number of stocks reduces risk. Less widely known is that it also increases expected returns.

Q3 2019 hedge fund letters, conferences and more

There is a tendency to think that owning a handful of stocks may be a bit riskier but have an equal likelihood of outperforming the market as a whole. This is wrong for two reasons:

- Higher standard deviations lead to lower returns; and

- A portfolio that is smaller but has a standard deviation equal to the market’s is still expected to underperform the market.

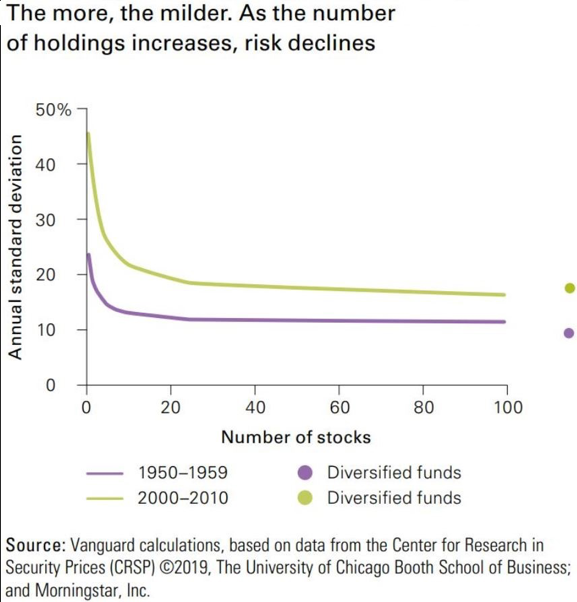

A recent Vanguard paper, What’s a Mutual Fund Worth?, demonstrated that U.S. stocks are more volatile than in the past. The authors (Andrew Clarke, Michael Nolan, and Tyrone Sampson) showed a portfolio of one stock has an annualized standard deviation of 45.3%, while 100 stocks reduce the standard deviation to 16.3%. Yet the investor is not compensated for diversifiable (idiosyncratic) risk, as we know.

Lower standard deviations can equate to higher returns

That lower standard deviation can increase returns is less well known. To explain this simply, a stock that increases 30% in one year and declines by 10% in the second year has a 10% simple average annual return but a geometric return of only 8.17%. A portfolio that increases 10% each year for two years also has a 10% simple average annual return but a higher 10% geometric. What this means is that lower standard deviations lead to geometric returns much closer to the arithmetic returns. In the first case, a $10,000 investment grew by $1,700 while in the second gained $2,100.

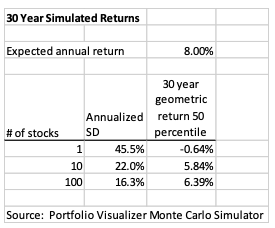

Let’s simulate 30 years of returns using Portfolio Visualizer’s Monte Carlo Simulation tool, with standard deviations calculated by Vanguard using data from CRSP and Morningstar. Further, let’s assume that any stock has an expected 8% return in any one year. This is the arithmetic return.

In the results below, a portfolio of 100 stocks has an expected long-run annualized geometric return of 6.39% but one stock has an expected loss of 0.64% annually. Ten stocks reduce the standard deviation significantly but still produce a long-run geometric return 0.55 percentage points less than the 100-stock portfolio.

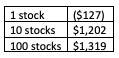

Over a two-year period with a $10,000 investment this translates to the following gains:

Over 30 years, the differences are far more dramatic. But, don’t generalize this math into a belief that lower standard deviation portfolios, such as minimum-volatility funds, reduce risk and increase returns. That is not necessarily true.

Read the full article here by Allan Roth, Advisor Perspectives