On February 22, Kraft-Heinz shocked investors with a trifecta of bad news in its earnings report: sub-par operating results, a mention of accounting irregularities and a massive impairment of goodwill, and followed up by cutting dividends per share almost 40%. Investors in the company reacted by selling their shares, causing the stock price to drop more than 25% overnight. While Kraft is neither the first, nor will it be the last company, to have a bad quarter, its travails are noteworthy for a simple reason. Significant portions of the stock were held by Berkshire Hathaway (26.7%) and 3G Capital (29%), a Brazil-based private equity group. Berkshire Hathaway’s lead oracle is Warren Buffett, venerated by some who track his every utterance, and try to imitate his actions. 3G Capital might not have Buffett’s name recognition, but its lead players are viewed as ruthlessly efficient managers, capable of delivering large cost cuts. In fact, their initial joint deal to bring together Heinz and Kraft, two of the biggest names in the food business, was viewed as a master stroke, and given the pedigree of the two investors, guaranteed to succeed. As the promised benefits have failed to materialize, the investors who followed them into the deal seem to view their failure as a betrayal.

Q4 hedge fund letters, conference, scoops etc

The Back Story

You don’t have to like ketchup or processed cheese to know that Kraft and Heinz are part of American culinary history. Heinz, the older of the two companies, traces its history back to 1869, when Henry Heinz started packing and selling horseradish, and after a brief bout of bankruptcy, turned to making 57 varieties of ketchup. After a century of growth and profitability, the company hit a rough patch in the 1990s, and was targeted by activist investor, Nelson Peltz, in 2013. Shortly thereafter, Heinz was acquired by Berkshire Hathaway and 3G Capital for $23 billion, becoming a private company. Kraft started life as a cheese company in 1903, and over the next century, it expanded first into other dairy products, and then widened its repertoire to includes other processed foods. In 1981, it merged with Dart Industries, maker of Duracell batteries and Tupperware, before it was acquired by Philip Morris in 1988. After a series of convulsions, where parts of it were sold and rest merged with Nabisco, Kraft was spun off by Philip Morris (renamed Altria), and targeted by Nelson Peltz (yes, the same gentleman) in 2008. Through all the mergers, divestitures and spin offs, managers made promises of synergy and new beginnings, deal makers made money, but little of substance actually changed in the products.

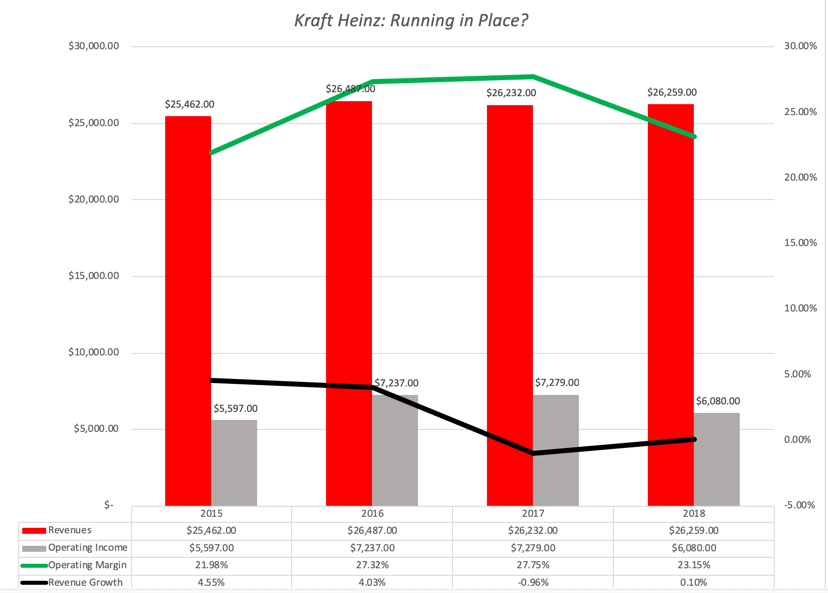

In 2015, the two companies were brought together, with Berkshire Hathaway and 3G playing both match makers and deal funders, as Kraft Heinz, and the merger was completed in July 2015. At the time of the deal, there was unbridled enthusiasm on the part of investors and market observers, and part of the unquestioning acceptance that the new company would become a force in the global food business was the pedigree of the main investors. In the years since the merger, though, the company has had trouble delivering on expectations of revenue growth and cost cutting:

The bottom line is that while much was promised in terms of revenue growth, from expanding its global footprint, and increased margins, from cost cutting, at the time of the deal, the numbers tell a different story. In fact, if investors were surprised by the low growth and declining margins in the most recent earnings report, they should not have been, since this has been a long, slow bleed.

The Earnings Report

The earnings report that triggered the stock price collapse, for Kraft-Heinz, was released on February 22, and it contained bad news on many fronts:

- Flatlining Operartions: Revenues for 2018 were unchanged from revenues in 2017, but operating income dipped (before impairment charges) from $6.2 billion in 2017 to $5.8 billion in 2018; the operating margin dropped from 23.5% in 2017 to 22% in 2018.

- Accounting Irregularities: In a surprise, the company also announced that it was under SEC investigation for accounting irregularities in its procurement area, and took a charge of $25 million to reflect expected adjustments to its costs.

- Goodwill Impairment: The company took a charge of $15.4 billion for impairment of goodwill, primarily on their US Refrigerated and Canadian Retail, an admission that they paid too much for acquisitions in prior years.

- Dividend Cuts: The company, a perennial big-dividend payer, cut its dividend per share from $2.50 to $1.60, to prepare itself for what it said would be a difficult 2019.

While investors were shocked, the crumb trail leading up to this report contained key clues. Revenues had already flattened out in 2017, relative to 2016, and the decline in margins reflected difficulties that 3G faced in trying to cut costs, after the deal was made. The only people who care about impairment charges, a pointless and delayed admission of overpayment on acquisitions, are those who use book value of equity as a proxy for overall value. The dividend cuts were perhaps a surprise, but more in what they say about how panicked management must be about future operations, since a company this attached to dividends cuts them only as a last resort.

The Value Effects

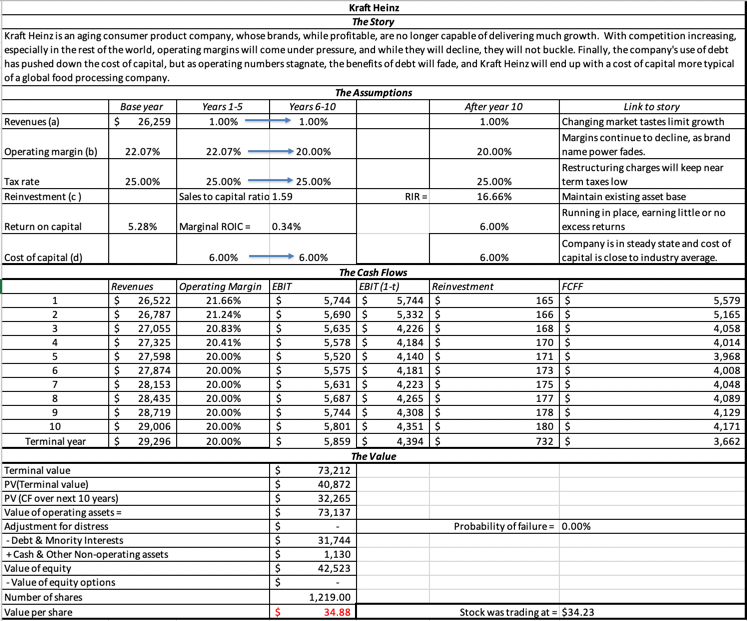

With the bad news in the earnings report still fresh, let’s consider the implications for the story for, and the value of, Kraft Heinz. The flat revenues and the declining margins, as I see them, are part of a long term trend that will be difficult, if not impossible, to reverse. While Kraft-Heinz may have a quarter or two with positive blips, I see more of the same going forward. In my valuation, I have forecast a revenue growth of 1% a year in perpetuity, less than the inflation rate, reflecting the headwinds the company faces. That downbeat revenue growth story will be accompanied by a matching “bad news” story on operating margins, where the company will face pricing pressures in its product markets, leading to a drop (though a small and gradual one) in operating margins over time, from 22% in 2018 (already down from 2017) to 20% over the next five years. The company’s cost of capital is currently 6%, reflecting the nature of its products and its use of debt, but over time, the benefits from the latter will wear thin, and since that is close to the average for the industry (US food processing companies have an average cost of capital of 6.12%), I will leave it unchanged. Finally, the mistakes of the past few years will leave at least one positive residue in the form of restructuring charges, that I assume will provide partial shelter from taxes, at least for the next two years.

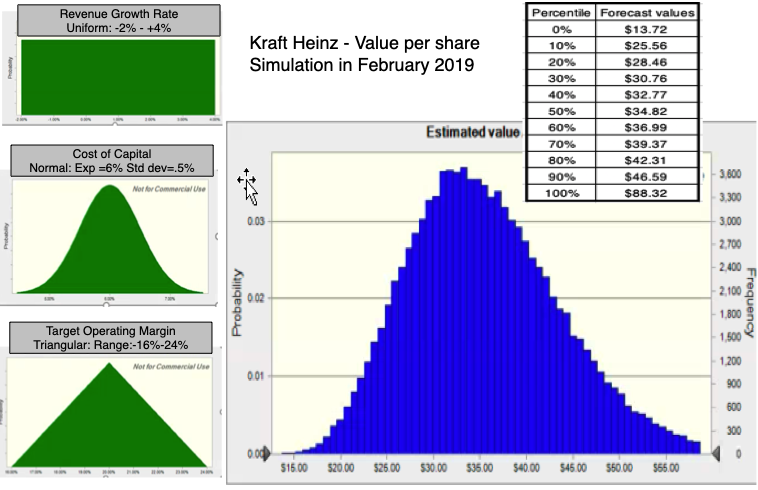

The good news is that, even with a stilted story, Kraft Heinz has a value ($34.88) that is close to the stock price ($34.23). The bad news is that the potential upside looks limited, as you can see in the results of a simulation that I did, allowing expected revenue growth, operating margin and cost of capital to be drawn from distributions, rather than using point estimates.

The finding the value falls within a tight range, with the first decile at about $26 and the ninth at close to $47 should not surprise you, since the ranges on the inputs are also not wide. As an investor, here are the actions that would follow this valuation.

- If you owned Kraft Heinz prior to the earnings report (and I thankfully did not), selling now will accomplish little. The damage has been done already, and the stock as priced now, is a fair value investment. I know that 3G sold almost one quarter of its hold 3 days after Tuesday, but that may say more about 3G than it does about Kraft Heinz.

- If you don’t own Kraft Heinz, the valuation suggests that the stock is fairly valued, at today’s price, but at a lower price, it would be a good investment. I have a limit buy on the stock at a $30 price (close the 25th percentile of the distribution), and if it does hit that price, I will be a Kraft Heinz stockholder, notwithstanding the fact that I think its future does not hold promise. If it does not drop that low, there are other fish to catch and I will move on.

There are two concerns, though, that investors looking at this stock have to consider. The first is that when companies claim that they have discovered accounting irregularities, but that they have cleaned up their act, they are often dissembling and that there are more shocks to come. With Kraft Heinz, the magnitude of the irregularity is small, and given that they have no history of playing accounting games, I am willing to given them the benefit of the doubt. The second is that the company does carry $32 billion in debt, and while that debt has no toxic side effects today, that is because the company is perceived to have stable and positive cash flows. If the margin decline that I forecast becomes a margin rout, the debt will expose the company to a clear and present danger of default. Put simply, it will make the bad case scenarios that are embedded in the simulation worse, and perhaps threaten the company’s existence.

The Lessons

There are lessons in the Kraft-Heinz blow-up, but I will tread carefully, since I risk offending some, with talk that you may view as not just incorrect but sacrilegious:

- It is human to err: At the risk of stating the obvious, Warren Buffett and 3G’s key operators are human, and are prone to not only making mistakes, like the rest of us, but also to have blind spots in investing that hurt them. In fact, Buffett has been open about his mistakes, and how much they have cost him and Berkshire Hathaway shareholders. He has also been candid about his blind spots, which include an unwillingness to invest in businesses that he does not understand, a sphere that only grows as he gets older and the economy changes, and an excessive trust in the managers of the companies that he invests in. While he is, for the most part, an excellent judge of character, his investments in Wells Fargo, Coca Cola and Kraft-Heinz show that he is not perfect. The fault, in my view, is not with Buffett, but with the legions of investors, analysts and journalists who treat him as an investment deity, quoting his words as gospel and tarring and feathering anyone who dares to question them.

- Stocks are not bonds: In my data posts, I looked at how companies in the United States have moved away from dividends to buybacks, as a way of returning cash. That trend, though, has not been universally welcomed by investors, and there remains a significant subset of investors, with strategies built around buying stocks with big dividends. One reason that stocks like Kraft Heinz become attractive conservative value investors is because they offer high dividend yields, often much higher than what you could earn investing in treasury or even safe corporate bonds. In effect, the rationale that investors use is that by buying these shares, they are in effect getting a bond (with the dividends replacing coupons), with price appreciation. From the Dogs of the Dow to screening based upon dividend yields, the underlying premise is that investors can count more on dividends than on buybacks. While it is true that dividends are stickier than buybacks, with many companies maintaining or increasing dividends over time, these dividend-based strategies become delusional when they treat dividends as obligated payments, rather than expected ones. After all, much as companies do not like to cut dividends, they are not contractually obligated to pay dividends. In fact, when a stock carries a dividend yield that looks too good to be true, it is usually almost always an unsustainable dividends, and it is only a question of time before dividends are cut (or even stopped) or the company drives itself into a financial ditch.

- Brand Names last a long time, but nothing lasts forever: A major lodestone of conventional value investing is that while technology, cost efficiencies and new products are all competitive advantages that can generate value, it is brand name that is the moat that has the most staying power. Again, that statement reflects a truth, which is that brand names last long, often stretching over decades, but even brand name benefits fade, as customers change and companies seek to become global. The troubles at Kraft-Heinz are part of a much bigger story, where some of the most recognized and valued brand names of the twentieth century, from Coca Cola to McDonalds, are finding that their magic fading. Using my life cycle terminology, these companies are aging and no amount of financial engineering or strategic repositioning is going to make them young again.

- Cost cutting can take you far, but no further: For the last few decades, we have cut a great deal of slack for those who use cost cutting as their pathway for creating value, with many leveraged buyouts and restructurings built almost entirely on its promise. Don’t get me wrong! In firms with significant cost inefficiencies and bloat, cost cutting can deliver significant gains in profits, but even with these firms, those gains will be time limited, since there is only so much fat to cut out. Worse, there are firms that find themselves in trouble for a myriad of reasons that have little to do with cost inefficiencies and cutting costs as these firms is a recipe for disaster. It is true that 3G did a masterful job, cutting costs and increasing margins at Mexico’s Grupo Modelo, the Mexican brewer that they acquired through Inbev, but that was because Modelo’s problems lent themselves to a cost-cutting solution. It may even have worked at Kraft-Heinz initially, but at this point, the company’s problems may have little to do with cost inefficiencies, and much to do with a stable of products that is less appealing to customers than it used to be, and cost cutting is the wrong medicine for whatever ails them.

Conclusion

I hope that you do not read this as a hit piece on Warren Buffett and/or 3G. I admire Buffett’s adherence to a core philosophy and his willingness to be open about his mistakes, but I think he is ill served by some of his devotees, who insist on putting him on a pedestal and refuse to accept the reality that his philosophy has its limits, and that like the rest of us, he has an ego and makes mistakes. If you have faith in value investing, you should be willing to have that faith tested by the mistakes that you and the people you admire make in its pursuit. If your investment views are dogma, and you believe that your path is only the correct one to success, I wish you the best, but your righteousness and rigidity will only set you up for more disappointments like Kraft Heinz.

YouTube Video

Data

Article by Aswath Damodaran, Musings on Markets