Value stocks have had a hard time in recent years, and this persistent underperformance is putting traditional and long-held ideas at risk of being thrown out and discarded. Terms like “value investing is dead” are starting to be thrown around along with the typical clichés like “new paradigm”, “structural change”, and “new normal”. But we’ve noticed a couple of particularly interesting developments for US value stocks that investors ought to pay attention to.

Q2 hedge fund letters, conference, scoops etc

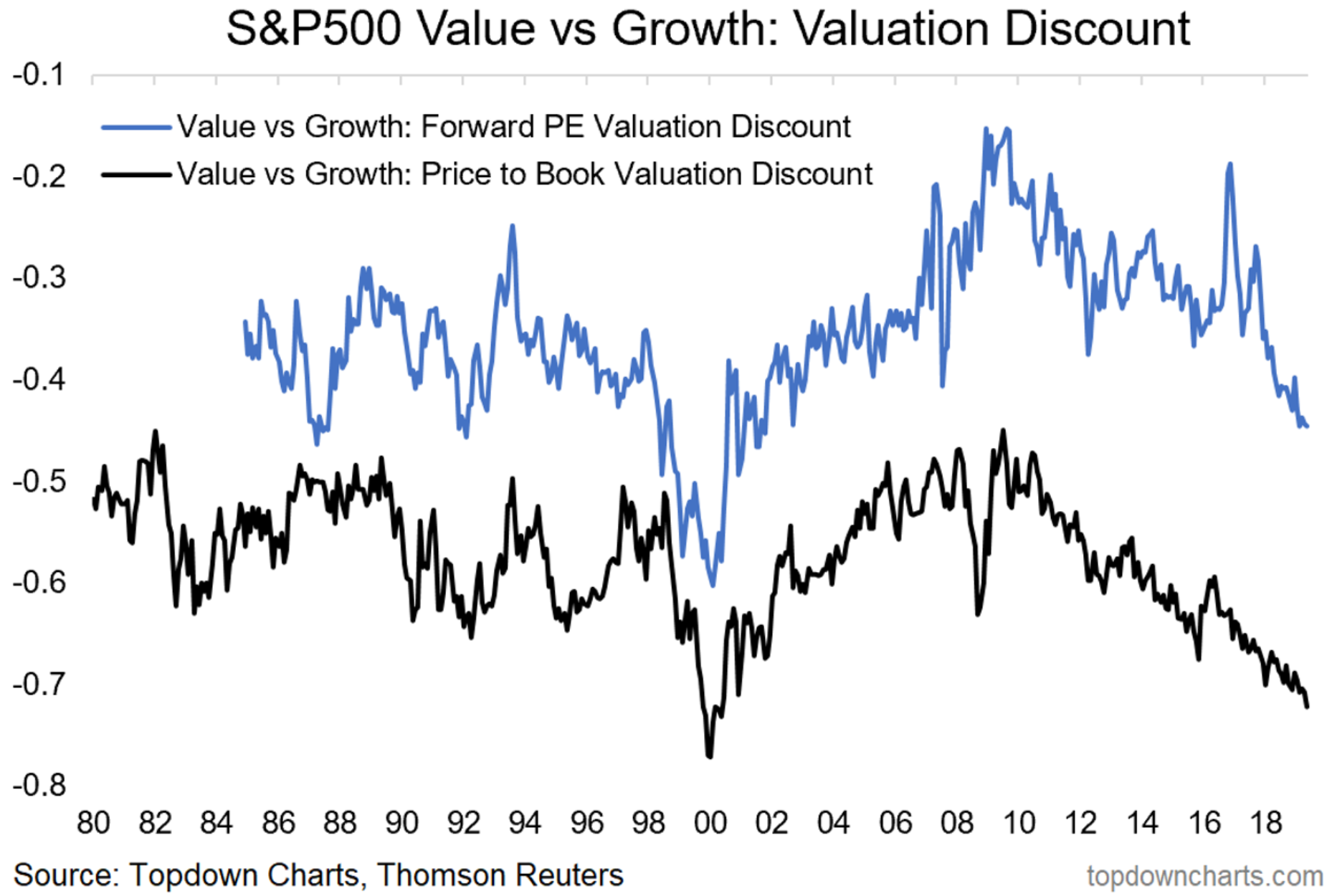

The main chart in focus today comes from a report where we took a closer look at valuations across sectors and industries in the S&P500.

The chart shows the value of value is about as good as it gets, with the relative value of value stocks trading close to record lows.

Specifically, what we’re looking at here in the blue line is the ratio of the forward PE of value stocks vs growth stocks. And the black line shows the same thing but for the price to book ratio.

Now, it’s important to note, that by definition value stocks will always be cheaper than growth stocks. But there is clearly a range there, and this range basically maps to the cycles of performance in value vs growth stocks.

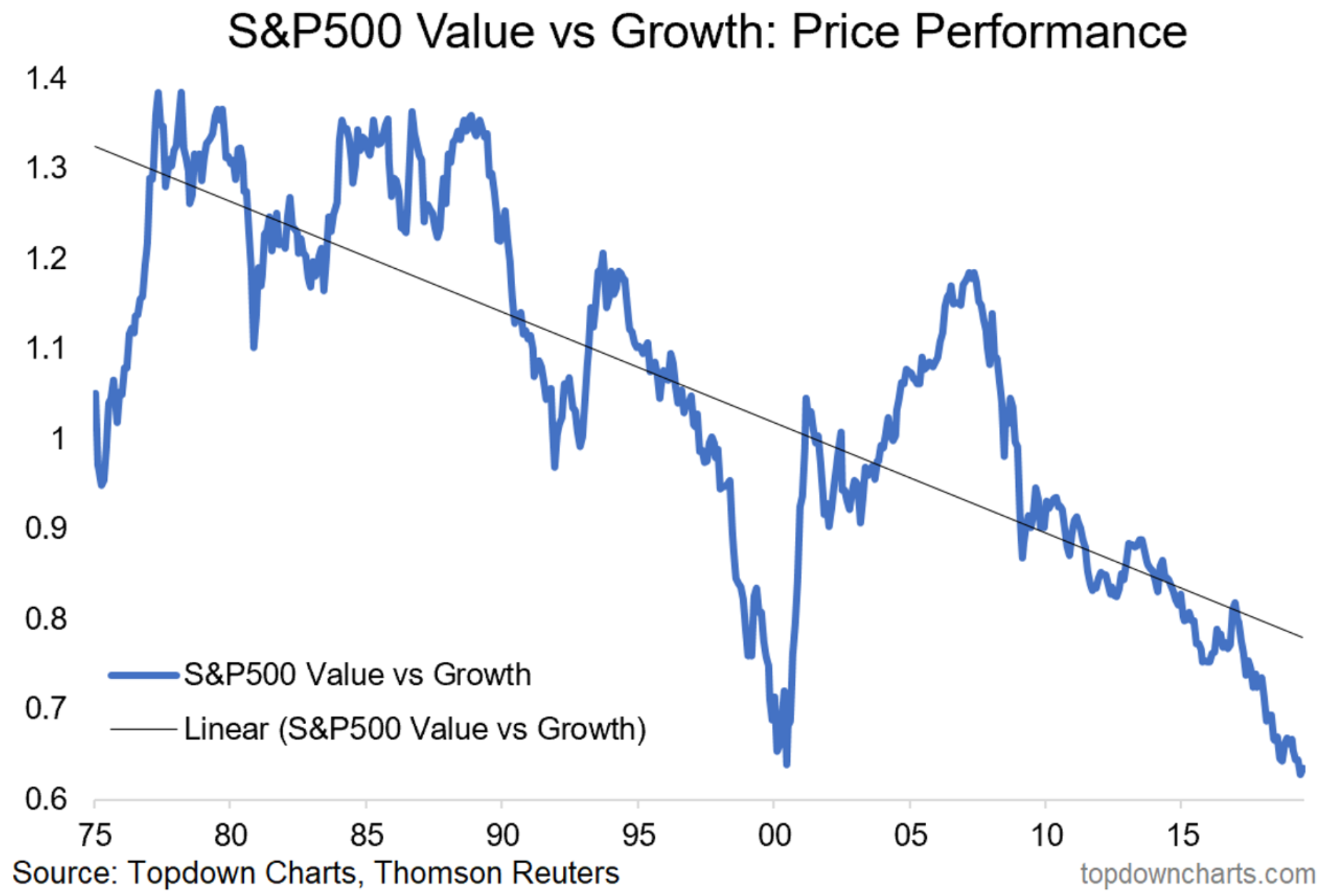

Speaking of which, it truly has been a lost decade for value investing, as the chart below shows near persistent underperformance by value stocks vs growth stocks over the past decade or so.

But with relative performance matching what we saw at the height of the dot com bubble, it seems the right question to ask is whether its time for some mean reversion here?

Strictly on the valuation side, the relative value picture shows near record lows – or at least cycle lows. So value stocks certainly have relative value on their side. Albeit as a side note, I would point out that our analysis shows value stocks are *not* necessarily cheap vs their own history… i.e. the rising tide has lifted all valuations.

In that respect, I think it could be quite likely that the way we get to mean reversion in relative value and relative performance here is that a broader valuation mean reversion event drives a correction through both value and growth stocks falling, but just value stocks not falling as much.

Either way, strictly from a valuation standpoint value stocks are certainly attractive. And if you think how late we are in the broader market/business cycle, it could make sense to have a fair representation of value stocks in the portfolio even if only for defensive purposes.

If you like my free articles, you will probably like our Marketplace service, which takes a deeper look at select ideas, provides you with a big picture weekly global market snapshot, and a monthly cheat-sheet on the outlook across global markets… Must-have market-intel for active investors.

Article by Top Down Charts